Here's analysis from Hedgeye CEO Keith McCullough in a note sent to subscribers earlier this morning:

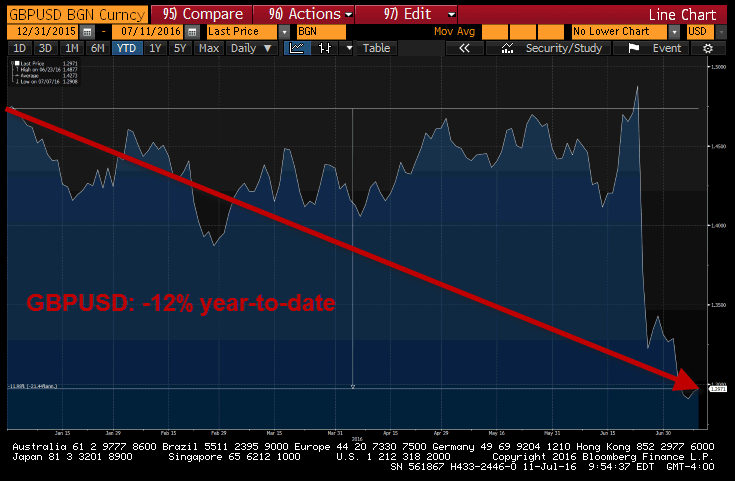

"With most US beta chasers talking “SP500” today, let’s stay focused on the bigger macro picture which is highly correlated to what USD is doing in the FX War. UK 10yr Yield dives to 0.71% this morning and the Pound’s crash are to lower-lows -0.7% at $1.28."

Meanwhile in Japan...

The yen weakened as Japanese Prime Minister Shinzo Abe "ordered a new round of fiscal stimulus spending after a crushing election victory over the weekend," Reuters reports. Abe was light on specifics but Reuters sources say that before the election "the government was ready to spend more than 10 trillion yen ($100 billion)." Here's analysis from McCullough:

"Yen slammed -1.6% vs. USD (our Yen SELL signal went out late last week – let’s see if its more than a trade) and this gets interesting now with USD UP year-over-year and everyone racing the British to the bottom; EUR/USD was a big focus of my Q3 Macro Themes Call and looks as precarious as it has in a year at $1.10."

We'll see if Abe's jawboning translates into action and if that breaks the clear cut trend ... Yen strength.

One thing is clear, central planners are just getting started.