"Thank goodness for no Brexit - we were running out of global equity bull market catalysts!" Hedgeye CEO Keith McCullough wrote in a note to subscribers this morning.

European equity markets surged on the news that Brexit polling showed a "resurgence" of the "Remain" camp. Here's the latest from MarketWatch:

"An opinion poll by Survation for newspaper the Mail on Sunday showed 45% in favor of remaining and 42% in favor of leaving. That telephone poll was conducted Friday and Saturday, after the killing of British politician Jo Cox. It shows a swing back to “remain,” as a previous survey conducted on Thursday by Survation had put Brexit in the lead by 3 points."

But take a look at the latest aggregate polling below, which shows "stay or leave" odds at essentially a coin toss (with 11% of the electorate undecided heading into Thursday's vote):

Here's additional Brexit analysis from McCullough:

"FTSE: +2.6% (DAX +3.3%) in a straight line to 6172 with intermediate-term TREND line up at 6335; anything that isn’t closed in Global Equity markets doing the same so they better not Brexit!"

"Big pop for Pound vs. USD of +1.8% taking it right back to where it’s been twice now (1.46-1.47) in both April and May; can it hold? Sure. Can it do this every day? Doubt it. Everything reflation should love it today regardless (Dollar Down)"

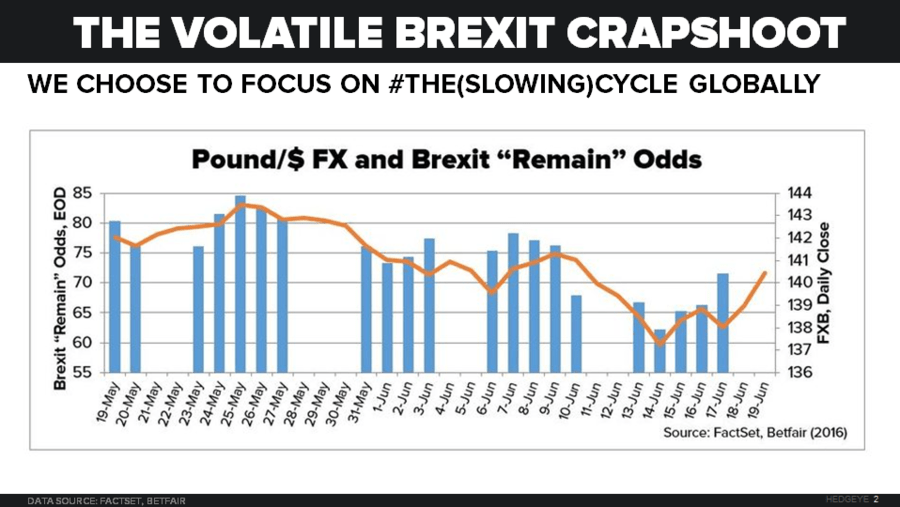

Finally, take a look at today's Chart of the Day, which shows the Pound/U.S. Dollar fluctuations tightly tracking Brexit "Remain" odds.