There’s a lot happening this morning in the markets, but what interests us is what’s NOT happening. Specifically, we’re witnessing (often without seeing) the change in RH’s promotional cadence play out.

The company noted with its 2/24 preannouncement that it would be moving away from promotions towards a membership model – which we think will be formally rolled out within two weeks. But what happened just prior to the 2/24 announcement was the elimination of any and all promotional emails.

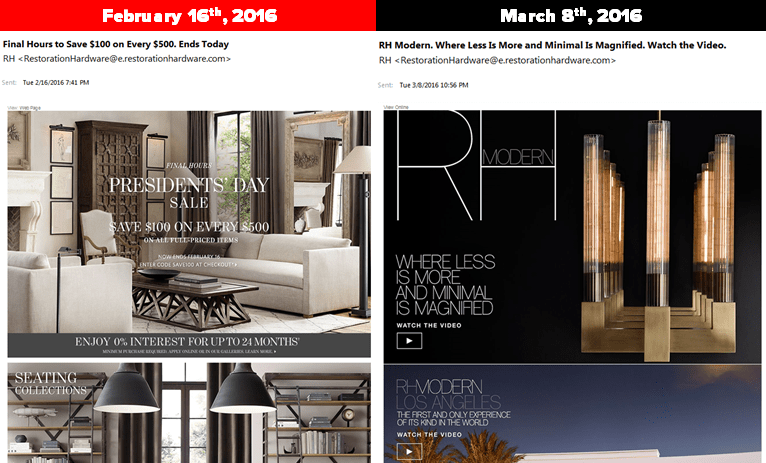

In fact, the last one was sent out on 2/16, and was arguably just as ‘Brand Destructive’ as the ones that came before it. In 3-years covering RH (the RH as it exists today) we’ve grown used to investors routinely talk about the latest promotional email from the company, and question why they exist for a brand that is supposedly so much higher-end. Those emails were sent not only every day, but multiple times each day to tens of millions of consumers – most of whom will likely never spend a dime at RH.

Three things have changed, however.

1) The first is size. Having an aggressive strategy where you need to blanket new consumers with spam on a) new products, and b) old products that need to be sold – might be appropriate when a company is maybe $500mm in sales (as RH once was). But it’s certainly not appropriate for a company that is $2bn in revenue looking to double in size through a higher end consumer base.

2) The second thing that changed is that selling online in this space stopped being as big of a competitive advantage about two years ago – at least how we look at it. Think about it…even Pier 1 went from 4% of sales online to about 20% in that time. Even aside from Home Furnishings competitors, most consumers’ in-boxes are absolutely riddled with product and promotional emails from every retailer/site they had the misfortune of registering with online…as well as the obscure retailers who paid-up for those (and your) email. The punchline is that the average consumer received about 10 emails per day three years ago from companies marketing products and services, but they receive 30 today.

3) Mobile has become a deterrent. About 90% of marketers now say that email is their primary channel for ‘lead generation’. But five years ago, mobile accounted for only 8% of marketing email opens. Today that number is 55%. Think about it…there’s a better than 50% chance that you’re reading this on a mobile device. I may be typing this on a mac with a 30” monitor, but it almost certainly looks less appealing when being consumed. Furniture takes this a step further. Why do you think that RH started presenting its quarterly earnings in a video format? Because it is an extremely visual part of retail, and they can appropriately show the vision on a big screen. That might look good on a large desktop or a smart TV. But it looks ‘above average’ on a regular laptop, and downright horrible on a 4” mobile device.

The punchline is that RH is changing the way it markets its product not just because business is weak and it had a problem delivering on Modern. But because it’s what the company needs to do in order to double the size of the company. The m.o. of the past economic cycle will certainly not take it through the next one. In fairness, RH was ready to roll this new strategy out roughly 18 months ago, but our sense is that it had such great momentum that it did not want to risk disrupting. Now, the time is right. It might be painful. In fact, it will almost certainly be painful. But do you think that just maybe a $38 stock and 25% downward earnings revision already knows this?

We can’t stand the uncertainty around another gap downwardward if numbers come down again with the guide later this month. But we maintain that our recession-case EPS estimate is $2.50, which we think puts the stock near $30. On the upside, we definitely, positively, absolutely think $10 in earnings is in play. Pick any multiple you want – the stock is many times where it is today.