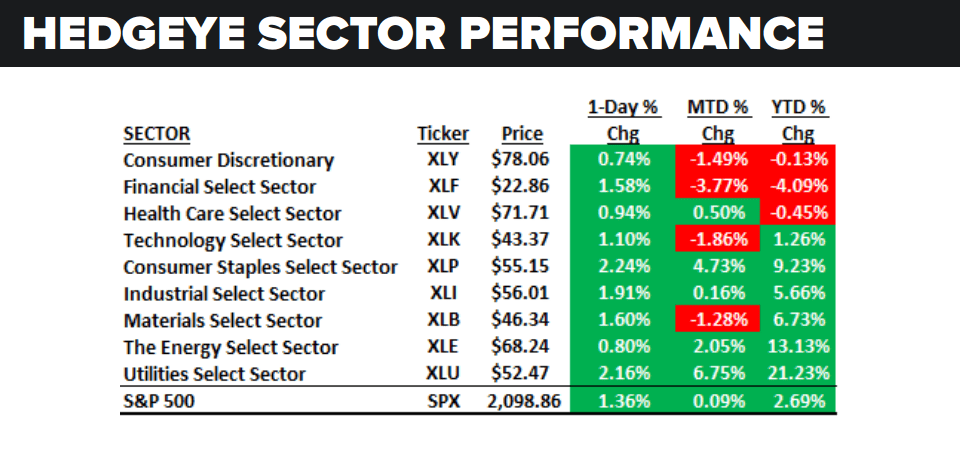

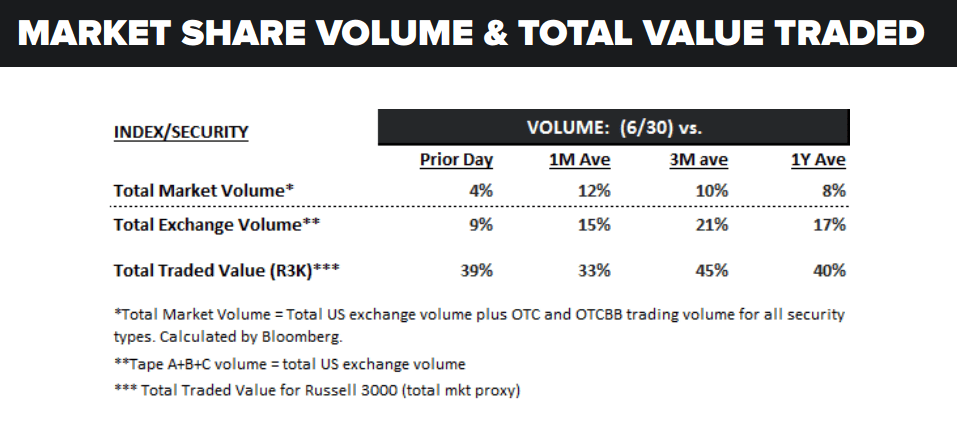

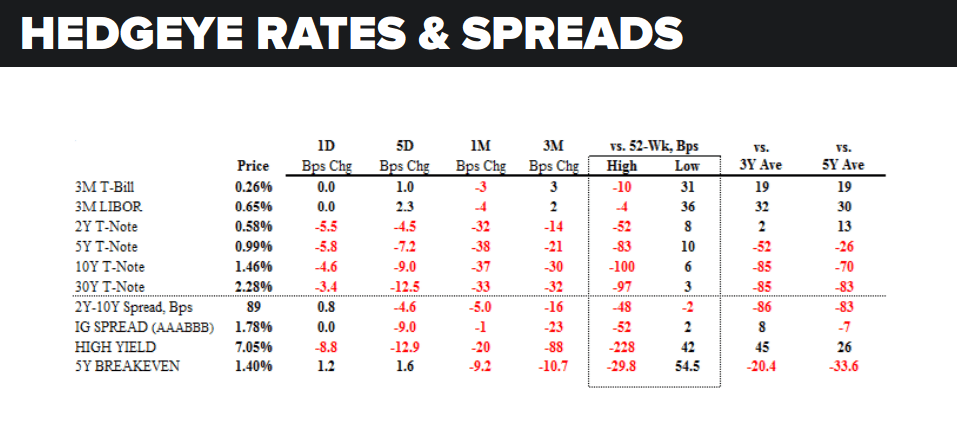

Editor's Note: Below are complimentary charts highlighting global equity market developments, S&P 500 sector performance, volume on U.S. stock exchanges, and rates and bond spreads. It's on the house. For more information on how Hedgeye can help you better understand the markets and economy (and stay ahead of consensus) check out our array of investing products.

CLICK TO ENLARGE