More than any other company/issue we've had questions on since 2016 kicked into high gear, RH takes the cake – and more specifically, its near-term earnings trajectory. We’d peg it at roughly a dozen queries in just two days, which is very big for us. We’re not surprised, and we agree 100% with the impetus for the concern. We believe fully in the long-term call, and believe now as much as ever that there’s $11 in earnings power, and that people will actually start to believe it within a year. But the cold hard fact remains that the tactical game changed in December due to promotional activity, perceived economic sensitivity, and timing issues around concept and new store launches.

We can talk all day about the 2-3 year economics of new categories ramping up sales into bigger stores at lower rents. But the fact is that if RH misses revenue and/or earnings in either of the upcoming two quarters, $11/ps in future earnings won’t mean squat, and this multiple will deflate faster than a game ball in Foxboro (sorry Patriots fans).

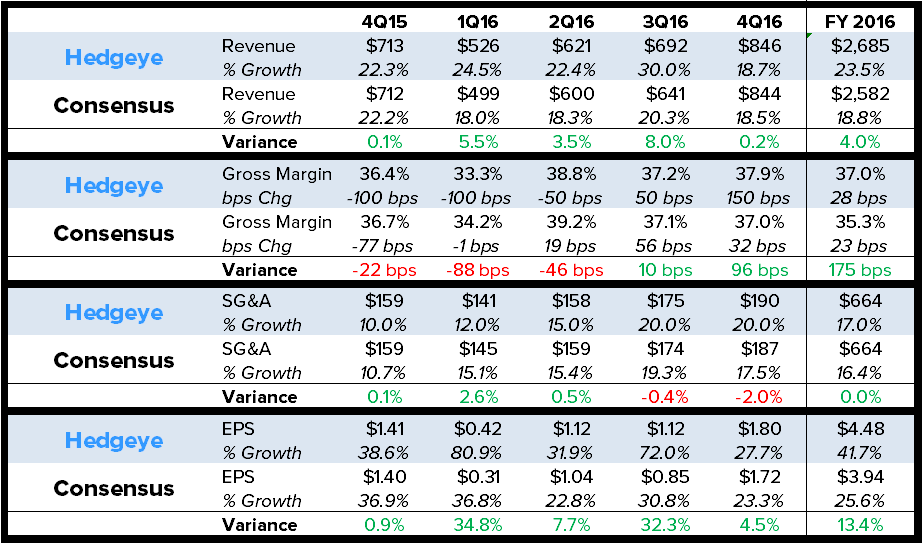

As such, in the tables and charts below, we compare where we shake out in each of the next four quarters versus consensus, with particular focus on Sales, Gross Margins, SG&A, and EPS in 1H16. The punchline is that we’re ahead of the Street every quarter on EPS, and are coming in at $4.48 for the year vs the Street at $3.94. The good news is that this is almost entirely top line driven throughout the year, with SG&A leverage to go with it. The downside is that we’re more conservative in both 1Q and 2Q than the Street on Gross Margin. When all is said and done, however, we think that a better comp and higher EPS will trump lower GM, given that weakness in the latter is so well telegraphed.

[As a point of reference, we’re going to vet every single part of the RH Bear Case across durations in a Black Book to be released on January 25th (1pm EST presentation). We won’t necessarily disprove all of it, but we will fully analyze it. Stay tuned for details.]

EXHIBIT 1: Hedgeye P&L Variance vs Consensus

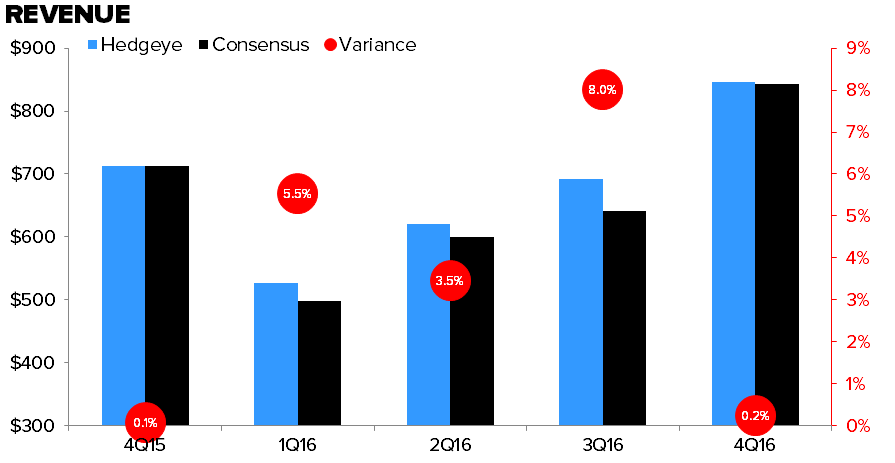

EXHIBIT 2: RH Revenue, Hedgeye vs Consensus

4Q15: To get to the streets #’s for 4Q (mid-point of guidance) need to assume a big ramp in the 2yr trend from 16% to 23%. That reacceleration = $79mm in sales. If we attribute all of that to Modern/Teen we have to make modest assumption that M/Teen books run a productivity rate of just 45% of Spring mailings. That would be what we’d consider an obscenely low performance. Plus RH guided down margins appropriately to win market share. It appears to be working. Top line should not be an issue.

1Q16: Modern/Teen not a 1-quarter event – this builds sequentially. Look at big Source Book revamp in 2Q/3Q14 for proof. Plus, vendor network is the M/T revenue bottleneck, not consumer demand. That’s not a bad position to be in.

2Q16: Continued benefit from Modern & Teen, plus newest design galleries (Chicago, Denver, Tampa, Austin + LA Modern) will have more material impact to topline. Increased marketing spend in the form of source book pages.

EXHIBIT 3: RH EBIT Margins, Hedgeye vs Consensus

4Q15: Promotional environment pressure takes margins down in 4Q. Guide for -100bps on GM likely overshot to the downside. SG&A leverage from Source Book savings and scale in the model.

1Q16: Assume that promotional pressure persists, coupled with DC occupancy deleverage, and higher shipping cost – offset by one more quarter of SG&A leverage as Source Books savings amortized over 12 month window. Strong top line flows through.

2Q16: Promotional pressure eases, product flow normalizes and retail occupancy starts to kick in. Take spending up on marketing to drive top line.

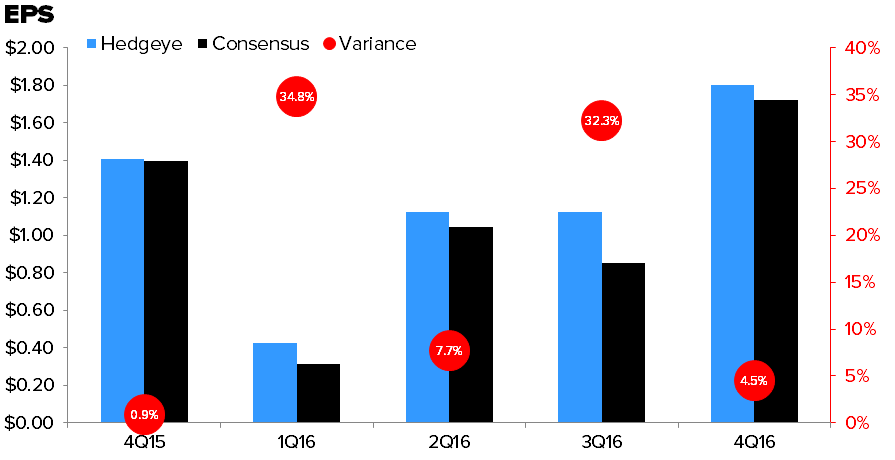

EXHIBIT 4: RH EPS, Hedgeye vs Consensus

4Q15: Expectations in check for 4th quarter, and RH has to deliver. Sales expectations assume a big acceleration, but product pipe, new galleries, and market share efforts will drive 35% earnings growth even with GM pressure.

1Q16: Street underestimating how long tail is on Modern/Teen product. RH will push envelope to take market share. Enough SG&A levers left to offset any GM pressure.

2Q16: New galleries + Modern/Teen + increased marketing dollars = strong top line. Modest EBIT margin leverage. Street too low by $0.10.

EXHIBIT 5: RH Peak, Mid, Trough Valuation and Sentiment Summary

Any way you cut it, RH is sitting near a trough valuation on all metrics, and within 200bps of peak short interest (currently 29%). In fairness, RH has trading history for only half of the current economic cycle – but for the stock to be anything other than egregiously cheap at $78, we need to be more wrong on the fundamentals than we’ve been on any name in a very long time.