“Sound was ethereal, not tangible.”

-Steven Johnson

Global Macro Themes are far from ethereal. That word is one Steven Johnson used to describe sound in How We Got To Now (“e-the-real: lacking material substance or extremely delicate and light in a way that seems too perfect for this world” –Merriam Webster).

“For thousands of years after Neanderthal singers gathered in the reverberant sections of the Burgundy caves, the idea of recording sound was as fanciful as counting fairies… no one had imagined capturing sounds directly. Sound was ethereal, not tangible.” (pg 90)

Obviously, as a macro-economics profession, we’ve moved beyond being baboons. But for whatever reason, Old Wall Consensus has had a very difficult time capturing data (both economic and real-time market data) and contextualizing it within longer-term cycles. That’s how you generate tangible Macro Themes. Instead of lacking substance, that’s how we try to make tangible calls.

Back to the Global Macro Grind…

No. Not all of our Macro Themes end up playing out. But we have built Hedgeye on a Research & Risk Management #Process that tends to be better than bad. The long-term goal, of course, remains excellence.

Turning tangible Macro Themes into big Global Macro Asset Allocation calls is the current manifestation of our #Process. Inspired by Bayesian Probability Theory, our best forecast for tomorrow perpetually evolves from what we just learned today.

Yes. Measuring and mapping TRENDING rates of change is a grind. It takes a disciplined and independent Research Team to both execute on that process (for 50 economies and their stock, bond, currency, etc. markets) and respond objectively to its messaging.

Once that’s done, across durations (TRADE, TREND, and TAIL @Hedgeye), the hardest thing to do is wait and watch…

Patience isn’t only one of the hardest things to have (because we are living in 21st century of “everything needs to happen now”)… but we also have a burgeoning client base of investors who operate with different investment mandates and durations as well.

Since we can’t be everything to everyone, I’ve determined that being who we are is the best place to start.

So I’ll start with that on this morning’s Q3 Global Macro Themes conference call (and @HedgeyeTV video presentation). If you’d like access to our 88 slide deck, ping .

Our Q3 Macro Themes are as follows:

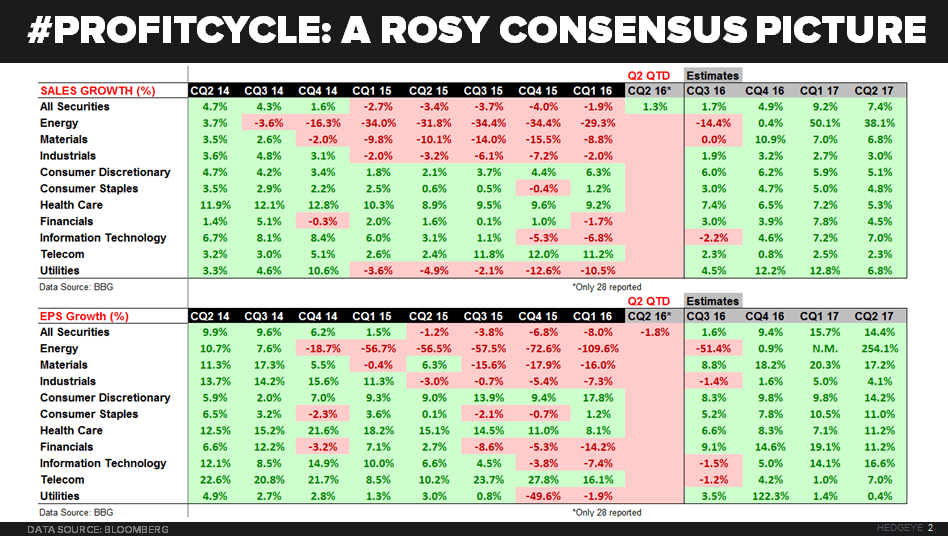

- #ProfitCycle

- #ConsumerCredit

- #EuropeImploding

Hashtag them. Timestamp them. Call them names. In case you haven’t noticed, we do not poach, borrow, or apologize for our original content. Our themes are born out of our #process, and we roll with them until we realize we are wrong.

When they’re right (that is the goal of the game!). We let them ride. Because that’s what cycles do.

That’s why I’m gravitating towards making the easiest call Theme #1 (i.e. an extension of the call we’ve been making for a year now). Theme #2 is the one with the most contrarian pop, validated by more recent data. And Theme #3 is some kind of big bang thing.

Since themes are born (and die) in probability space, what that means is:

- Theme #1 is already high probability (> 66% chance and rising towards 80-90%) because it’s already happening

- Theme #2 recently crossed the threshold of high probability (instead of a coin toss it’s at least 66% and rising)

- Theme #3 is at the threshold, but potentially has a longer-term duration to the idea/theme playing out

That’s the thing with super-long-term ideas (our new Sector Head of Demography, Neil Howe, calls them “Super TAILs”), like real-time market risk… they can happen slowly, or all at once. You need to be humble enough to embrace uncertainty with those.

Back to Themes #1 and #2 (again with the preponderance of the recent data showing a rising probability of them being right, faster, than Theme #3), the “calls” I’m going to make at 11AM are going to be:

- LONGS: Slower-and lower-for-longer (no need to change the view on the Long Bond, Rates, Gold, Utilities, etc.) #LetThemRide

- FINANCIALS: reiterated as our favorite underweight, adding US consumer credit exposures to the table pounding

- CONSUMER DISCRETIONARY: (especially “high end”) is going to be an exposure to short on bounces, with impunity

Then, like the #BeliefSystem (breaking down) call we made on our Q1 2016 Macro Themes call, we have a bigger bang theory on this grand-central-market-planning-experiment called the Eurozone and her young ethereal currency they call the Euro.

I’m looking forward to not only presenting what we view as developing truths, but engaging in post call debates with clients, worldwide, on where we could be right or wrong. Collaboration is a long-term tangible theme for modern day risk managers too.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.29-1.50%

SPX 1

NASDAQ 4

VIX 14.11-25.29

EUR/USD 1.08-1.12

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer