Its that time of year again.

Earnings season is upon us and, by just about every estimation, companies are due to report lackluster results on the top and bottom line.

Here's what you need to know via our Macro team in a note sent to subscribers earlier this morning:

"With 39 S&P 500 companies having reported Q1 earnings to date, sales growth is down -1.1% year-over-year and earnings growth has slowed to -11.8% year-over-year -- which would be the worst annual growth rate of the cycle if it holds through the rest of reporting season. Declines are being led by Materials (-34%), Tech (-20%) and Financials (-17%).

Compounding matters is the 25-30% spread between pro forma and GAAP, which continues to be reflected in a rising economy-wide debt-to-free-cash-flow ratio. Specifically, that ratio just reached 4x in 4Q15, which is the threshold it breached in 3Q07 on its way to peaking at 4.6x in mid-2008. We reiterate our view that neither the corporate profit nor credit cycles have seen their respective depths."

REMINDER

If the current earnings data holds, this would be the third quarter of contracting corporate profits.

WHY IT MATTERS

Our Macro team continues to highlight that when corporate profits decline for two consecutive quarters or more the S&P 500 declines by at least 20%.

Click chart below to enlarge

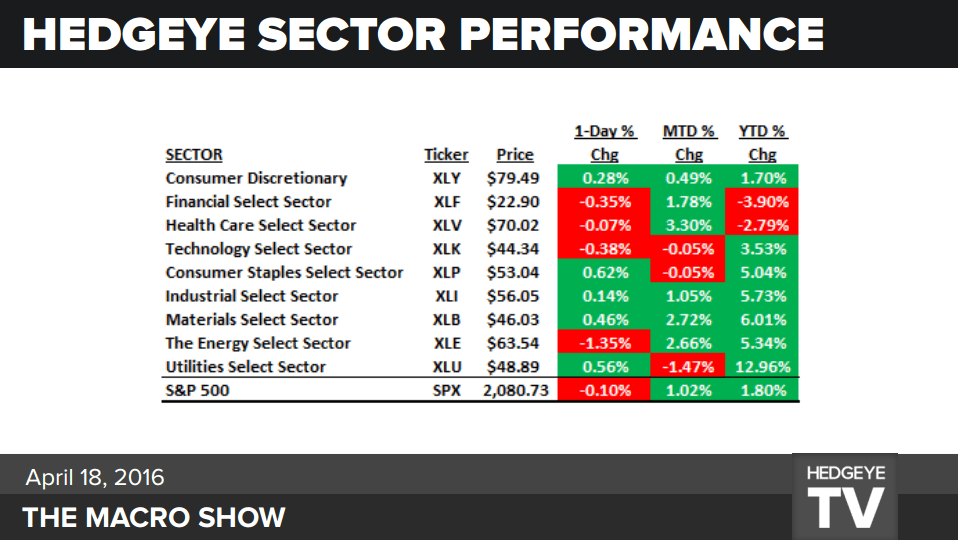

Performance? Where We're at...

In spite of truly ugly S&P 500 earnings in the last couple quarters, equities have rallied significantly off the February lows. However, this doesn't change our market views. We remain steadfastly bearish. Even with the recent pop, our favorite sector longs (Utilities, XLU) & shorts (Financials, XLF) continue to outperform. Here's the year-to-date scorecard: