We've been hearing for a while now, from various pundits and prognosticators, that "global demand has bottomed." The problem with that argument is that it just isn't born out by the facts.

Setting aside that economic indicators around the world are rolling over, simply looking at the massive drawdowns in global equity markets could satisfy even a casual observer's curiousity that all is not well.

Here's analysis from Hedgeye CEO Keith McCullough in a note sent to subscribers earlier this morning:

"I know. When trying weave the “global demand has bottomed” narrative about US stocks, you have to ex-out things like Japanese and German Equities (and their bond yields hitting all time lows) – small details I’m sure, but both Nikkei and DAX down another -1% today and down -20% and -19%, respectively, from last year’s highs."

Take a look at the Nikkei...

And Germany's DAX...

Clearly, global demand has not bottomed...

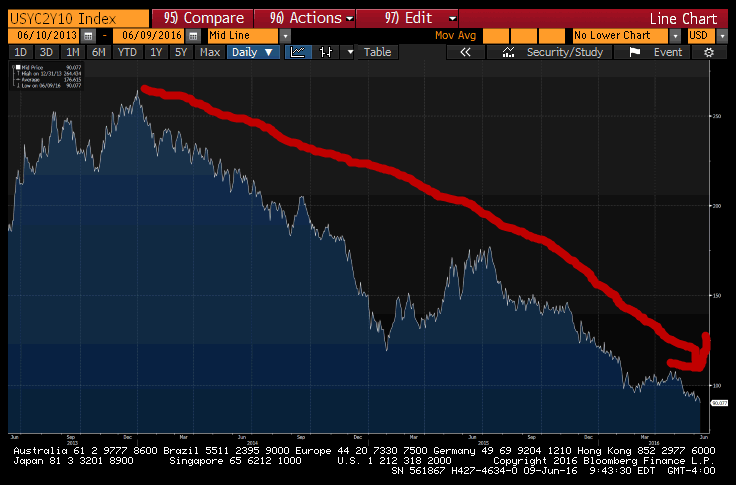

Here's the most obvious #GrowthSlowing indicator. The 10yr to 2yr Treasury yield spread is pancaking, with the yield on the 10yr at 1.669% this morning.

More to be revealed.

(FYI: Our biggest Macro call, Long Bonds (TLT) is breaking out to new highs today.)