Key Takeaway:

The reflationary bounce that took hold February 12th persists, in spite of generally weak economic data from the U.S. and profit pressures at J.P. Morgan, Bank of America, and Wells. Bank CDS tightened globally, while the YTM on high yield fell -33 bps to 7.60%.

Our heatmap below is positive on the short term, negative on the intermediate, and mixed on long-term readings.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 5 of 13 improved / 1 out of 13 worsened / 7 of 13 unchanged

• Intermediate-term(WoW): Negative / 4 of 13 improved / 5 out of 13 worsened / 4 of 13 unchanged

• Long-term(WoW): Negative / 2 of 13 improved / 2 out of 13 worsened / 9 of 13 unchanged

1. U.S. Financial CDS – Swaps tightened for 12 out of 27 domestic financial institutions. Even with JPM, BAC, and WFC reporting sliding profits last week, their CDS tightened by -7 bps to 69, -8 bps to 98, and -5 bps to 58 respectively.

Tightened the most WoW: MS, MTG, JPM

Widened the most WoW: PRU, MET, LNC

Tightened the most WoW: LNC, JPM, GS

Widened the most MoM: MET, PRU, AIG

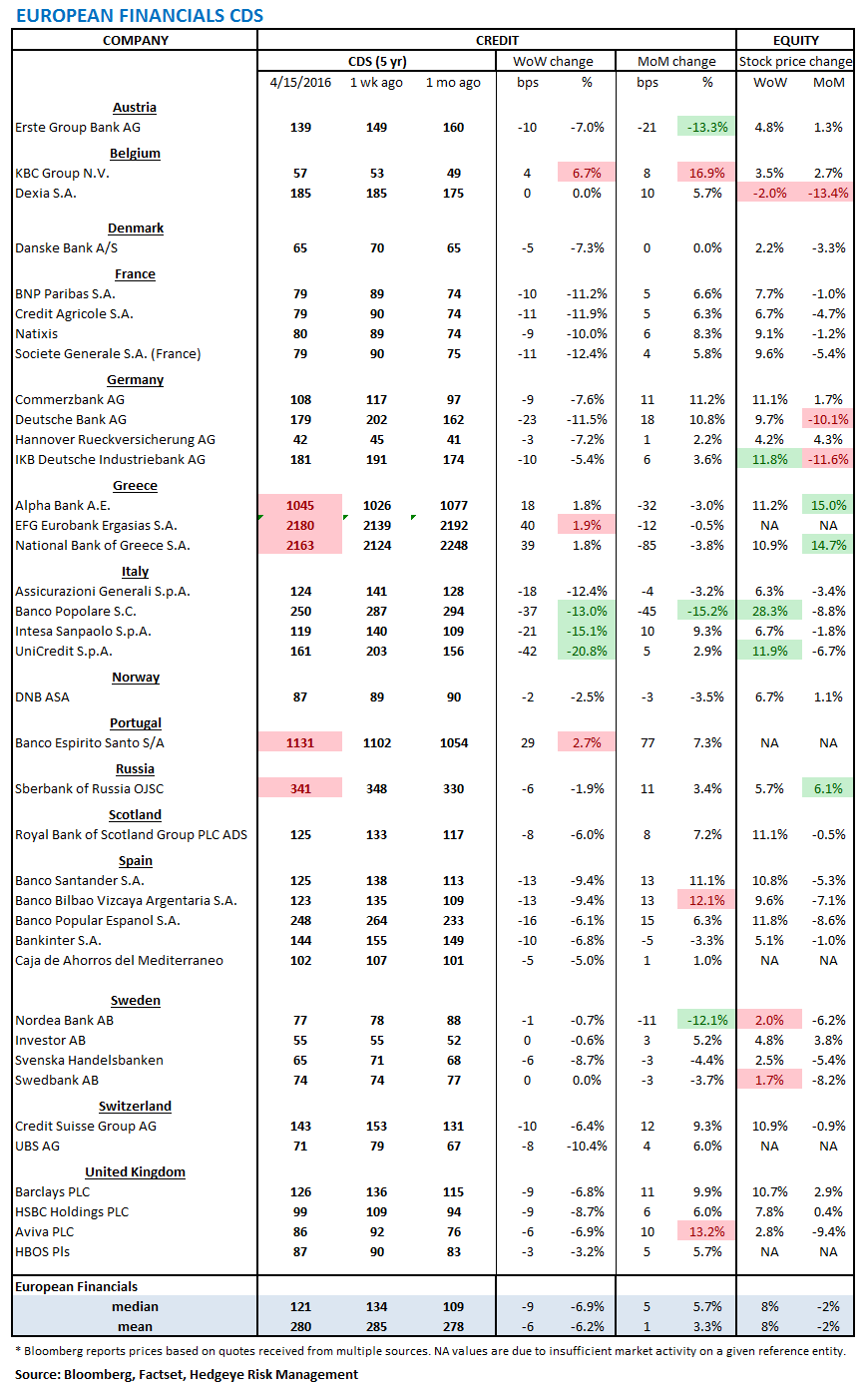

2. European Financial CDS – Swaps mostly tightened in Europe as investors clung to optimism last week. The median spread tightened by -14 bps to 121.

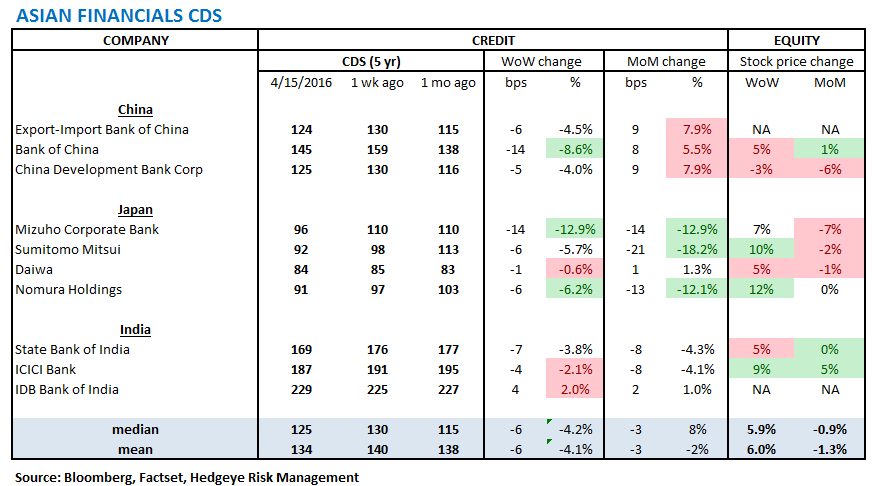

3. Asian Financial CDS – Swaps tightened nearly across the board in Asia last week. IDB Bank of India was the only one to widen, by 4 bps to 229. Even Chinese swaps tightened, where data released last week showed 1Q16 economic growth slowing to 6.7%, the slowest quarterly growth since 2009.

4. Sovereign CDS – Sovereign swaps mostly tightened over last week. Italian and Spanish swaps tightened the most, by -7 bps to 129 and by -7 bps to 93 respectively.

5. Emerging Market Sovereign CDS – Emerging market swaps mostly tightened last week. In Brazil, where a congressional committee recommended that President Dilma Rousseff be impeached, swaps tightened by -48 bps to 342.

6. High Yield (YTM) Monitor – High Yield rates fell 33 bps last week, ending the week at 7.60% versus 7.93% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 13.0 points last week, ending at 1871.

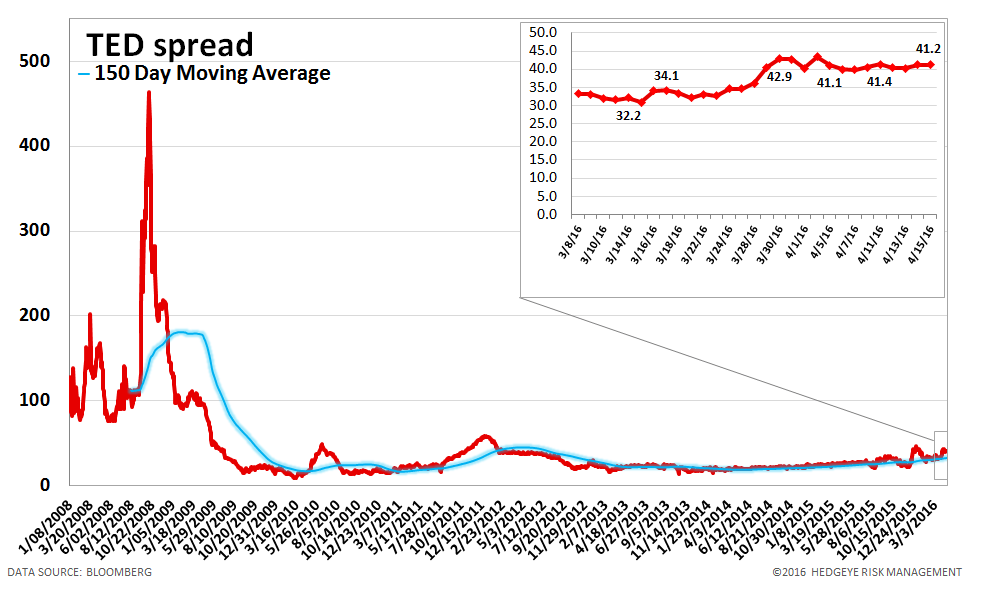

8. TED Spread Monitor – The TED spread rose 1 basis points last week, ending the week at 41 bps this week versus last week’s print of 40 bps.

9. CRB Commodity Price Index – The CRB index rose 3.6%, ending the week at 174 versus 168 the prior week. As compared with the prior month, commodity prices have decreased -1.5%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 10 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 2 basis points last week, ending the week at 2.00% versus last week’s print of 1.98%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China rose 8.7% last week, or 229 yuan/ton, to 2,852 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. Chinese Non-Performing Loans Chinese non-performing loans amount to 1,274 billion Yuan as of Dec 31, 2015, 51.2% higher year-over-year.

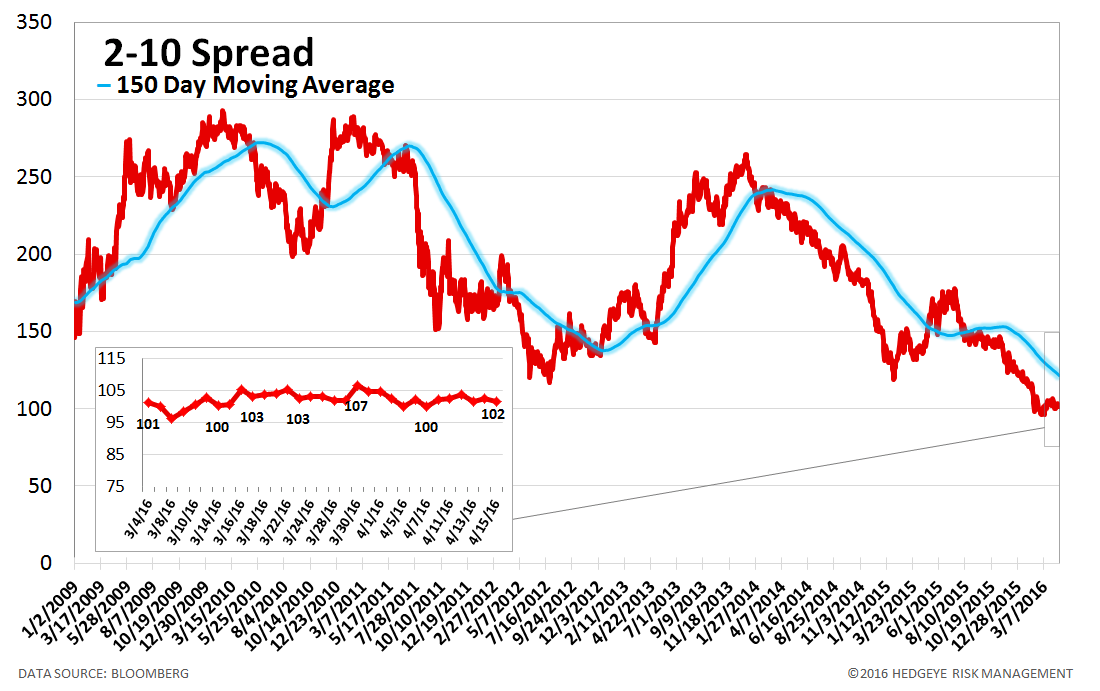

14. 2-10 Spread – Last week the 2-10 spread was unchanged at 102 bps. We track the 2-10 spread as an indicator of bank margin pressure.

15. CDOR-OIS Spread – The CDOR-OIS spread is the Canadian equivalent of the Euribor-OIS spread. It is the difference between the Canadian interbank lending rate and overnight indexed swaps, and it measures bank counterparty risk in Canada. The CDOR-OIS spread was unchanged at 41 bps.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT