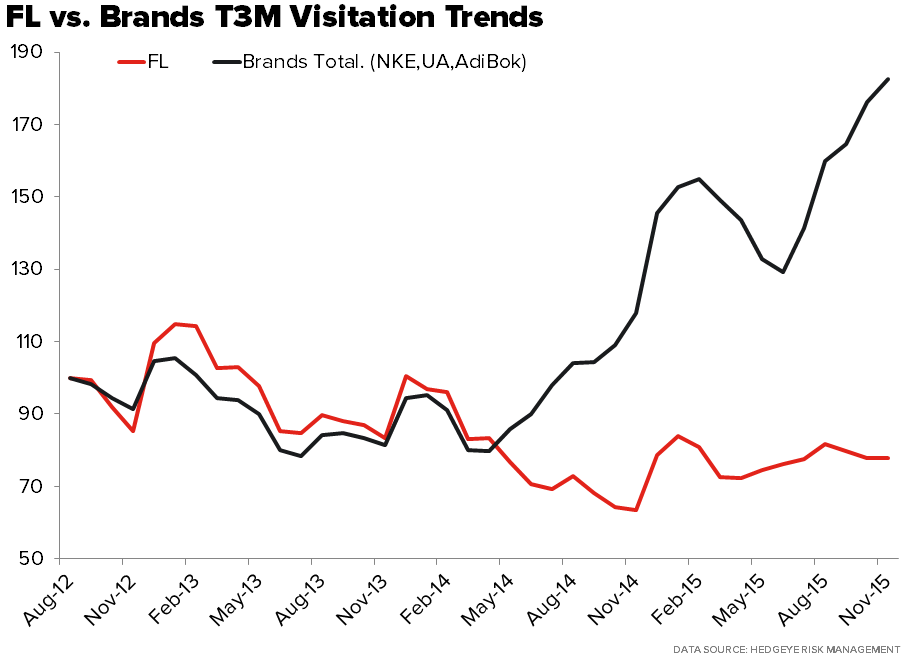

FL | THIS IS BAD

Takeaway: e-commerce trends appear to be bifurcating further between Nike and FL as we head into year-end. FL remains Best Idea Short.

For the full note see link: CLICK HERE

Free Shipping Friday -- Seriously... ANOTHER Themed Shopping Day?

Today is Free Shipping Friday. For starters, did anyone know that this day even existed? It sounds more like an Instagram hash tag than a shopping promotion, but it’s simply another invented day along with the usual suspects (Black Friday, Cyber Monday, Small Business Saturday, Green Monday) intended to create a little extra buzz as we approach the end of the Holiday shopping season. In fairness, the retailers need everything they can get. But on the flip side, if everybody is doing it, is it really a competitive advantage for anyone?

The day not only offers free shipping, but guaranteed delivery by Christmas eve. Of over 1064 participating merchants, one notable missing name from the list is KSS, which on its own lowered its free shipping threshold from $75 to $50 a few weeks back and introduced a whole host of Door Buster sales that will hit this Saturday.

One day of free shipping isn't damning for margins by any means, but we think it’s indicative of the inevitable reality that US Retail is moving to 100% free shipping, 100% of the time.

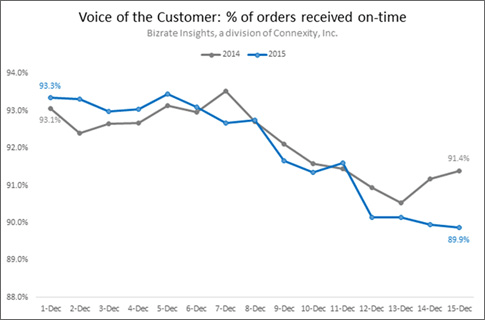

It will be interesting to see how the carriers handle the capacity. We've seen the reports noting the higher volume, and the spread in on-time order rates has widened by 2 points vs. last year (see exhibit 2 below). With all the promises being made on delivery time, we could see a lot of disappointed parents on Christmas Day.

TGT, WMT, AAPL - TGT mobile wallet in the works...great

http://uk.reuters.com/article/uk-target-mobile-payment-idUKKBN0U11U720151218

We don't understand the need for retailers to launch their own mobile payment systems -- aren't credit cards enough? As if the companies need to assume the liability, why not let Apple, Google, and Samsung duke it out. On Target specifically, who in their right mind would give the company that type of access to credit card information after its system and security failures led to one of the biggest data breaches in retail history?

BBY - Best Buy hopes faster free shipping will rein in holiday procrastinators

AMZN - Amazon leasing airplanes, tired of UPS and FedEx

The force is strong in retail thanks to Star Wars

Marketing campaign launch date challenged Cyber Monday in online sales

BABA - Bad BABA warned of selling counterfeit items by US

http://www.wsj.com/articles/u-s-warns-alibaba-again-about-selling-counterfeit-goods-1450406612

APP - Two Parties Aligned With Charney Said to Have Bids Out for American Apparel

AMZN - Study: Most holiday shoppers check out this retailer

"87% of respondents will comparison shop at Amazon.com before buying a gift….73% of respondents said they will buy from Amazon and 71% will spend more than a quarter of their holiday budgets on Amazon"

http://www.retailingtoday.com/article/study-most-holiday-shoppers-check-out-retailer