Editor's Note: Hedgeye Financials analyst Jonathan Casteleyn was on The Macro Show this morning discussing Brexit, European equities and a number of his high-conviction long and short calls. Below is an abridged transcript from today's episode in which Casteleyn explains why investors in European equities should "avoid the whole region."

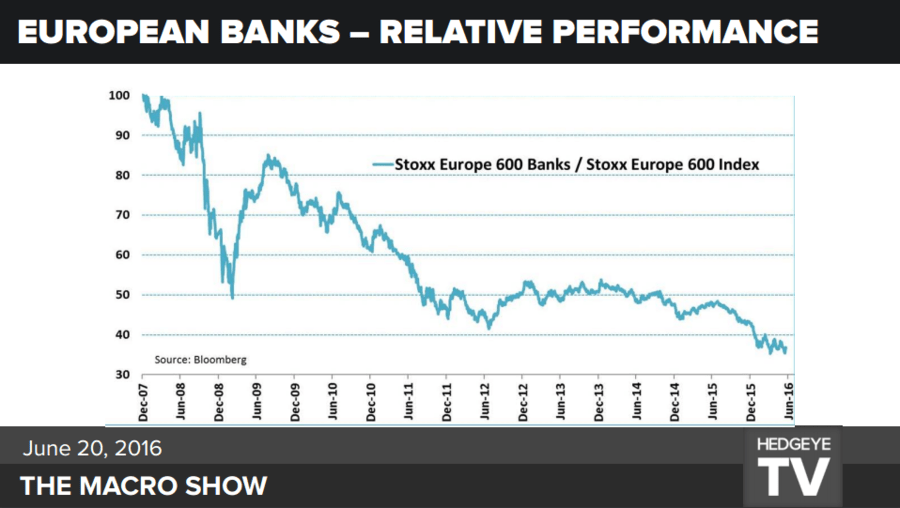

“This is what I think we should be talking about in Europe. The region is actually really unappealing as you can see in this time series of European bank stocks [see below].

Out of the 2008-2009 Financial Crisis, you saw a slight rebound in the banking sector but there’s been no recovery. Rates are down, growth is down, deflation is moving into the economy and there’s been no rebound in financial company profits. Essentially, the banks are dis-incentivized to make loans because they can’t do it profitably.

Remember, this chart has nothing to do with Brexit and is proof that the financial sector is not a place to invest. Since credit is the lifeblood of the economy, the pull forward of consumption, Europe is in massive distress.

We just want to avoid the whole region.”