VFC is near the top of the list of names we really want to own. The portfolio (even though we don’t like portfolios of brands) has gotten so good over time, it diversified geographic exposure more than most people think with ~30% of sales coming from outside the US, and its channel distribution is just about as good as a wholesale portfolio can expect – and it is now by a factor of 3 it’s own largest customer. These factors add up to a degree of earnings defendability that you don’t find too often in retail. And of course, check out the 20-year chart. Some management teams are worth betting against – this one certainly is not.

With all that said, we saw an extremely sharp deceleration in organic growth – from 7.4% to 2.6%, at the same time Gross margins rolled 70bps vs last year and EBIT margins similarly turned down. Management came across as ‘beyond-beared-up’ on the global demand equation throughout the remainder of this winter season and at least for the next 6 months. Yes, weather played a part in the miss – we all know this part of the story without having to go through puffy coat inventory issues. But let’s be crystal clear, there was more than weather at play here. In fact, Janet Yellen likely had a bigger impact than mother nature.

Given VF's product diversity mass market/athletic and global reach, this company should be putting up more consistent and predictable earnings than just about anybody, anywhere. And yet, it didn’t, which might end up being one of the more negative data points we've seen through retail earnings season.

Yes, the stock is starting to look ‘cheap’ (whatever that means). But when a management team as good as this loses control over its business so quickly and to such a great extent, we absolutely positively cannot say that this guide down will be the last. If you have to maintain certain exposure to retail, then yes, it might be worth picking away at VFC on red – but only because everything else is likely to go down more.

Other Thoughts --

Macro Outlook - VFC sounded particularly bearish on the current Macro environment. Characterizing the Macro environment as 'worse than anyone expected'. Supporting that with numbers, this was the first time VFC reported negative revenue growth since 2009. But, unlike many street models would lead one to believe, it's not letting up now that we've entered 1H16.

Inventory - Inventory was up 9% and the sales/inventory spread weakened to -13% from -9% last Q. Despite management spin, the fact is that inventory is way too high at VFC and likely around the industry (DKS, TGT, WMT, etc.). Even if we were to adjust for the cold weather hit, we are still looking at a sales to inventory spread of -9%.

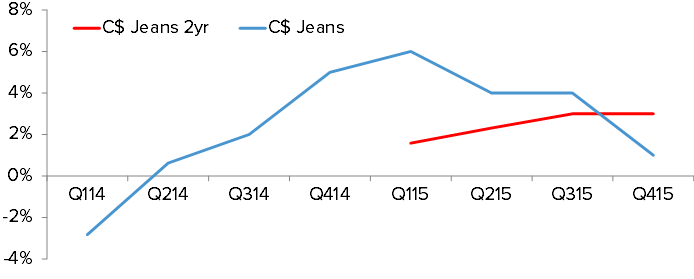

Outdoor Weak, Jeanswear Strength - If there was one positive in this print for VFC and its US wholesale partners it’s the jeanswear segment. Contrary to what we heard from HBI on the basics category at WMT and TGT, the jeanswear segment actually accelerated in 4Q. Not that the wholesalers can hang their hats on that one. Outdoor was the laggard at 1% C$ revenue growth, especially when considering the way it has carried the topline. But, North Face as a brand is anything but broken.