KEY POINTS

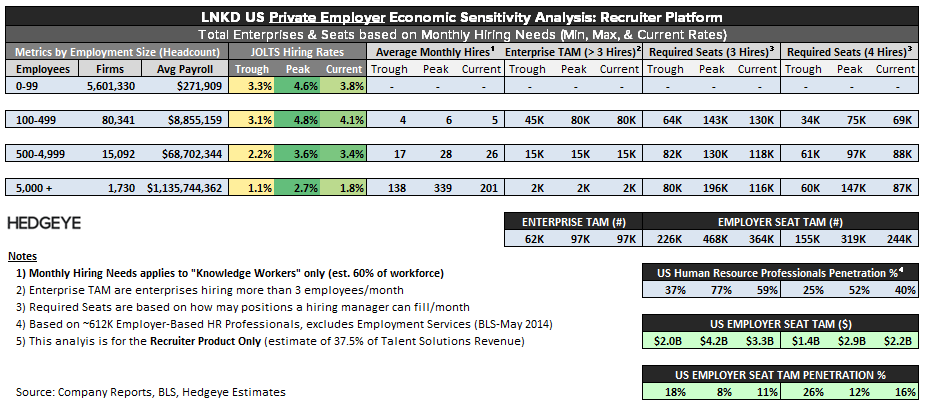

- CLOSED LONG, MULLING SHORT: Our Talent Solution TAM analysis suggests that the majority of LNKD’s opportunity is in the up-sell opportunity (vs. account volume). We believe that opportunity is largely driven by the selling environment, which is largely driven by macro; specifically where we are in the employment cycle. Our Macro team has been flagging that we are late cycle, and recently suggested that we may be heading into a recession as early as 2Q16. With that backdrop, we closed the long once we saw our tracker deteriorate more than seasonality alone would have suggested. Now, the question is whether that deceleration is a blip, or the beginning of a bigger trend. If the latter, our TS Economic Sensitivity analysis suggests the up-sell will get much tougher from here (see first table and note below for detail).

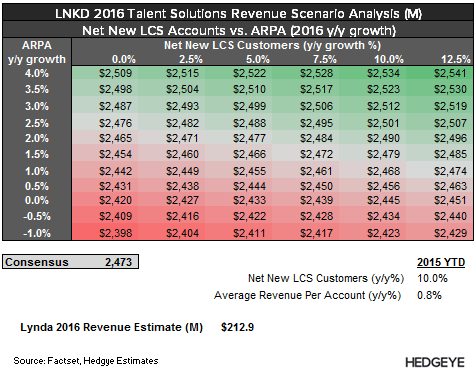

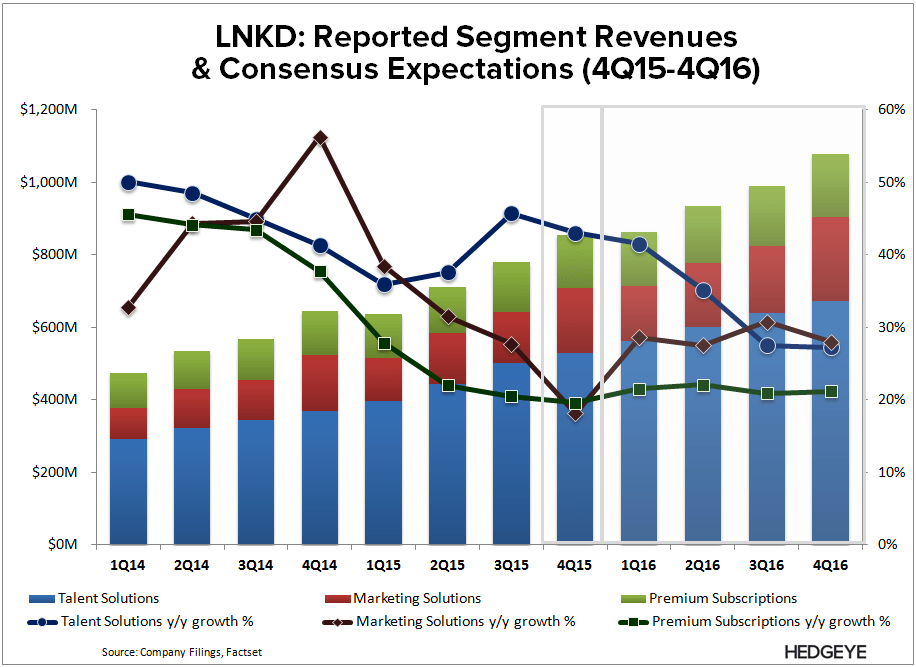

- EXPECT LIGHT 2016 GUIDANCE: We suspect it's even less likely now that mgmt guides to street expectations if our tracker is correctly flagging a deteriorating selling environment. Consensus may have been asking for too much to begin with. The implicit assumption in consensus Talent Solution revenues estimates is calling for an acceleration in ARPA, which would be a challenge even if the selling environment wasn’t deteriorating as our tracker suggests. Futher, consensus is assuming accelerating growth in LNKD's other two segments, meaning any upside from both Sales Navigator and the dissipating Display headwind appear to be captured in estimates. Further, Fx remains a headwind YTD, which we expect to be top of mind for this mgmt team since FX was the largest source of its guidance cut last year.

- BUT CAN’T QUITE GAUGE REACTION: We doubt we’re alone in our expectation for soft guidance since LNKD’s mgmt team is notoriously conservative with its guidance to begin with. The setup right now isn’t all that dissimilar to the 2015 guidance release, which was inline with consensus revenue and slightly lower on EBITDA, with 1Q15 missing across the board. However, LNKD crushed 4Q14 estimates, and the stock ripped. We believe mgmt gave itself enough breathing room on the 4Q15 guide, so it’s possible that the stock could pop on this print as well. Then again this isn't 2015, and LNKD’s recent outperformance suggests expectations are rising into the print. We're debating whether to pull the trigger on the short before LNKD reports on Thursday.

![]()

LNKD: New Best Idea (Long)

07/14/15 08:00 AM EDT

[click here]

As a reminder, we will be hosting our quarterly Internet Best Ideas call this Thursday at 1pm EST. In the interim, let us know if you have any questions, or would like to discuss further.