Our cartoonist Bob Rich captures the tenor on Wall Street every weekday in Hedgeye's widely-acclaimed Cartoon of the Day. Below are his five latest cartoons. We hope you enjoy his humor and wit as filtered through Hedgeye's market insights. (Click here to receive our daily cartoon for free.)

Enjoy!

1. Bear Grillz (6/17/2016)

For investors bearish on U.S. economic growth, like us, Gold is having an amazing run this year. Year-to-date, Gold (GLD) is up 21.7% versus up just 1.4% for the S&P 500.

2. Brexit (6/16/2016)

A few catalysts to keep an eye on:

- The Fed (Yellen went dovish yesterday and equities turned red on that into the close)

- Brexit (what if they do exit?)

- Mean Reversion and performance chasing

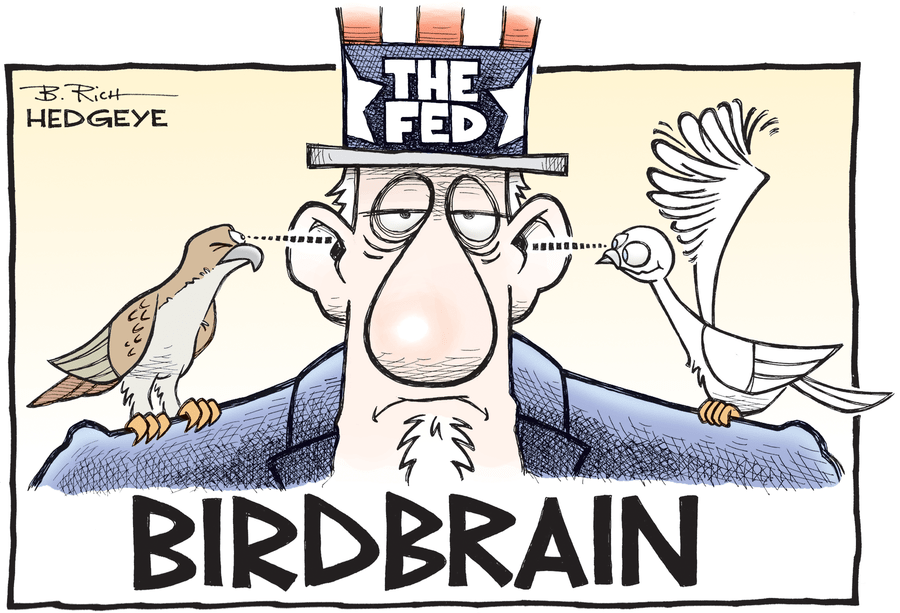

3. For The Birds... (6/15/2016)

"Fed 'data dependence' or absolute mediocrity in forecasting?" Hedgeye CEO Keith McCullough wrote following today's FOMC statement. "The Fed was hawkish in December, dovish in March and April, hawkish in May and now dovish again in June."

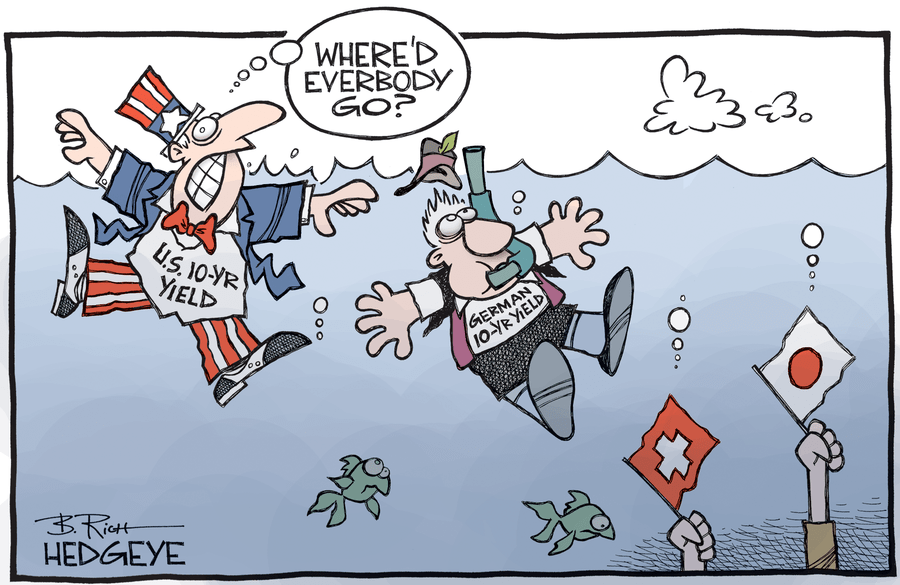

4. An Update On Global Bond Yields (6/14/2016)

The yield on the 10-year German Bund hit an all-time low today falling into negative territory for the first time ever. Global sovereign bond yields continue to make new lows as #GrowthSlowing fears persist.

5. Living In A Bubble? (6/13/2016)

Last week, hedge fund titan George Soros grabbed headlines after it was announced he had come out of semi-retirement and placed bearish bets, shorting the S&P 500 and buying gold.