Last week we laid out the SHORT case for CMG (click HERE to view) given the issues the company is facing surrounding the consumer perception of the brand.

The non-GMO tailwind is turning into a headwind.

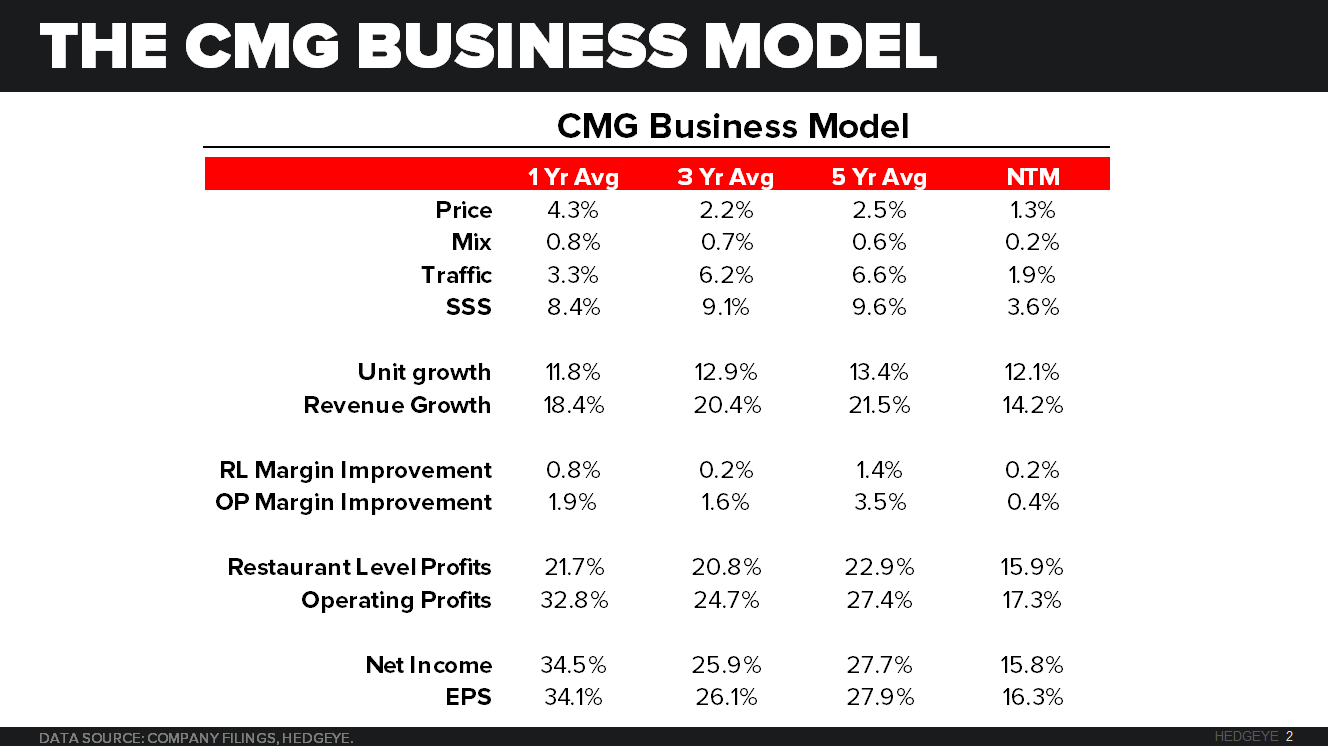

Limited pricing and declining traffic suggest a lower trajectory for same-store.

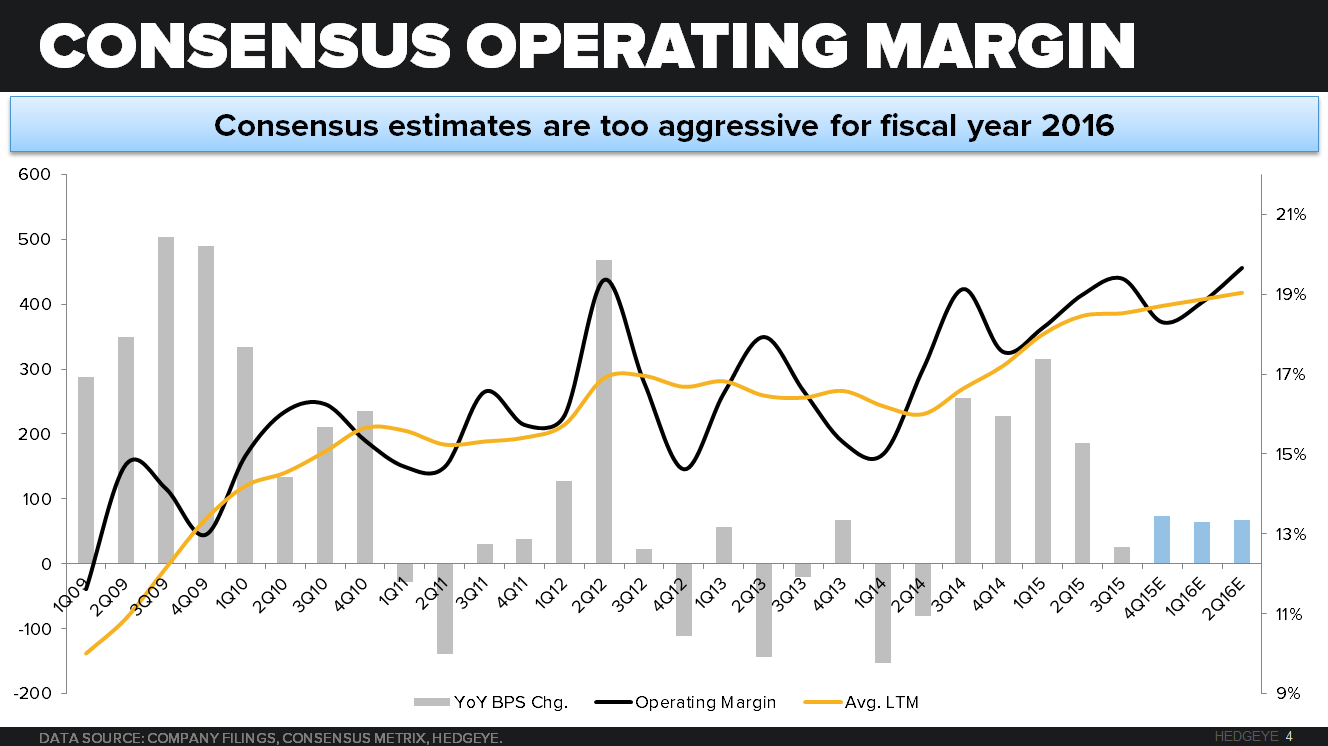

Margin pressure will ensue with slowing sales trends.

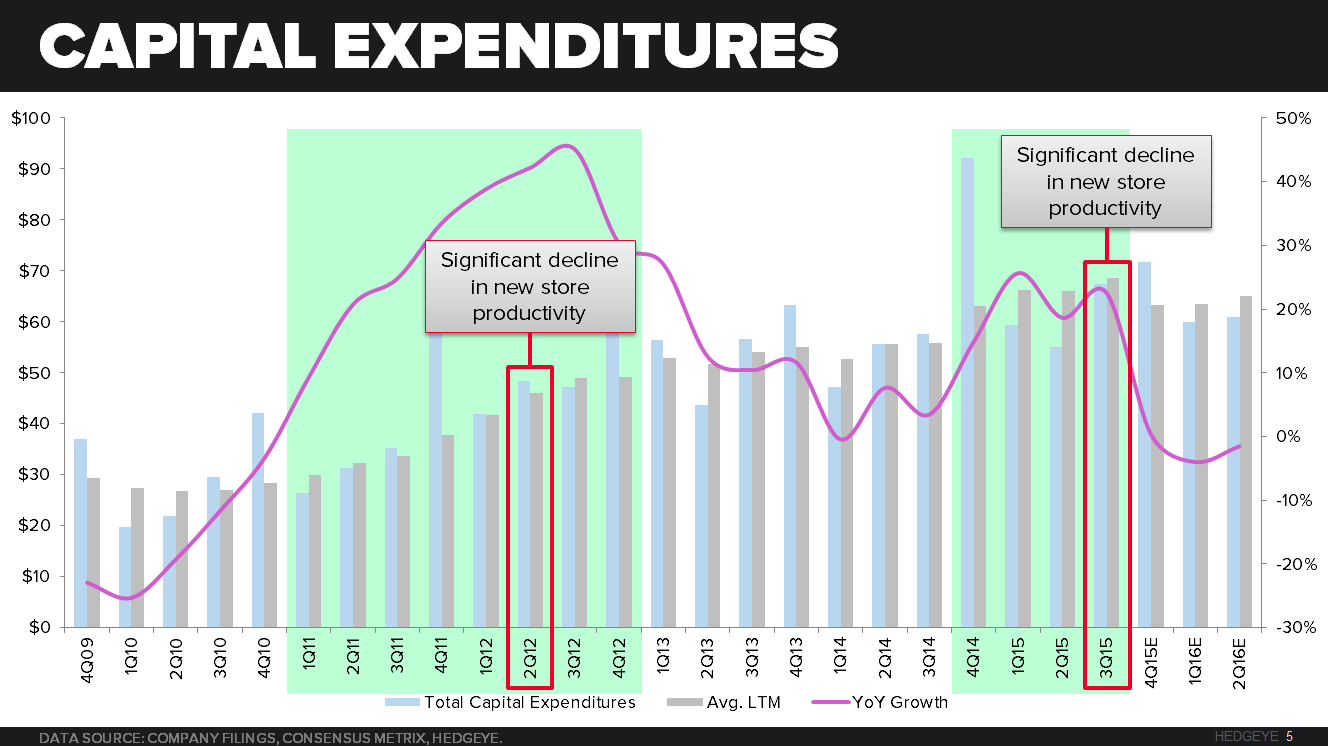

Aggressive capital spending in 2011 & 2012 led to lower productivity in 2Q12. Aggressive capital spending from 2014-2015 is leading to new lows in productivity.

Accelerated development is increasing the pressure on the entire organization (i.e. foodborne illness)

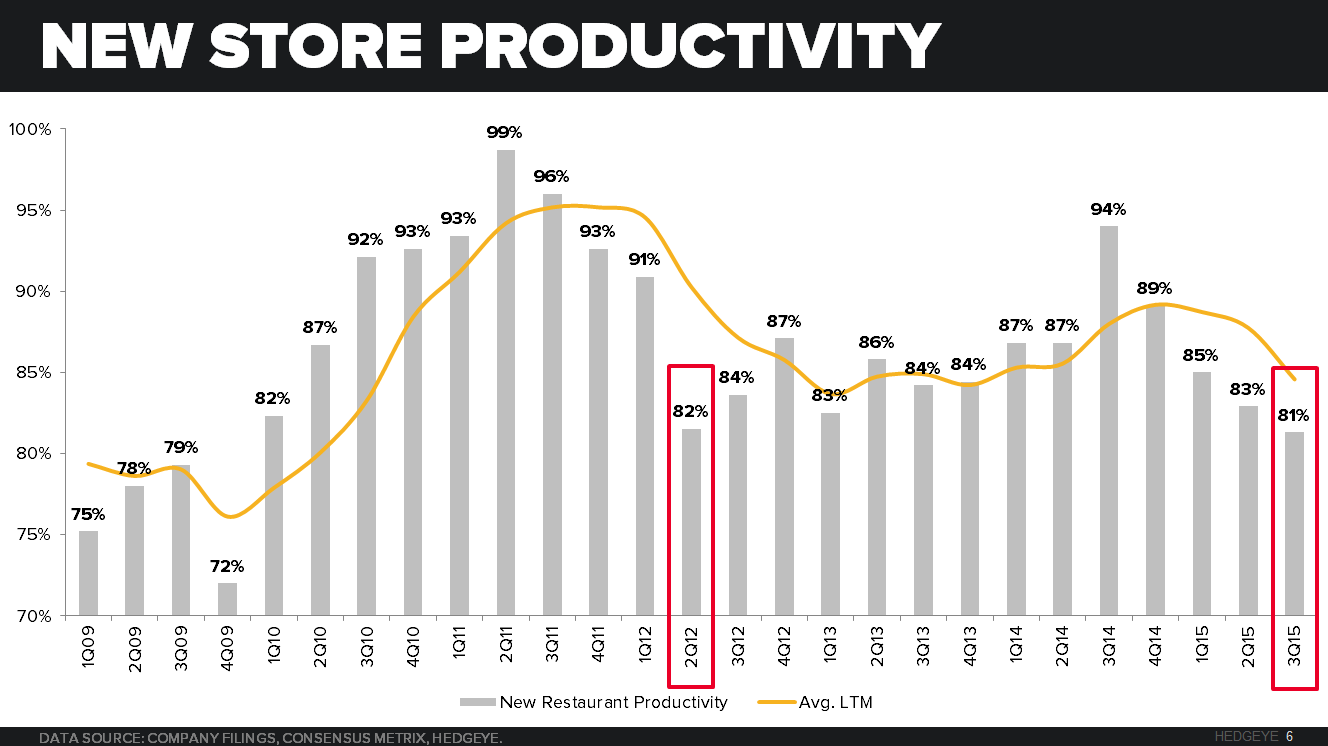

New store productivity is the ultimate arbiter of future growth. Based on this calculation, shown below, CMG's new stores have hovered at 85-95% of an existing store's volume since 2010. In 3Q15, the new unit productivity is below where it was in 2Q12. This number will likely head lower in the coming quarters.

Accelerated unit development in 2016 will only make the problem worse.

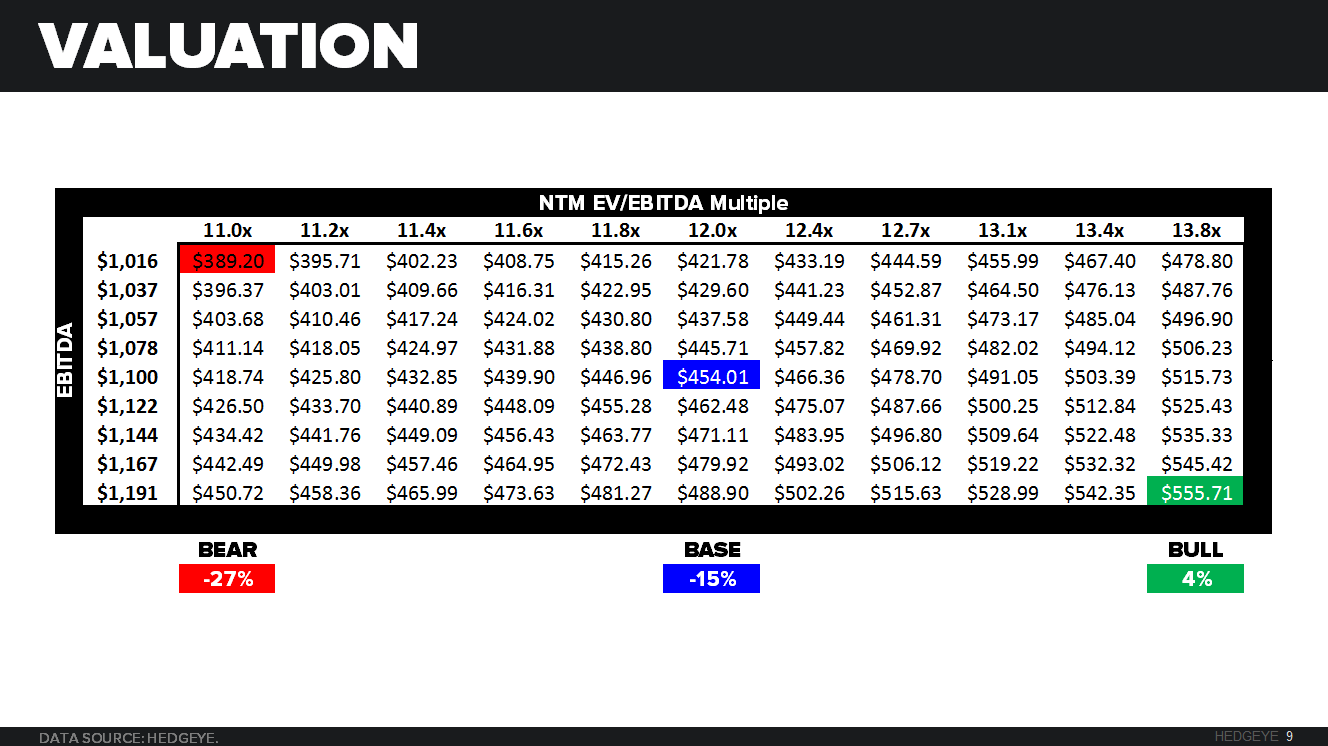

The stock will adjust to a slower growth; lower margins and lower returns and a lower multiple.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst