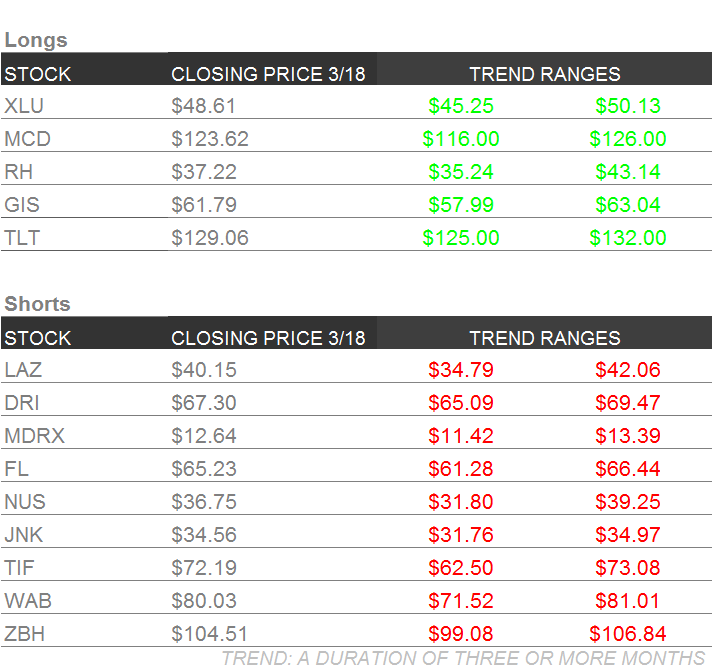

Below are our analysts’ new updates on our fifteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

Please note that we removed Wayfair (W) from the short side of Investing Ideas this week.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | ZROZ | JNK

To view our analyst's original report on Junk Bonds click here, here for Utilities and here for Pimco 25+ Year Zero Coupon US Treasury ETF.

If the Fed’s backing off of rate hikes due to “external” factors (interpreted “ex. U.S.”) signaled anything, it’s that growth expectations have been taken down. Ask the bond market:

- The 10yr yield declined -6bps on Fed day and finished -10bps on the week

- Long-Term Treasuries (TLT) finished +1.9% on the week

- Pimco 25+ Year Zero Coupon US Treasury ETF (ZROZ) finished +1.7% on the week (we added ZROZ to investing ideas last Friday as it is most sensitive to lower long-term yields moving lower)

- Junk Bond ETF (JNK) finished +67bps higher on the week (relative underperformance vs. TLT)

- Utilities (XLU) hasn’t bounced as much as leveraged , high-beta resource names, but the outperformance is greatly divergent vs. both the market, and our preferred sector short in financials (XLU +12.3% YTD, S&P -0.3% YTD, XLF -4.6% YTD)

Aside from Mr. Market, the Fed downwardly revised expectations (the common lag) on Wednesday:

- The median 2016 GDP forecast revised to +2.2% vs. +2.4% in December

- The median 2016 PCE Inflation forecast revised to +1.2% vs. +1.6% in December

- Median Federal Funds end-2016 rate forecast revised to 0.9% vs. +1.4% in December

From a GROWTH, INFLATION, POLICY perspective, it’s lower for longer on growth and inflation and a more dovish Fed.

So is growth still slowing? Let’s dissect the preponderance of recent data as highlighted by Hedgeye Macro Analyst Christian Drake in Friday's Early Look note...

- Past Peak: Corporate profit, labor, income, consumption, confidence and credit cycles are all in their expansionary twilight.

- Industrial production: accelerated to the downside (-1.0% YoY) in Feb.

- HMI & Housing Starts: Builder Confidence held at a 9-month low in March and Housing Starts, despite sequential improvement, have been flat for 10-months. (& Spoiler: Existing Home Sales should be negative on Monday)

- Retail Sales: Headline retail sales were negative M/M for a second month in February

- Inventories: Inventories again grew at a premium to sales in the latest January data, sending inventory-to-sales ratios across the supply chain to new highs. Note: Unless companies are successfully foreshadowing accelerating demand, excess inventory = lower future profitability at the corporate level (discounting to move supply) and lower growth at the aggregate level (lower inventory build drags on Investment growth)

Now for the positive data, at least from a policy perspective (remember the Fed’s dual policy mandate is inflation and full employment):

- Employment: The unemployment rate is 4.9%, and the labor force participation is showing some multi-month mojo and labor slack continues to diminish.

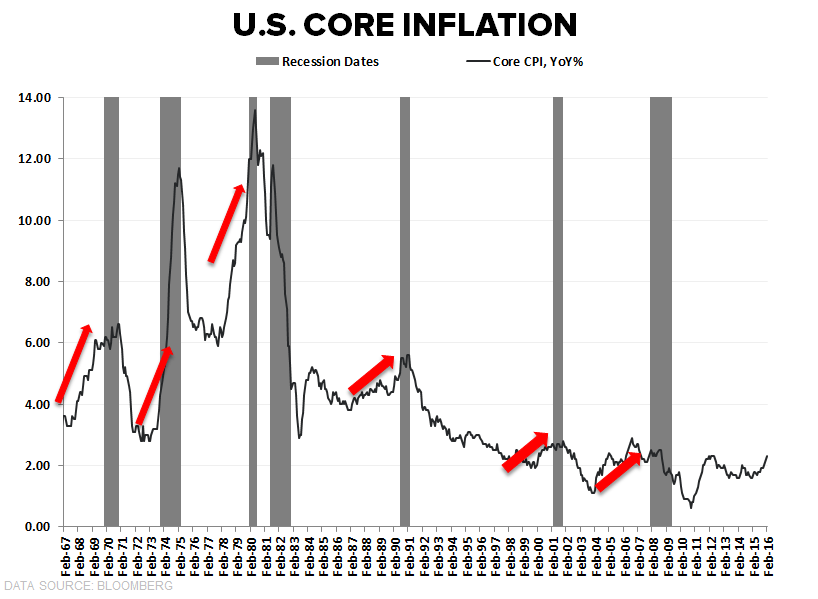

- Inflation: Core CPI Inflation accelerated for a 9th straight month, making a new 45-month high at +2.3% YoY in February. And while Shelter inflation (33% weighting in the Index) made a new high at +3.28% Y/Y and continues to backstop headline growth, Services ex-shelter accelerated to a 13-month high. Meanwhile, Core Goods (i.e. commodities less food & energy) inflation - which depends more on short-run inflation expectations, currency impacts and import prices – went positive (+0.1% Y/Y) for the first time in 3 years and will be broadly interpreted as strong dollar impacts burning off. Moreover, the pickup in core and ex-shelter price growth – and in Medical Care specifically (which carries a significantly higher weighting in the PCE price index than the CPI index), suggests inflation in the Fed’s preferred Core PCE inflation reading will continue its path higher.

We would argue that excess inflation in key consumer cost centers (rent/housing & healthcare as described above) steals share of wallet from discretionary consumption. The most important point to emphasize here with respect to recent employment and inflation data is that inflation is the most lagging of indicators and cresting employment + rising inflation classically characterizes the last part of the cycle. This is nothing different from what we have said before with regards to the late-cycle labor market, and here are a few visuals that empirically support our view:

MDRX

To view our analyst's original report on Allscripts click here.

No update on Allscripts (MDRX) from our Healthcare team this week. But analysts Tom Tobin and Andrew Freedman did briefly discuss MDRX while addressing a number of important trends impacting their sector during a recent HedgeyeTV video. Topics included:

- This week's JOLTS data

- Update on MEDNAX (MD)

- Key takeaways from their proprietary maternity tracker

- And what's next for Valeant Pharmaceuticals (VRX)

It's a must-see video for investors looking to contextualized the trends in Healthcare. (Note: Healthcare (XLV) is the worst performing S&P 500 sector year-to-date).

Click here to watch the video.

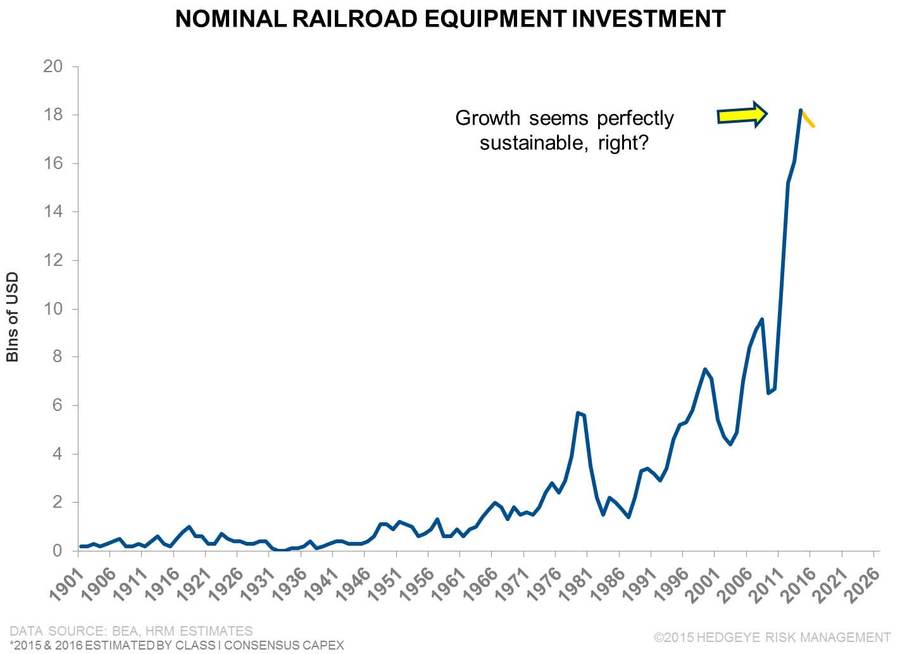

WAB

To view our analyst's original report on Wabtec click here.

We would look to use the recent squeeze as an entry opportunity, although we acknowledge the risks of adding to a position that has moved against us of late. We expect rail capital spending to turn down given fleet demographics and customer volume trends. We still expect Wabtec (WAB) to earn well less than $4 per share in 2016, with weak 2H15 implied order rates as one several supporting data points for that view.

NUS

To view our analyst's original report on Nu Skin click here.

No update on Nu Skin (NUS) from Hedgeye Restaurants analyst Howard Penney this week. However, while you wait for next week's update, Penney and analyst Shayne Laidlaw discussed a number of key trends facing the Consumer Staples industry including other high-conviction ideas in the sector during a recent HedgeyeTV video.

Click here to watch the video.

TIF

To view our analyst's original report on Tiffany click here. Below are the key takeaways from Tiffany's (TIF) earnings report this week:

Demand Issues

The underlying slowdown in demand is a big concern. US census reported jewelry store sales up 2.5% in calendar Q4, yet TIF comped -8% in $C in the Americas.

Management Guidance Credibility

Guidance was revised down again. Management has downwardly adjusted their annual outlook in 6 of the last 7 guidance updates. We expect another guide down in 2016.

Re-Investment Needed

We believe the company needs a serious capital plan to re-invest in the brand to drive long-term growth. The incremental $7mm in capex planned for 2016 is nowhere near enough. Either we get a big strategic investment, reset expectations and properly align this brand for growth, or TIF growth remains stagnant.

Takeaway: Despite a headline adjusted EPS beat, the quarter was ugly, management is losing credibility, the brand is becoming less relevant, and we may be in the early innings of a consumer slowdown. We're getting increasingly bearish on this model and remain short.

Click here to watch a brief video on TIF's earnings.

LAZ

To view our analyst's original report on Lazard click here.

Lazard (LAZ) shares had a good week, rallying in tandem with both U.S. and Emerging Markets (EM). We continue to estimate that the upward rebound in risk assets is temporary, or a bear market rally, as economic fundamentals remain weak within the framework of a late cycle U.S. and Global economy. Lazard understates its emerging markets exposure with more EM strategies in its Global and Regional segments than investors realize.

Thus, when EM markets again readjust downward, LAZ shares will again underperform the Financial sector and other asset management complexes. EM markets are still hostage to historically low crude oil prices and also sovereign bankruptcy as Brazilian, Venezuelan, and Russia governments continue to “hang by a string” hoping for a more substantial rebound in energy. While crude is up over $10 per barrel recently, the energy complex is still down over 50%, which will make EM outperformance outside of this recent trading bounce difficult to sustain.

MCD

To view our analyst's original report on McDonald's click here.

Here's the bullish case for McDonald's (MCD) via our original stock report in August 2015:

"We are going to be looking at a much different company 1-3 years from now. Urgency has been instilled from the top down by new CEO Steve Easterbrook. He wants more speed and is encouraging people to get things done faster... All Day Breakfast, responsibly sourced ingredients, and bringing back the value proposition will lead to increased sales and customer satisfaction."

That's been showing up in MCD's numbers pretty much since August when we said, "2015 will be the last time this stock is below $100." Take a look at the chart below. Restaurants analyst Howard Penney nailed it:

MCD is up 24% since we recommended it to Investing Ideas subscribers, versus down -2.6% for the S&P 500. Stick with it here.

RH

To view our analyst's original report on Restoration Hardware click here.

Last weekend the new Restoration Hardware (RH) rewards program went live to customers. Called the Grey Card -- the key feature is 25% off all orders for a $100 annual fee. There are other benefits associated with the card: early access to sale events, preferred financing (w/ an RH Credit Card), and 10% savings on sale items. But the key benefit (outside of the discount), we think is access to RH's in-house Interior Designers at no additional cost.

Over the near term -- there is little doubt that the shift in promotional posture will make quarterly top-line results choppy as customers adjust to the new value proposition and the company laps meaningful promotional events. But, if we look at it over a slightly longer duration we think it will:

- Allow RH to get valuable insight on customer behavior as it analyses customer buying behavior through membership rewards data, and;

- Allow the company to smooth out the demand curve which will allow for greater efficiency from the vendor network and supply chain.

ZBH

To view our analyst's original report on Zimmer Biomet click here. Below is a brief update on Zimmer from Healthcare analyst Tom Tobin.

“I think, so our guidance of price decline in 2016 is essentially in line with what we saw in 2015, roughly 2% type price decline. The kind of the corollary to that is, does CJR in the United States have a dramatic impact on pricing, and we do not believe that to be the case in 2016, we understand across the whole episode of care that hospitals are going to be very focused on improving the quality and efficiency of care across the episode of care.” Daniel P. Florin Chief Financial Officer & Senior Vice President at the Barclay’s Healthcare Conference 3/16/2016

We spoke again to one of our orthopedic surgeon contacts this afternoon who helped us understand this Zimmer Biomet (ZBH) statement as only partly factual. The fact is that the CCJR, or the new CMS bundled payment “pilot” program now in place, will not have a “dramatic impact on pricing…in 2016.” We think what will be dramatic, in 2016, is the CCJR’s impact on case volume. Dramatic pricing pressure is something we and ZBH will have to wait until 2017 to see.

Near term, the CCJR will lead to case volume declines, as small volume community practitioners avoid sicker patients where they could lose large sums of money. According to our contact, the CCJR is already making it close to impossible for small hospitals to continue to offer joint replacement at all. Patients are being asked to get their diabetes, weight, or some other risk factor under control before the case is performed. Sicker patients make up as much as 20% of the patient volume in ortho, which means there is likely to be a big downward impact on case volume as the CCJR rolls out.

Our surgeon suggested small hospitals cannot afford to have a case go badly where they are responsible for all of the cost and will no longer offer large joint surgery. If our contact is correct, and we agree with him, small hospitals, which represent 20% of joint replacement volume, will be another headwind to case volume. Also, as these patient cases consolidate into the 43% of surgeries already performed at urban teaching hospitals, we’ll assume those large centers will be paying much less for their implants and -2% price declines will look like a distant and pleasant memory.

Our surgeon contact also confirmed for us (the first time we’ve heard this with specificity) that the ACA lead to a substantial increase in total joint volume in 2014 and 2015. The newly insured patients did not come to his high-end academic center, but instead were treated at the County Hospital. Further, instead of helping this marginally profitable system, the newly insured under the ACA have pushed the local County Hospital to the brink of insolvency. It turns out higher volume at unprofitable reimbursement rates is worse than a lower volume of unprofitable patients.

We’re reaching out to speak to the Chief of Orthopedic surgery at this County Hospital to hear more details on incremental case volume, and the impact to ZBH and other orthopedic vendors as our #ACATaper theme unfolds in the coming months.

Clearly management at ZBH is dismissing CCJR as an issue based on their comments this week, at least for the remaining 9 months of 2016. Meanwhile, the ACA hasn’t even come up on ZBH earnings calls or at their investor conference appearances. For the moment, we feel good that we are ahead of the curve about our ZBH short.

FL

To view our analyst's original report on Foot Locker click here.

Comp Trends:

We think comp sales at Foot Locker (FL) have hit a point where they are very likely slow in 2016. Below is a chart of the FL comp trend along with its 3-year average. If we assume a relatively consistent underlying 3-year growth rate, we get to a comp rate slowing to the low single digits in 2H16. If that should happen, the leverage of occupancy and SG&A is wiped away and earnings growth slows.

Combine slowing earnings growth with FL's increased capital spending plan announced a month ago and you get materially declining asset returns. Last we checked, stocks don’t go up when financial returns get cut in half.

GIS

No update on General Mills (GIS) this week, but the company remains one of analyst Howard Penney's top Long ideas in the Consumer Staples space. As we have continued to say, it boasts style factors ideal during turbulent times; high market cap, low beta and liquidity. Case in point, GIS is up 7% year-to-date, versus essentially flat for the S&P 500 in 2016.

We'll have an update next week after GIS reports earnings.

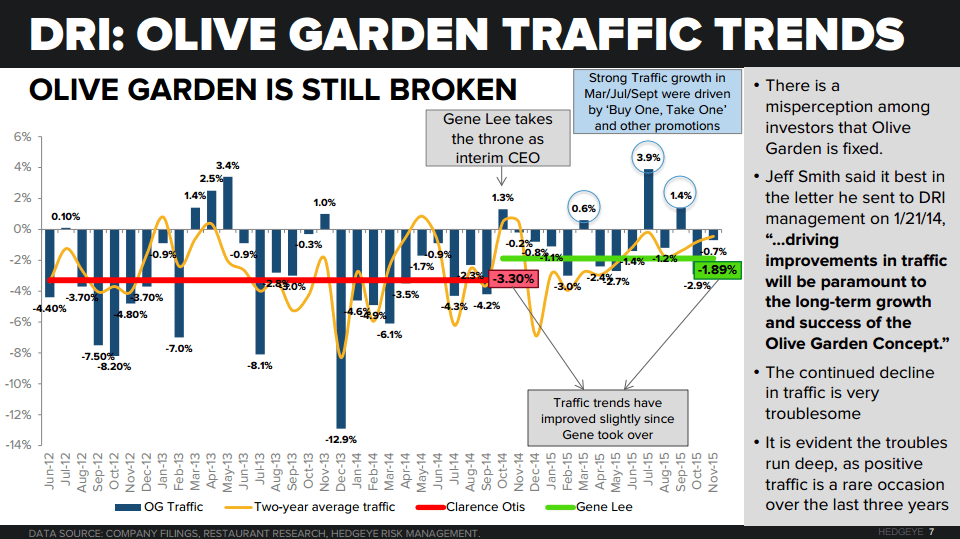

DRI

To view our analyst's original report on Darden Restaurants click here.

In a recent HedgeyeTV video update, Restaurants analyst Howard Penney visually contextualized the issues facing Darden Restaurants (DRI) and its chain Olive Garden. As you can see in the graphic below, Olive Garden's problems run deep as evident in its slowing traffic. That's not good considering Olive Garden makes up 56% of DRI sales.