Conclusion: The call here is simple. It’s not easy, but it is simple. If you DON’T think we’re headed into a recession, or are not concerned about growth slowing incrementally from here…then you’re looking at a 20% FCF yield and 6% dividend yield as PIR recovers from a 3-year investment to build its online business from 1-20%. In a normal economy next year, this stock could be a 4-bagger. But if you’re in the other camp, then the equity value could go away entirely. That’d be a great buy for some financial buyer at just $200mm – but it wouldn’t help equity holders much. Since we put PIR on our Best Ideas List in mid-August, the margin recovery part of the story really has not changed, and valuation looks extremely attractive. Unfortunately the Bear case gained serious momentum – most notably with premium players like RH even calling out the promotional nature of the space (if it gets to RH’s level, you know its bad). We still think that the upside to a $20-something stock is there. But so is potential downside to zero. That’s a push from where we sit. A ‘push’ is not good enough for us to stand behind this one, as such it’s being relegated to our Idea Bench.

Our Best Bear Case:

Does Pier 1 Imports really need to exist? Seriously, if the chain went away entirely overnight, would the consumer really miss a beat? Probably not. They’d buy their rattan furniture and decorative nick-nacks at Target, Wayfair, or one of the other thousand places to buy cheap goods from China. The company seemingly has no real product strategy – at least that’s what someone listening to the call (like us) would surmise. All the company talks about is its tactical marketing plan needed to drive more people into the store. In this business, great product can get by with mediocre marketing, while mediocre product needs world class marketing. Also, the company talks about how [these volatile consumer shopping patterns are changing how we think about and plan our business.] Really? Couldn’t the company anticipate that traffic would be under pressure? It’s been written in the cosmos for the past three years at a minimum. We’d be a lot more comfortable with a clear vision as to how PIR can lead the consumer to create its own destiny as opposed to having to make tactical adjustments everytime Target or Wayfair burps in the wrong key. Comps were negative this quarter for the second time in five years, and we have yet to see any Gross Margin recovery from its e-commerce build-out initiatives over the past three years. SG&A (-9%) made the quarter, and while much of this is sustainable, the reality is that the company is reactionary in planning more TV advertising, which kind of shoots the SG&A leverage angle in the foot for 2017 (Jan). Ultimately, PIR is in a relatively good category in retail – one that does not have anywhere near the volatility as apparel. So will PIR be here in 5-years? Yes, it will. It’ll likely have 2/3 the number of stores it does today, but it will still probably be around. That, however, does not mean that the equity needs to be worth anything. With the stock approaching $5 and a market cap of $450mm, it’s entering no-man’s land. There’s not a very big pool of institutional investors out there who are going to step in and load up on a marginal quality, levered, home furnishings retailer, with a footprint that’s too large, a market cap that’s too small, when we’re at the tail end of an economic cycle. Sheer gravity could cut this stock in half again from here.

Our Best Bull Case

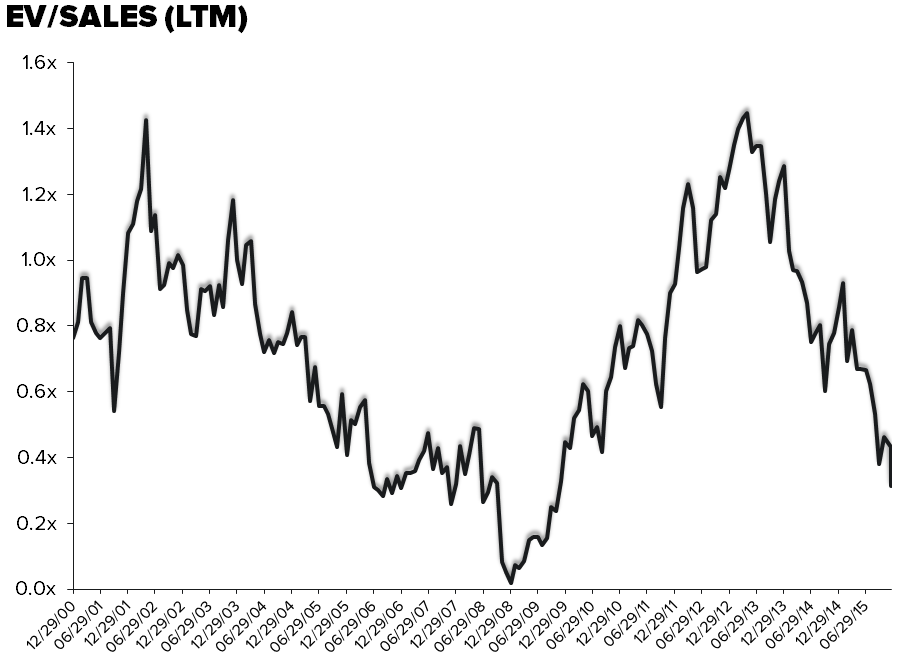

As noted when wearing the Bear hat, this is a relatively stable category, and PIR is an established brand that has relevance across a very wide age demographic. Brand weakness has not driven earnings down in recent years, it’s been investment in the infrastructure. By and large, PIR’s product has always been primed perfectly for on-line distribution. But as recently as three years ago, on-line as a percent of total was only 1%. Yes o-n-e percent. So the company invested to build its capability to make small shipments to many individual customers instead of only making large shipments to a much smaller number of stores. This investment cost PIR over 500bp in margin, and our math suggests that about 300bp is recoverable. About 20% of sales is on-line today. At the same time, the investment the company made in e-comm is clearly rolling over, with capex coming down 33% and SG&A off 9% in the quarter. The company’s commentary suggests a conservative guide for FY17, and even on a – flattish comp we’re still looking at $0.60 in earnings, and better yet, a $30mm sequential positive change in cash flow. If you look at valuation today, you’ve got 0.3x EV/Sales, which is about as low as it’s going to get unless you think the business is going away, which we don’t. Despite the volatility in the stock, on an annual basis revenue and EBITDA are fairly predictable. Yes, the company has around $200mm in debt ($150mm net) but we don’t have any maturities till 2021, when we’ll be in a completely different economic cycle. We think that PIR earns about $0.60 next year, or about $100mm in free cash flow – that’s less than 8x earnings, about a 20% FCF yield and a 6% dividend yield.

Details on the quarter...

Top Line

PIR put up only its 2nd negative comp number since 2Q10 (Aug ’09). That’s an impressive string for a company who sells marginal home goods, but is further evidence of the fragmentation in the market place. The question we have to ask ourselves now with a -2% to -4% comp on the horizon in 4Q and ‘conservative’ topline planning in FY17 is, has something fundamentally changed in the industry that makes a name like PIR a secular loser? Essentially the Wayfair question. When we look at the numbers – PIR is operating in a $175bn category, with $27bn of that done online. PIR now competes in the online arena, it didn’t 3 years ago, and has just over 1% of the total market share. The largest player in the space, Ashely Home Furnishing has ~2.5% share of the market. In that type of competitive environment we don’t think that there is a net loser and a net winner. PIR has inflicted a lot of wounds to itself over the past 18 months, but we don’t think that the competitive environment is so vastly different that it can’t produce the 2% top line growth it needs for this model to work.

Gross Margin

Merch margins were down another 380bps in the quarter with supply chain inefficiencies accounting for 200bps of the decline and the balance attributed to an increase in promotional activity. For the year, merch margin guidance stands at 55% down from the 58%-58.2% guide giving on the 4Q15 conference call. Supply chain inefficiencies have continued to dilute the gross margin line and will continue longer than previously anticipated through 1H17. 140bps of the decline is from executional issues on the DC front, tack on another 60bps from inventory clearance issues in 2Q16 and another 30bps in 4Q15 and we get to 230bps from supply chain issues that will start to roll off in 2Q17. In light of the promotional environment, it’s likely that PIR will compete some of that gain back in the form of price, but the margin leverage from efficiency measures + lease negotiations/store closures + e-comm fulfillment scale = a nice gross margin lever in 2017.

SG&A

PIR made the number on SG&A leverage with dollars down 9% YY, that largest decrease since Aug ’09. The obvious whole in the cost structure is the marketing spend which was down 16% in the quarter as the company pulled back on national TV media spend. But, let’s not forget that PIR is reaching the tail end of a 3yr e-comm buildout that not only ate away gross margin in the process but required a significant amount of spend on the SG&A side.

Balance Sheet

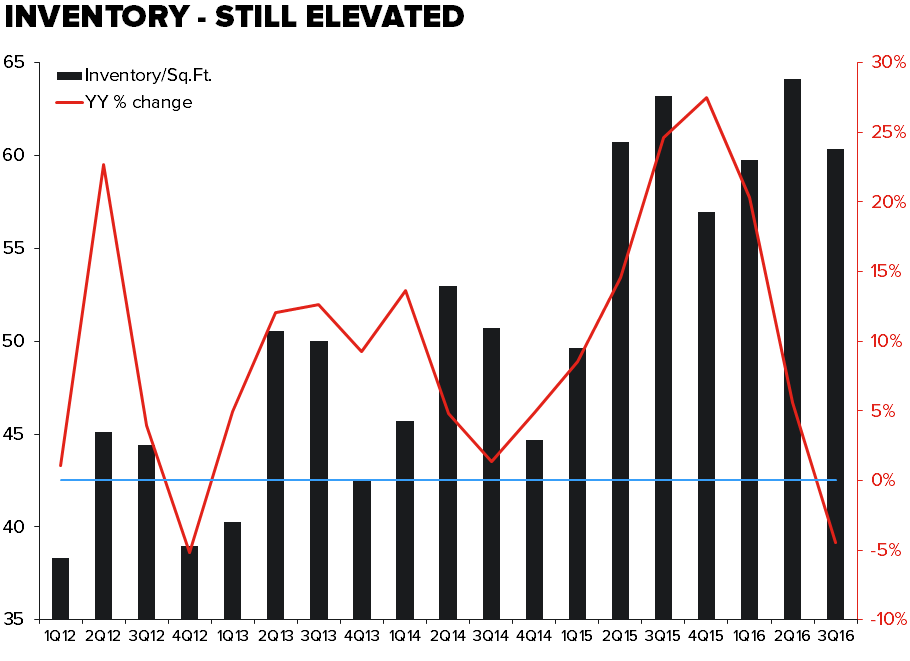

Big improvement in working capital with inventory growth down 6% YY. The sales to inventory spread went into positive territory for the first time in 2 years, and inventory per square foot was down 5% from the big build up headed into Holiday 2014. But, there is still a lot of wood to chop on that line as inventory per square foot sits at levels 36% higher than in 3Q12. You could make the argument that with e-commerce now in the mid-teens as a percent of sales and exclusive online content making up a portion of the inventory balance, that the comparison isn’t apples to apples. But, we think that a 10%-15% drop is more than possible. By our math that would free up about $60mm in working capital.