Will the ECB issue “simulative” policy at its next meeting Thursday, March 10th? Our opinion is a resounding YES! Skip further down the page for our 7 supporting pieces of evidence.

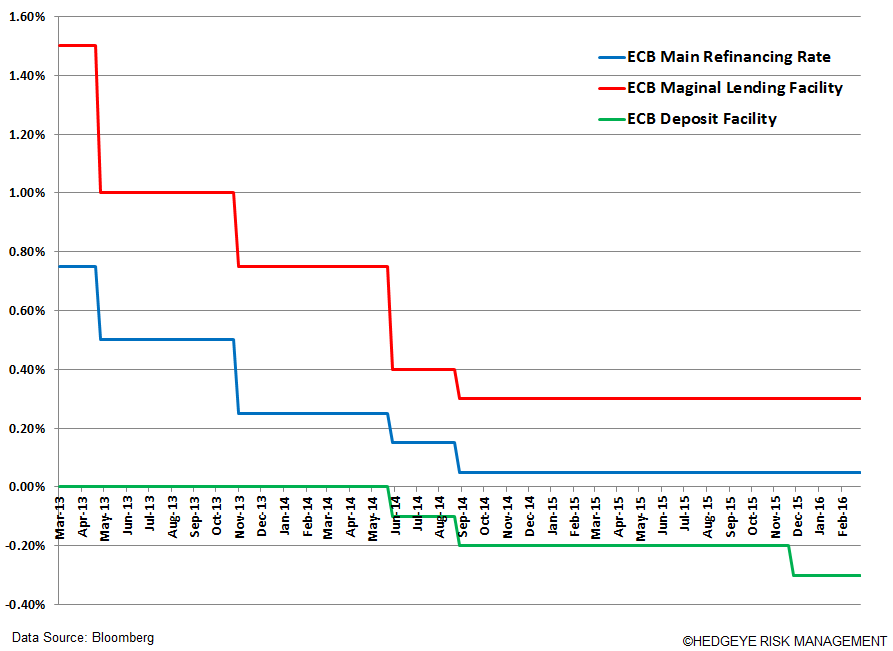

What’s in the cards? It’s anyone’s guess but we see a strong probability that the ECB’s QE program is increased (up from monthly allotments of €60 Billion) and we could see further points shaved off the Deposit Rate (currently at -0.30%).

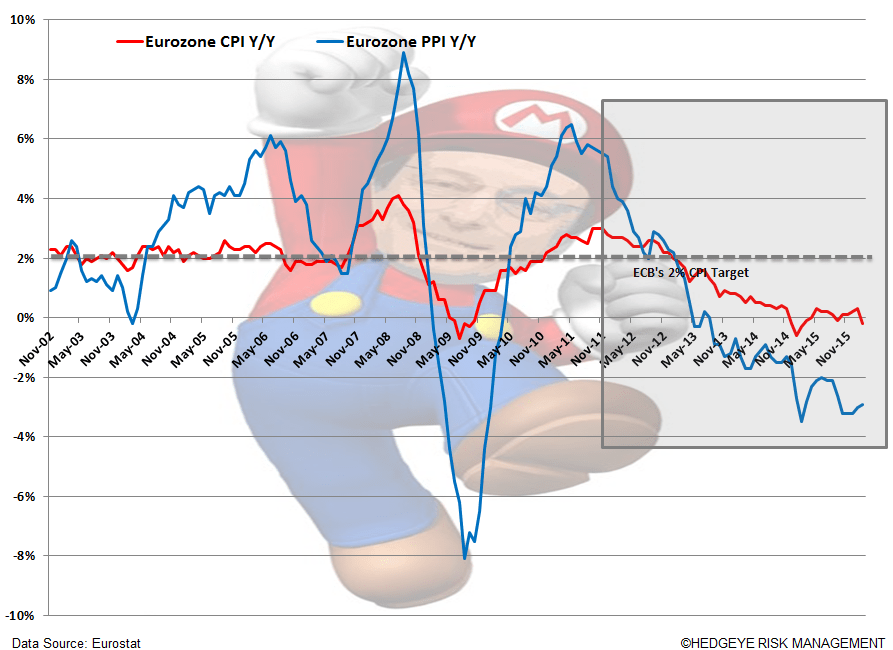

Will it move the economic needle? No! As we’ve called for time and time again, we do not see Draghi (nor other global central bankers) arresting Economic Gravity. For example, Eurozone CPI has held below +0.5% for the last 20 months (and is currently negative at -0.2%), this all in a period in which Draghi’s has purchased €780 billion in sovereign paper as a “simulative” and “inflationary” policy. How about that 2.0% inflation target? A pipe dream!

EUR/USD. What is different this time around is our call that the ECB’s Extend & Pretend “simulative measures” will strengthen the EUR/USD rather than weaken the common currency. Specifically, we expect the EUR/USD to bounce on March 10th if more QE is announced.

How’s that? As Keith explains in his Big Bang Theory, after 600 rate cuts globally, there’s a new regime of investors that has given up on the belief that central bankers can artificially produce stimulus and weaken their currency for economic benefit. This policy hasn’t worked in Japan, and it isn’t going to work in the Eurozone.

In the chart directly below we outline that our Big Bang Theory could get the EUR/USD up to our TREND ($1.12) and TAIL ($1.13) resistance levels, or a monster gain of 1% to 2.7% from current levels. We'd also expect associated selling of European equities.

Our Top 7: The Forces Starring Draghi Straight in the Face… and Suggesting Policy “Action”:

- It’s All About Inflation! Or lack thereof… Not only is the ECB nowhere near its 2.0% inflation target, CPI is negative! In the initial February reading, Eurozone CPI fell to -0.20% Y/Y vs Expectations for 0.00% and Prior +0.30%. This is the first time inflation went into negative territory since September 2015. #GravityHurts

- Producer Price Index, like CPI, mirrors the deflationary forces, most currently at -2.9% JAN Y/Y, and has been in negative territory since July 2013! (see Super Mario chart below)

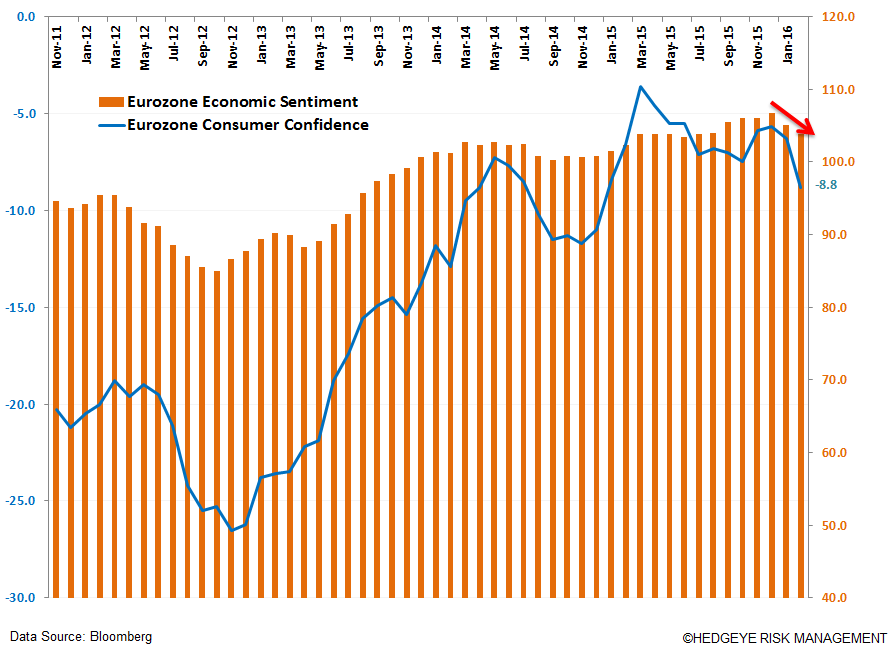

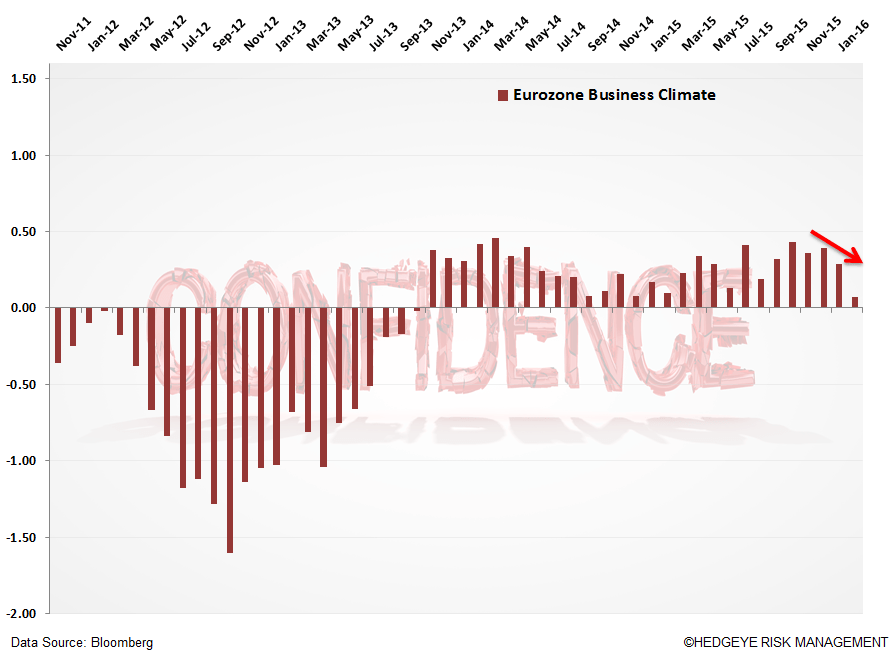

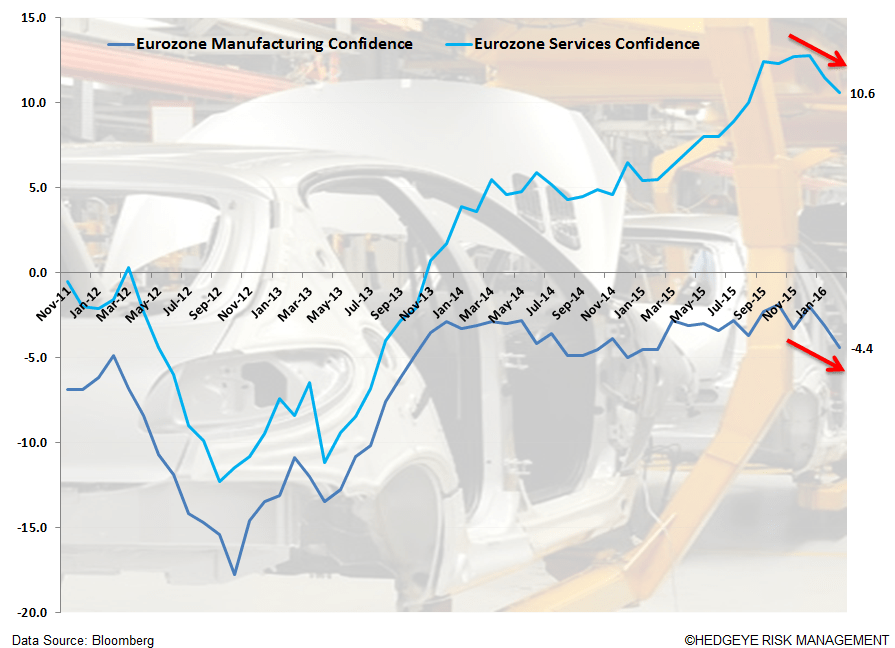

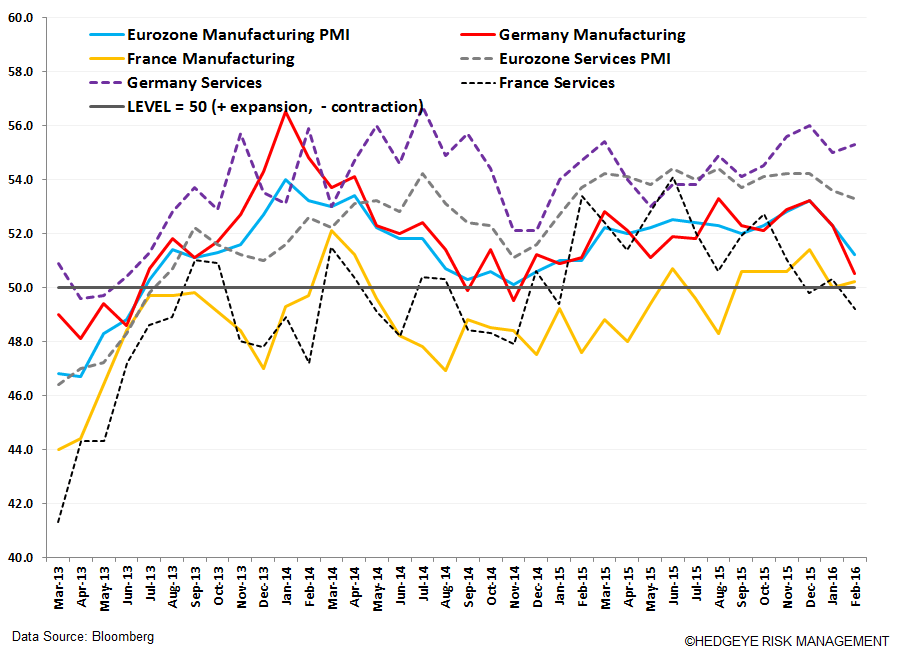

- Growth is Anemic. See our proprietary Eurozone GIP (growth, inflation, policy) for the coming quarters (ugly Quad 4 = growth slowing as inflation decelerates); declining Eurozone Confidence figures; and recent trends in PMIs = down! (See charts below)

- The ECB Council is overwhelmed with Doves (see Bloomberg Industries chart below) and has telegraphed policy Action!

- In a letter to a European MEP, ECB President Draghi reiterated that the policy review in March should be seen against a background of increased downside risks to the earlier outlook. The letter confirms that the technical preparations are being made in order to ensure that the full range of policy options are available.

- ECB’s VP Constancio recently said that while no decisions have been made, a lack of confidence in getting inflationary pressures higher could cause his central bank to deliver more stimulous next month.

- ECB’s Liikanen said the central bank is ready to use additional monetary policy measures, if needed, to reach its targets.

5. A Year Later… Draghi last cut the Deposit Rate in December 2015 (by 10bps to -0.30%) and issued the QE “Drugs” (monthly asset purchases set at €60 Billion/month) in January 2015. With investors wanting results yesterday, one year into this program is a long time. Delivering more “non-conventional” policy “sauce” is a great way to CYA after a year in which Draghi failed to arrest declines in growth and inflation.

6. ECB Minutes called for downward pressure on inflation outlook from the decline in oil prices and oil futures curve.

7. ECB External Projections Down. In January, the ECB published its updated economic projections by external analysts (not the ECB staff who announces updates at the March meeting) and the forecast for inflation expectations were lowered.

- Professional forecasters cut inflation forecast to 0.7% in 2016 vs prior 1%, 2017 at 1.4% vs 1.5% and 2018 at 1.6%.

Mr Draghi, we'll be tuned in this coming Thursday!