Video REPLAY

Audio REPLAY

Link to MATERIALS

We hosted a Best Ideas Short call on shares of T. Rowe Price (TROW) yesterday. While a well managed, disciplined investment manager, the secular shift to ETFs and mostly importantly to Large Cap strategies is too pervasive for the firm to meet the Street's expectations in our view. In addition, this predominately equity mutual fund manager is at the wrong part of the cycle operating at peak margins and peak profits with the growing potential for a long overdue market decline to kick off negative operating leverage. The firm has unappreciated equity leverage in its most important product, its target date fund franchise with its "through" asset allocation. Our key takeaways are:

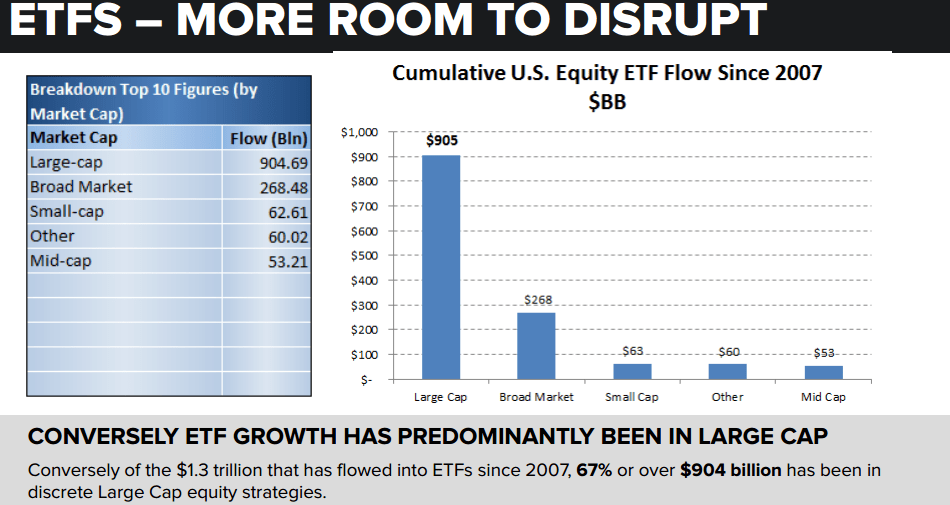

1.) The shift from active to passive continues to accelerate and 67% of passive inflows are going to Large Cap strategies. TROW has the largest percentage of Large Cap product of any public mutual fund manager and when including SMAs, TROW's Large Cap exposure goes to over 40% of total assets-under-management:

2.) The firm's Target Date franchise is its go to source of growth, however the oldest Baby Boomers turned 65 in 2011 and now three Series of TROW target date products are in redemption. The hump gets worse in the distribution into the 2020 series which is the second biggest pool of TD assets for the manager. Target date is the only source of growth currently in the overall complex.

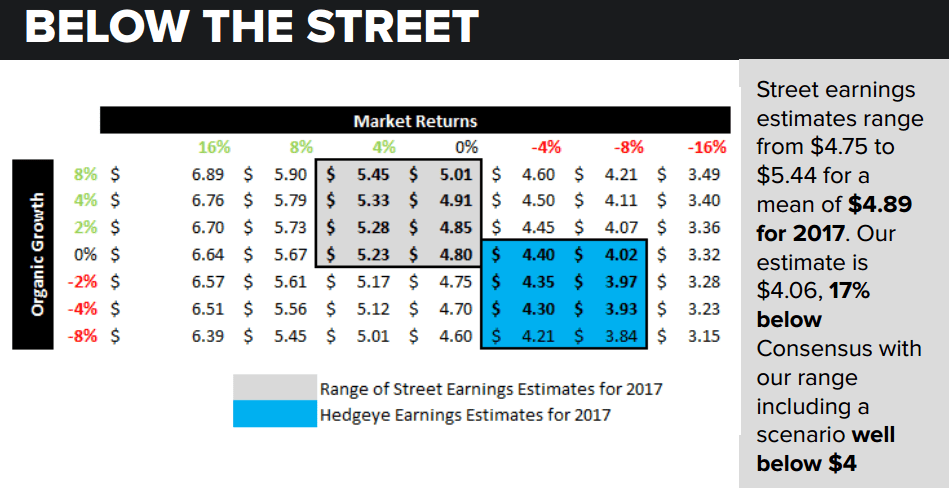

3.) TROW is once again at peak margins and profitability and after setting a new high water mark in 2014 at over 50% pretax margins, results are set to recede. TROW will also be bumping up against a break point in fees at over $500 billion in mutual fund AUM which won't help margins. We have earnings at $4.06 for 2017, -17% below the Street before considering that the stock's multiple should also contract against the group.

Please let us know of any questions.

Jonathan Casteleyn, CFA, CMT