We added HBI to our short list yesterday. We don’t like the Brands, don’t like Management, and don’t like the Company, but that alone is no reason to short a Stock. What is, however, is the fact that we think that earnings and margins are at peak. We’re 7% below consensus this year, -20% in ’17, -30% in ‘18, and -40% by year 3. Some argue that stock might seem cheapish today at a mid-teens multiple and 5% FCF Yield – though we really don’t follow that logic. Once the dust clears from the acquisitions, special charges, and cotton prices normalize from the 7-year low, we think we’ll be looking at lower multiples on lower earnings and cash flow. A low double-digit multiple on our numbers gets us to a high-teenager. We don’t like high teenagers. Perhaps management agrees, especially CEO Noll who has cut his stake in half over four months.

Here are some factors to consider…

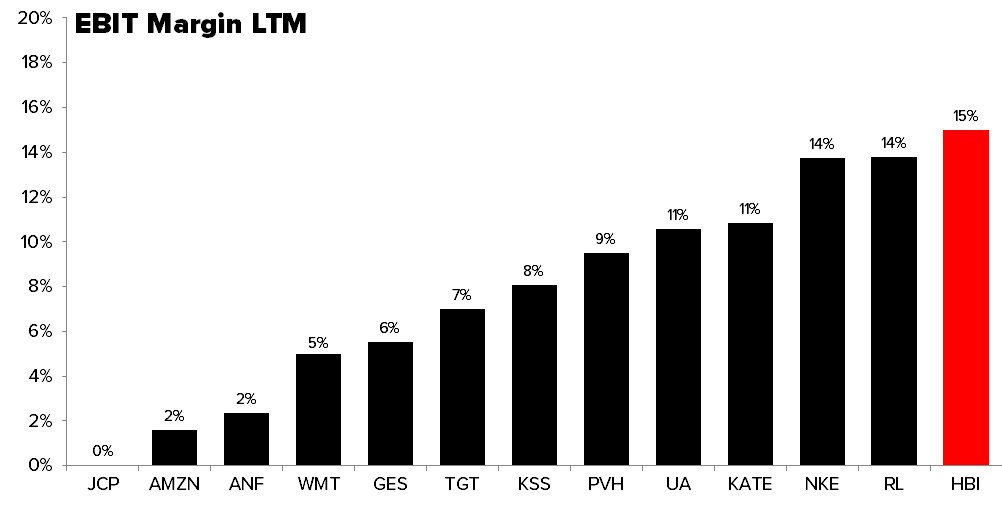

1) Why? Can someone, ANYONE, explain to me why HBI has operating margins of 15%? That’s demonstrably higher than the following companies – UA, RL, PVH, GES, CRI, ANF, KATE, and yes – even NKE. It’s also well above its key retailers (WMT, TGT, KSS, JCP, AMZN). Why should a company whose primary brand sells through mass channels and department stores have higher margins than the best brands in the business? As hard as we try, we cannot figure it out aside from over-earning due to a 7-year trough in cotton prices and the temporary benefit of being a serial acquirer and restructurer of companies in an effort to grow away from its core.

2) Let’s consider how the margin structure changed at HBI over the past 4-years. Cotton peaked in the market at about $2.00 in 2011, which ultimately flowed through and hit HBI’s margins in 2012. That was when the stock was at a split-adjusted $5. Overly penalized, for sure. But we’d argue we are seeing the inverse today. Since the precipitous decline in cotton to the $0.57 level we see today (a 7-year low and near a 20-year low), HBI recouped seven (7) full points in Gross Margin. Over the same time period, how much did the company see flow through to EBIT margin? Seven. Ordinarily, we’d like to see a company invest more of the upside. They’ll say they ‘innovate to elevate’. But we’ll bet there’s a direct flow through in margin downside if either a) cotton prices head higher, or b) if Wal-Mart and Target decide that HBI is making too much money.

3) Buying at the Top? HBI buying so much stock when margins are at all-time peaks (and management is selling) comes across to us as flat-out reckless. In fairness to HBI management, we see this behavior from most major consumer companies – they buy stock when they CAN and not when they SHOULD. This is not unlike Target, which is taking the incremental $1.2bn it gained from its pharmacy business and using it to buy back shares at $80. Our sense is that it will come back to haunt them if we’re right on earnings and this stock is in the high teens.

4) Acquisition Behavior Bothers Us. This company has acquired an average of a company a year for 5-years for a total of $1.5bn. It’s also taken $546mm in restructuring charges, or 25% of non-GAAP EBIT, since the Maidenform acquisition in October 2013.

5) As hard as it might try, HBI can simply not grow online. If there was only one statistic we could see for a consumer brand to gauge the health of its business, it would be the direct to consumer (DTC) sales of its product. DTC sales at HBI, however, have shrunk as a percent of sales over the past 5 years from 9.5% to 6.8%. We’ve never seen a company do that before. Our sense is that WMT, TGT, the Department Stores, and Dollar Stores all would react severely if HBI tried to go direct. And yes, we understand that WMT and AMZN sell Hanesbrands online, which counts as a wholesale sale on the P&L but shows up online. It does not matter. Margins are better for a direct sale full-stop. We refuse to accept the premise that underwear is not a category that lends itself to online sales. Tell that to Tommy John, Lululemon, and UnderArmour, who all have 30-40%+ online businesses and are charging $30-$40 per pair (not package), and they can hardly keep them in stock. It’s abundantly clear where the trend is going – and HBI can innovate all it wants, but it’s likely not going to be a player in this premium game.

6) When management buys a share of stock, we’ll step back and question our logic (though we’ve done that a few times already). We have seen an absolutely massive degree of selling from the management team over the past year – see Rich Noll’s selling activity below. Specifically, he has sold $85mm in stock over the past 14 months, most of that +/- $2 of where it is trading today.