Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

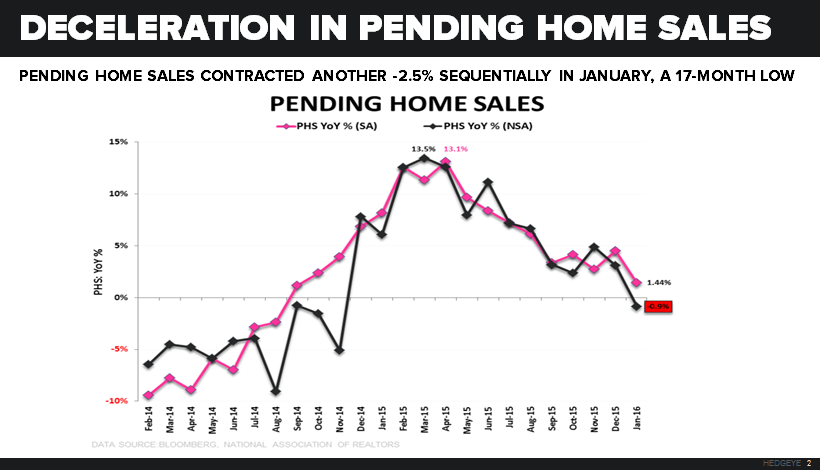

"... For #behavioral evidence of that reality, look no further than one of our better new short selling ideas – US Housing (ITB). Signed contract activity for “Pending Home Sales” contracted another -2.5% sequentially in January. That’s a 17 month low in rate of change terms…"