“Growing up, I heard the word genius a lot.”

-Angela Duckworth

For those of you who are new to following me, you’ll realize that I am no genius. In the mess of strategists and economists you can read rants from in the morning, I may very well be the furthest thing from it.

The aforementioned quote comes from a book I cracked open this weekend called Grit – The Power of Passion and Perseverance. So far the book is ok. Unlike Duckworth, I didn’t grow up listening to my Dad talk about geniuses in the WSJ. I was taught to grind.

If you spend enough time grinding it out in macro markets, you’ll be taught many lessons in humility. Don’t let those deter your professional progress though. Every mistake leads to a learning opportunity. The faster you learn, the faster you grow.

Back to the Global Macro Grind…

With $13.4 TRILLION in negative yielding bonds out there globally (up from $13.1T last week), most macro market participants are learning that without A) #GrowthSlowing and B) falling bond yields, that returns in both stocks and bonds won’t grow much faster.

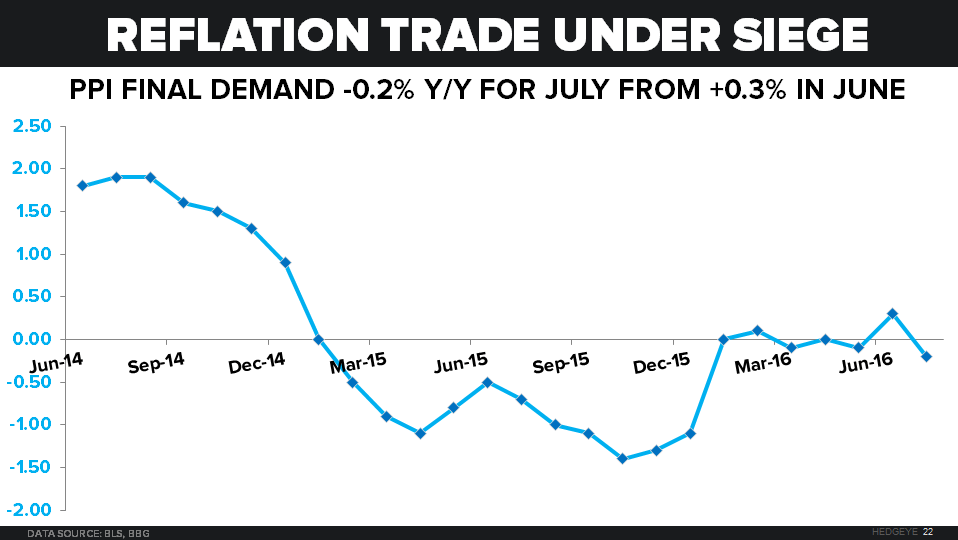

I guess that’s partly why, on the heels of both US Retail Sales and Producer Prices (PPI) slowing on Friday, both US stocks and bonds remained close to their all-time closing highs.

With the “reflation” trade under siege since peaking in early June, a -0.2% year-over-year Producer Price report for JUL (vs. +0.3% y/y in JUN) gave the market what it loves most when it can’t beat 1% GDP growth – Down Dollar, Down Rates:

- US Dollar Index ended the week down -0.5%

- US 10yr Yield fell 8 basis points on the week to 1.51%

- CRB Index and Oil reflated +0.5% and +6.4% on the week, respectively

In the UK they get this evisceration of the purchasing power of The People program (via Down Pound) much more readily. With the British Pound down another -1.2% last week (vs. USD), the stocks in London (FTSE) ramped another +1.8% to +10.8% YTD.

Not to be confused with something like the Nasdaq or SP500, which were +0.1% and +0.2% on decelerating volume last week to +4.5% and +6.9% YTD, respectively, the UK stock market looks more like their athletes (37 medals in Rio!) than their poor people do.

Yep. That’s how the math works. If you get paid in a currency… and I burn it for the sake of “reflating asset prices” in that currency… you get poorer, in that currency. So you better own some bonds, buildings, and stocks… so that you aren’t as poor as real poor people.

Back to the USA, here’s how the Equity Sector Styles paid out on a Down Dollar, Down Rates week:

- Energy Stocks (XLE) led gainers, closing up +1.7% on the week to +13.9% YTD

- Financials (XLF) led losers (again), closing down -0.7% on the week to +0.1% YTD

Poor bankers.

Due to their own architectural genius I’m sure, banks have empowered and employed an un-elected set of central-market-planners that have officially become the causal factor in the “under performance” of their equities (yes, many bankers still get paid “in stock”).

Great week for stocks (and the bonds that are outperforming them)! But another brutal week for one of the leading indicators on how banks make money (i.e. the Yield Spread). Here’s how that spread looked subtracting the 2yr yield from the 10yr yield last week:

- US Yield Spread down another -6 basis points on the week to 80bps = down -41 basis points (bps) YTD

- UK Yield Spread down another -14 bps on the week to 38bps = down -93bps YTD

- JGB Yield Spread down another beep on the week to 9bps = down -19bps YTD

True, Japanese Bankers aren’t as genius as American ones these days. That’s what happens when your central bank has almost inverted your yield curve. Once that happens, the only guys who can try to be rock-stars are the bankers at the central bank itself.

Oh, you as an American, British, or European banker don’t like that? Maybe you should think about a career pivot into central-market-planning. As of last week it looks like the Bank of Japan (BOJ) is a Top 5 holder in 81 of the 225 stocks in the Nikkei!

That’s right – after another GDP #GrowthSlowing report (Japan’s GDP for Q2 was 0.2%), the Japanese are trying to teach all bankers around the world that, Ex-Banks, stocks can never go down (ever again) provided that central bankers buy them with printed money.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.46-1.58%

SPX 2156-2194

NASDAQ 5110-5265

Nikkei 166

VIX 11.01-14.77

USD 94.99-96.64

YEN 100.06-103.21

Oil (WTI) 39.28-44.98

Gold 1

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer