Key Takeaway:

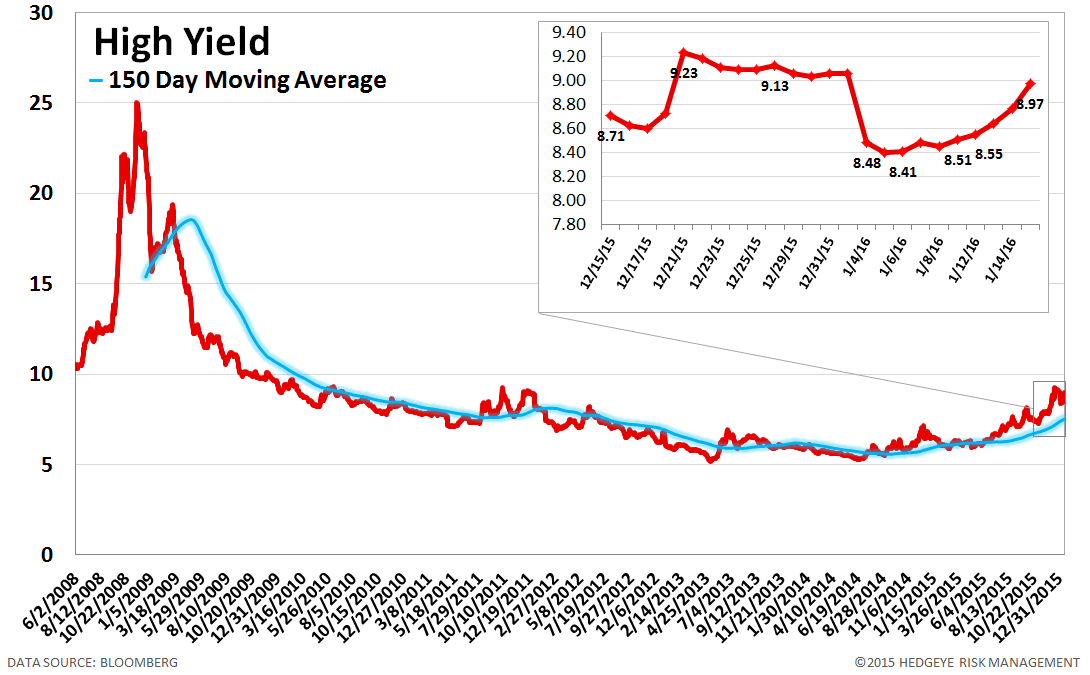

Slowing growth, both domestically and in China, cascading oil prices and rising concerns over default in the energy arena continue to sound the alarm for investors. Default swaps widened globally last week, especially in emerging markets and most notably in Russia where Sberbank swaps widened by +50 bps to 413 bps and Russian sovereign CDS widened by +50 bps to 385 bps as oil prices continued their slump. Additionally, the high yield YTM blew out by +53 bps last week to 8.97%.

Our heatmap below is more negative than positive across all durations.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 2 of 12 improved / 6 out of 12 worsened / 4 of 12 unchanged

• Intermediate-term(WoW): Negative / 3 of 12 improved / 7 out of 12 worsened / 2 of 12 unchanged

• Long-term(WoW): Negative / 1 of 12 improved / 4 out of 12 worsened / 7 of 12 unchanged

1. U.S. Financial CDS – Swaps widened for 12 out of 27 domestic financial institutions with the median spread expanding by another 6 bps week over week. At the bottom of our U.S. CDS table below, we have added indices on investment grade and high yield CDS, which widened last week by 11 bps to 110 and by 33 bps to 555, respectively.

Tightened the most WoW: CB, ACE, MMC

Widened the most WoW: AIG, AXP, MET

Widened the least/ tightened the most WoW: CB, MMC, ACE

Widened the most MoM: AXP, ALL, MET

2. European Financial CDS – Swaps mostly widened among European banks last week. CDS on Portugal's Banco Espirito Santo were an exception, tightening by -490 bps to 1,229 on deliberations at ISDA'S Credit Determinations Committee. Last week, the committee failed to reach a super-majority decision on whether the transfer of Novo Banco senior bonds into Banco Espirito Santo constituted a governmental intervention. Additionally, it has set January 22 as its decision deadline on whether a portion of Novo Banco CDS would be transferred to Banco Espirito Santo.

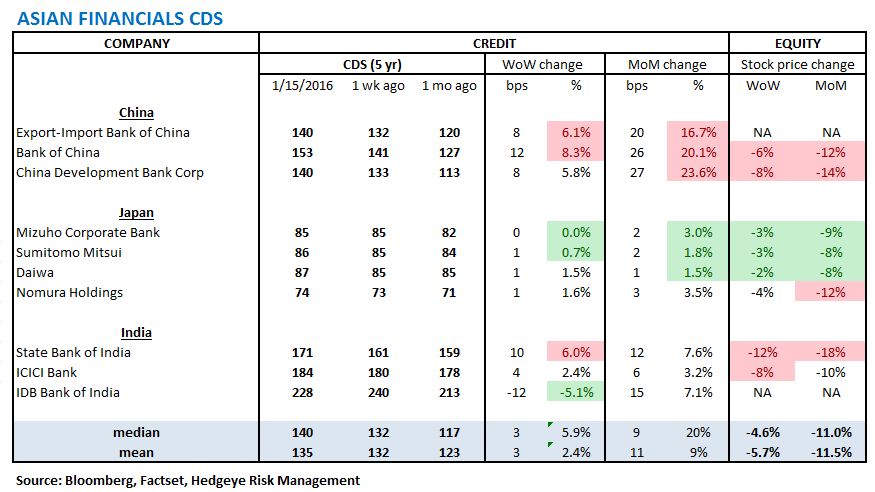

3. Asian Financial CDS – Swaps among Asian financials mostly widened last week. Chinese bank CDS widened between +8 and +12 bps as investors continued to worry about the country's decelerating economy. In India, although IDB Bank of India CDS tightened by -12 bps to 228, ICICI Bank and State Bank of India widened by 4 bps to 184 and by 10 bps to 171, respectively.

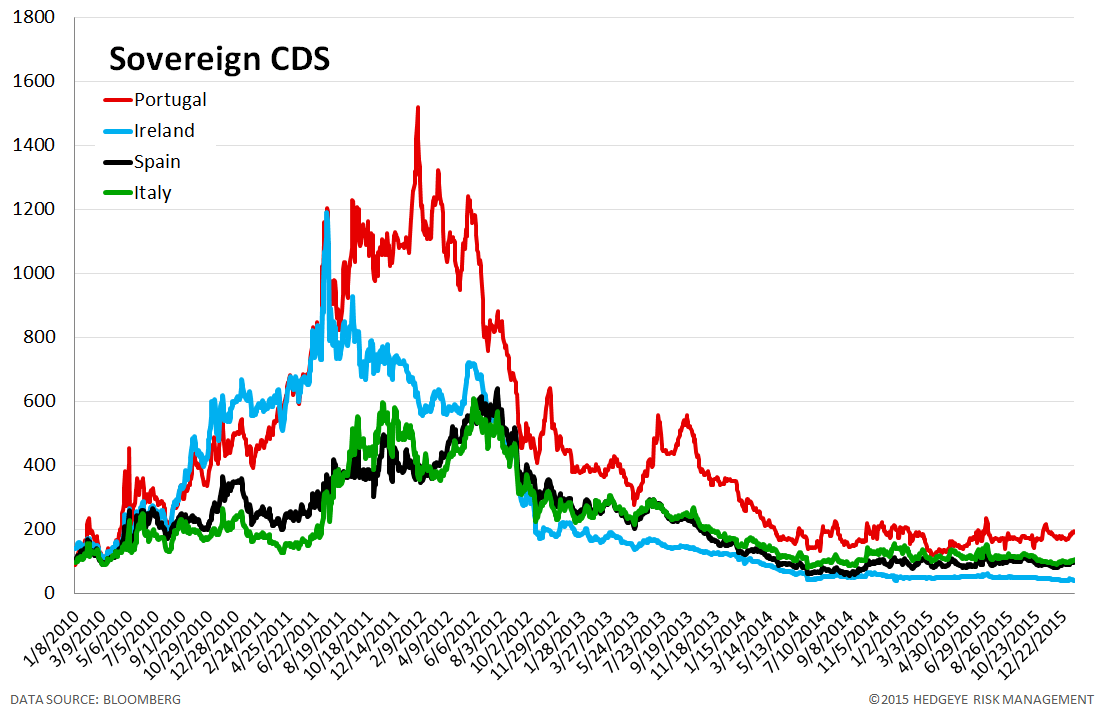

4. Sovereign CDS – Sovereign swaps mostly widened over last week as growth concerns mounted. Portuguese sovereign swaps widened the most, rising by +12 bps to 194.

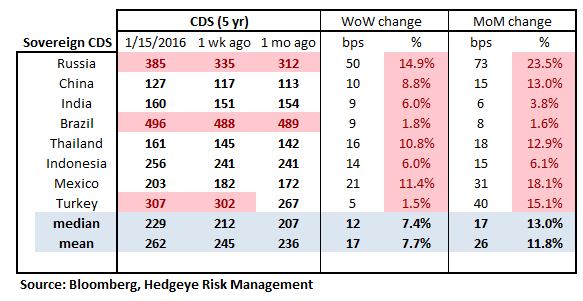

5. Emerging Market Sovereign CDS – Emerging market swaps were hit especially hard by concerns over slowing growth in China and low oil prices. Russian sovereign swaps widened by +50 bps to 385 bps. Meanwhile, Brazilian sovereign CDS are once again knocking on the door of 500 (496 bps), +9 bps on the week.

6. High Yield (YTM) Monitor – High Yield rates rose 53 bps last week, ending the week at 8.97% versus 8.45% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index fell 6.0 points last week, ending at 1802.

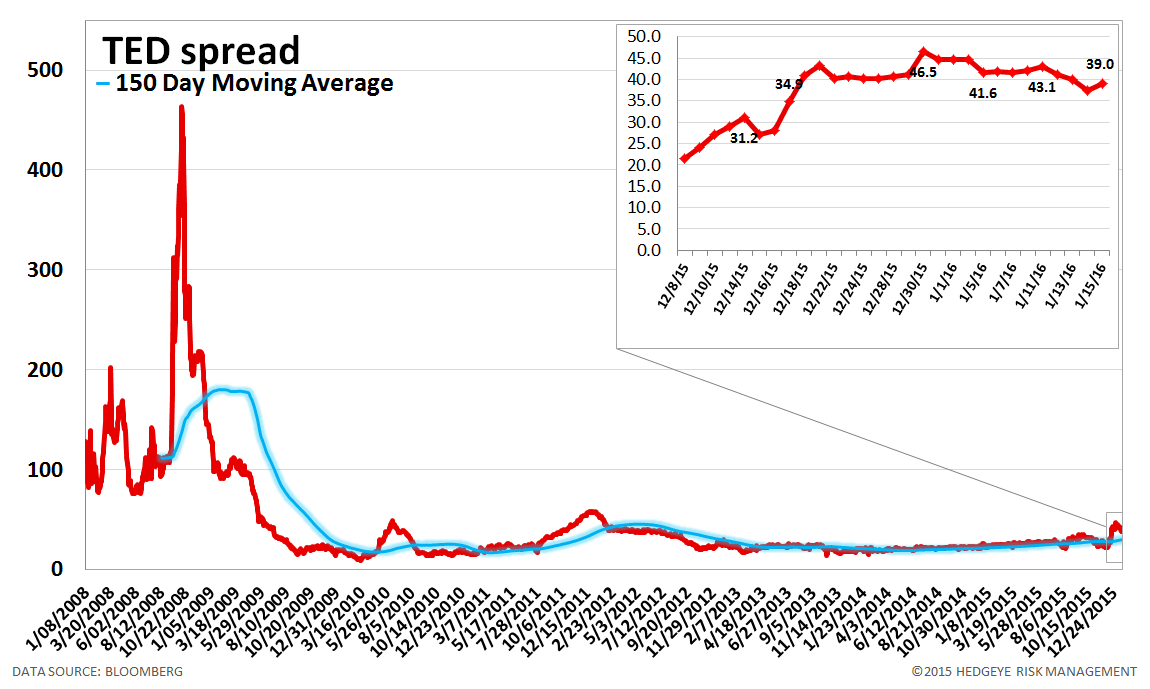

8. TED Spread Monitor – The TED spread fell 3 basis points last week, ending the week at 39 bps this week versus last week’s print of 42 bps.

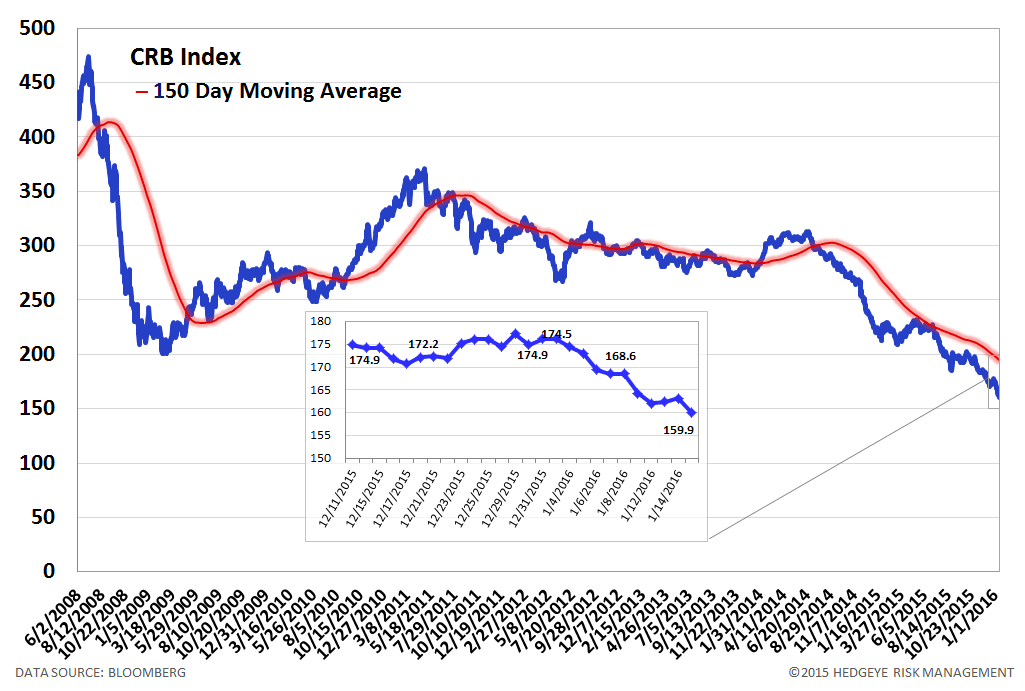

9. CRB Commodity Price Index – The CRB index fell -5.6%, ending the week at 160 versus 169 the prior week. As compared with the prior month, commodity prices have decreased -7.1%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 12 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index was unchanged, ending the week at 1.96%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China fell 1.6% last week, or 33 yuan/ton, to 2009 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

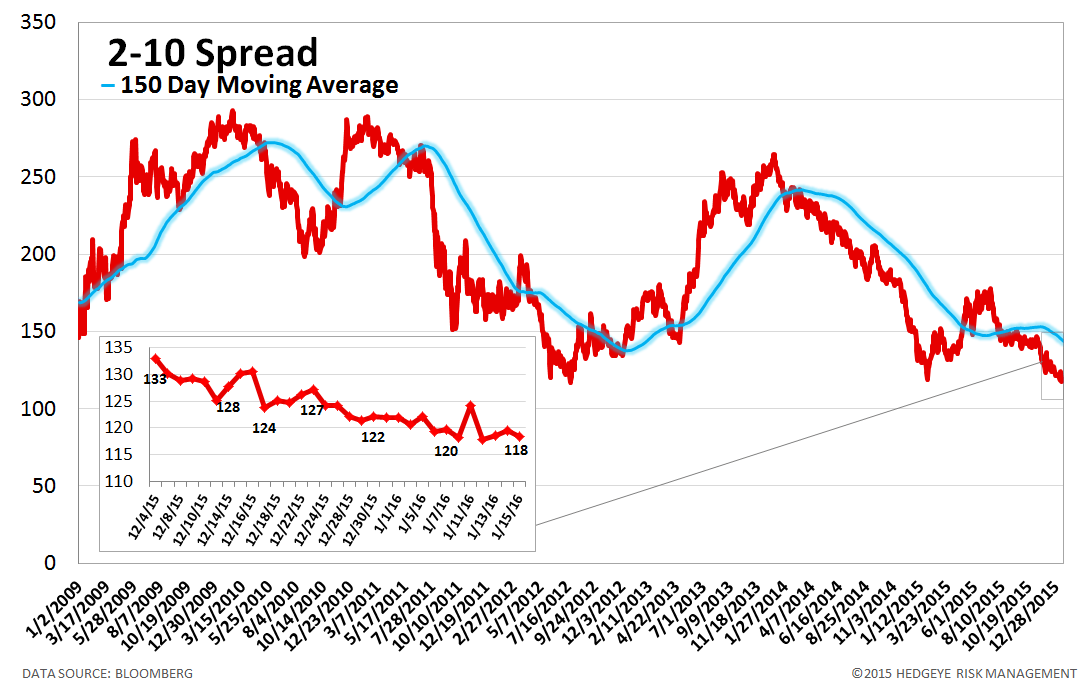

13. 2-10 Spread – Last week the 2-10 spread was unchanged at 118 bps. We track the 2-10 spread as an indicator of bank margin pressure.

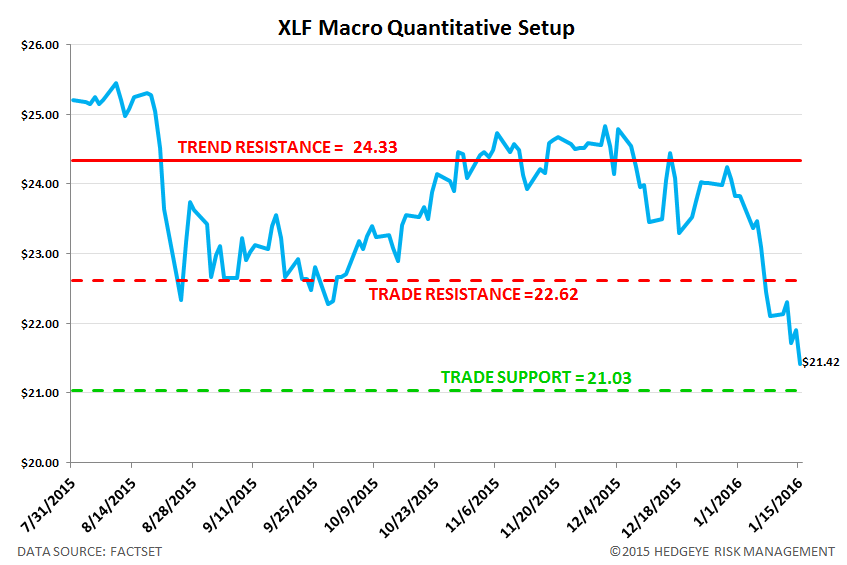

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 5.6% upside to TRADE resistance and 1.8% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT