Think first quarter earnings are growing gangbusters? Think again.

Here's the latest from our Macro team in a note sent to subscribers this morning:

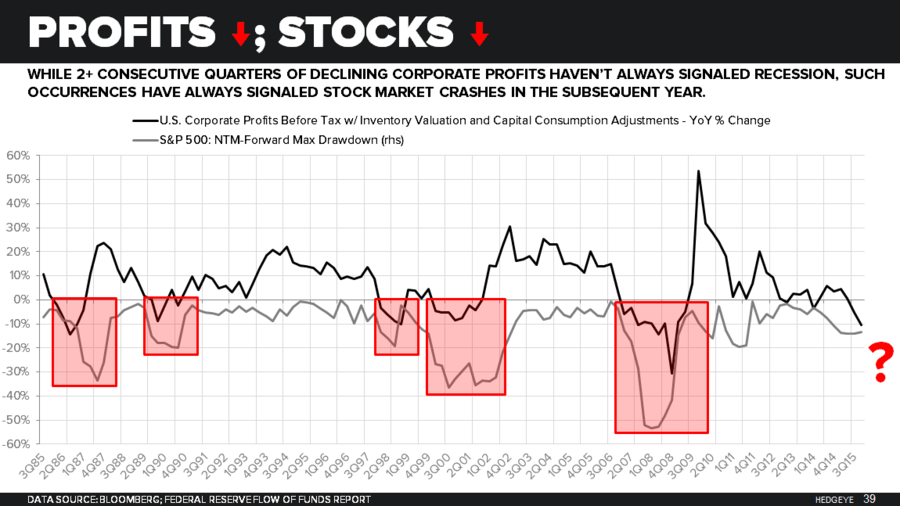

"Q1 earnings season kicks-off next week with the bulge bracket banks leading the way (JPM next Wednesday). If you think we’ll follow-up an awful Q4 2015 reporting season (S&P revs -4.0% Earnings -6.9%) with a rebound, think again. We won’t be lapping bad comps until at least Q3 of this year (reported in Q4). In Q1 of 2015, 8/10 sectors saw Y/Y earnings growth, and the one sector with awful earnings was energy, where WTI averaged $48.57 vs. $33.63 in Q1 0f this year. Don’t get excited about Q1 earnings season. It will be more of the same. #thecycle."

Here's the chart highlighting why all of this is so significant.