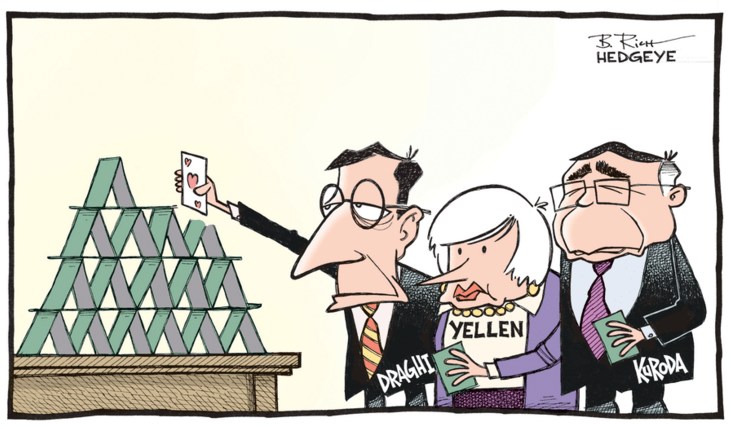

It's happening.

Make no mistake. The #BeliefSystem that central planners can arrest economic gravity is breaking down. That's what we said in our 80-slide 2Q Macro Themes deck, released in April, and that's precisely what's playing out in macro markets today.

Despite dovish Fed rhetoric yesterday, the U.S. dollar is strengthening and equity markets are selling off, in direct opposition to Yellen & Co's intent.

Meanwhile, policymakers at the Bank of Japan have watched the Yen strengthen today too, with the JPYUSD cross hitting year-to-date highs, and the Nikkei self-destructing (it lost 3% today alone).

Keep in mind that Yen strength came after the BOJ announced today that it will continue to conduct open market operations at an annual pace of 80 trillion yen ($760 billion) and is maintaining its negative interest rate policy.

Here's additional analysis from Hedgeye CEO Keith McCullough in a note sent to subscribers earlier today:

"They’re really out on the central banking #BeliefSystem in Japan – on the heels of reiterating 80T (T = Trillion Yen), the Yen ramped +1.7% (vs USD) to yet another YTD high, and the Nikkei continued to crash, -3.1% overnight (-7.2% on the week) and -26.1% from last year’s cycle peak in Global Equities (July)"

Take a look at a chart of the Yen:

And here's the Nikkei crash. Not good...

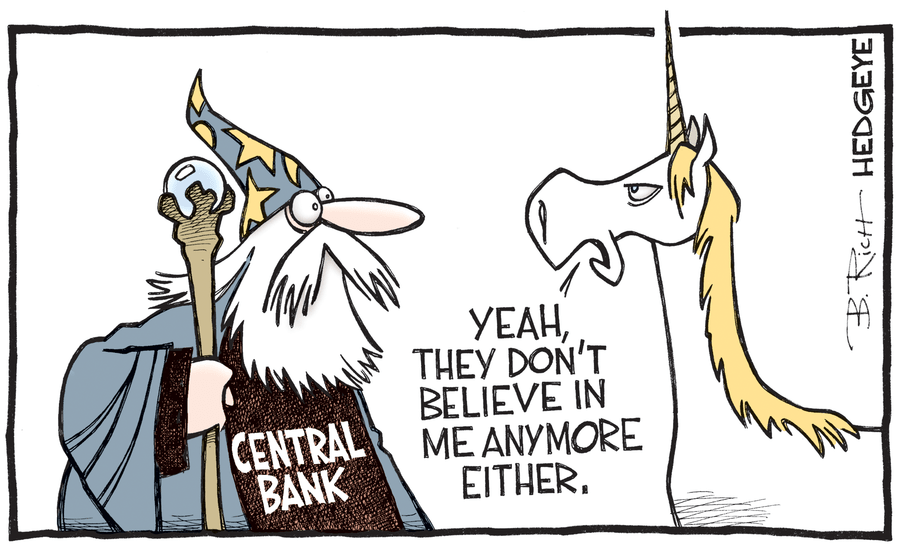

Need to understand the #BeliefSystem breakdown fast?

Here's the full description from our 2Q Macro Themes deck:

Click to enlarge

We're reiterating that call this morning.

We'll leave you with this brief message from CEO Keith McCullough:

More to come.