Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

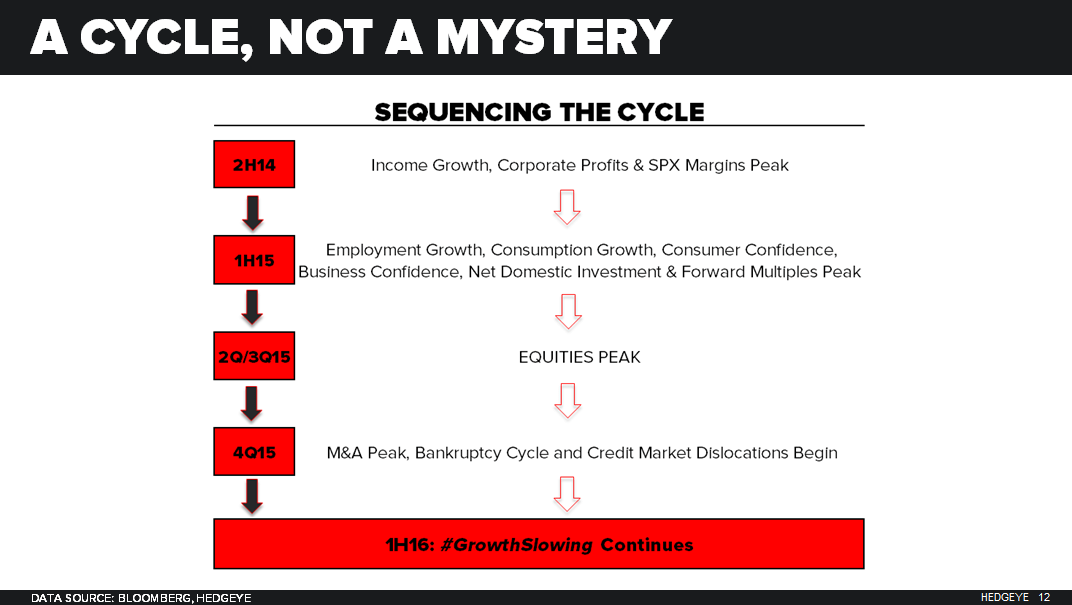

"... As Yellen and her colleagues who now read @Hedgeye Macro can see in today’s Chart of The Day (slide 12 of the Q2 Macro Themes deck), #TheCycle is not a mystery. This one has been both obvious and pedestrian in its sequence:

- Q2 2014 = Income Growth, Corporate Profits, and S&P 500 Margins #peaked (in rate of change terms)

- 1H 2015 = Employment & Consumption Growth, Confidence, Domestic Investment, and Multiples #peaked

- Q2/Q3 2015 = US Equities Peaked

- Q4 2015 = M&A #Peaked and the #CreditCycle (and market dislocations) began

- 1H 2016 = #GrowthSlowing from #TheCycle peak (in rate of change terms) continues"