This was absolutely not a good quarter from WSM. Sales growth was decent at 7.8% – but to be clear, the company bought it. Gross Margins were -112bps, leading to Gross Profit growth of just 4.6%. And if the company didn’t pull the goalie on the SG&A line (corporate), EBIT would have been down 6%. To be clear, this was the WSM’s greatest SG&A leverage this cycle – and on a mediocre comp. Add on a lower tax rate, and earnings would have been $0.13 lower than the reported number, or an $0.08 miss. Oh yeah…cash flow was down 50%. No one talks about that. We’re taking our 2016 number down to $3.70 vs the Street at $3.90. Does that make WSM a raging short? No. But we’d argue that unlike RH, only 40% of WSM’s mix is defendable in the face of a weakening consumer. All in, this stock has seen 12-13x earnings during a downward revision cycle. Let’s generously say 14x $3.70 next year – that’s a $52 stock vs $66 today. We’ll take that.

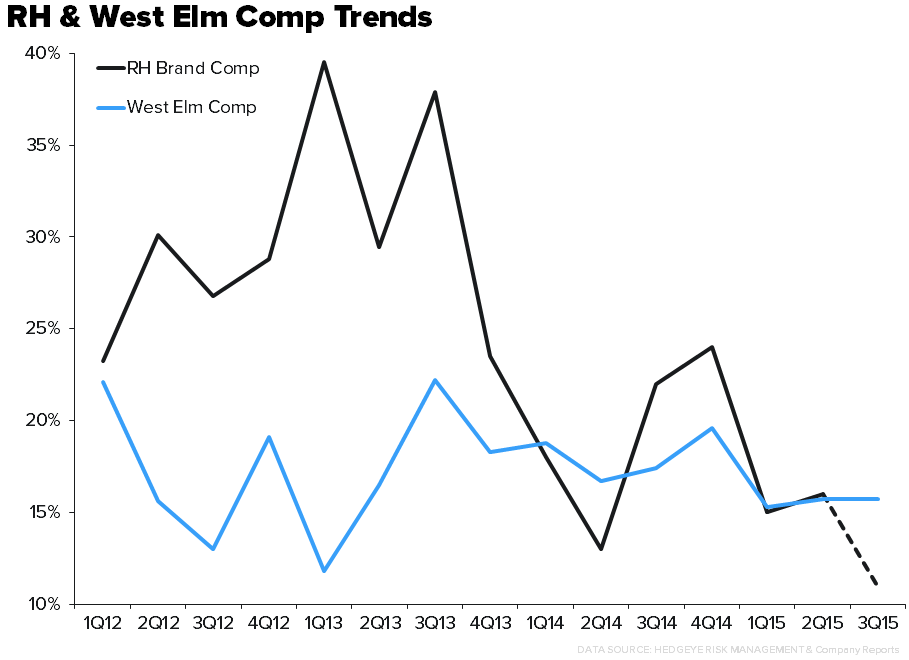

Comps – The company actually missed comp expectations by 50bps though sales beat as International revenue made up the difference. But, all concepts with the exception of Pottery Barn showed underlying strength accelerating on a 2yr basis. Ex-West Elm, by our math the company put up a 2.5% comp the lowest number since 4Q12. As noted above the company bought the comp.

Weak Guidance – WSM guided the mid-point of comps, sales, and earnings 200bps, 2%, and 6% below the street, respectively. There seemed to be a fair amount of caution embedded in the guide as the company held full year guidance and backed into the 4Q implied numbers with little confidence in the outlook for Holiday. That’s what happens when the rest of retail is imploding, mall traffic remains weak, and the 4Q comp is much more levered to things like Peppermint Bark and gifting than actual home furnishings. 4Q numbers look hittable, but the lack of a ringing endorsement by the management team is worth calling out.

West Elm – i.e. the only concept within the WSM family of brands that is growing square footage put up a 15.7% comp in the quarter which equated to a 40bps acceleration on a 2yr basis sequentially. The concept has always been a good bell weather for RH from a directional standpoint. The consumer/concept are much different, West Elm productivity is in the $800/sq.ft. range compared to RH at $3,300 (inclusive of e-comm) in the same size box, but it’s the only concept growing square footage. We are modeling a divergence in 3Q15 as RH pushed its growth into 2H from 1H with the release of two new concepts this Fall (Modern and Teen).

GM – was down 110bps in the quarter, with merch margins relatively flat offset by dilution from International franchise growth and increased shipping expense as WSM continues to iron out its inventory position from the West Coast port contract dispute that we should mention was resolved nine months ago (and yet the company still talks about it). On the shipping front, new rate hikes at FedEx and UPS haven’t hit the P&L, so this was all self-inflicted. Each of the negative drivers on the GM line appear to be unique to WSM and shouldn’t be contagious to a name like RH.

SG&A – SG&A leveraged by 95bps with all and then some of the leverage attributable to unallocated corporate expenses, which was down 100bps (the best leverage we’ve seen this cycle). By our math that’s an $0.08 benefit to earnings or all and then some of the 3Q beat. If International (which was called out as the biggest drag to Gross Margin) is in fact EBIT margin accretive, we didn’t see it this quarter. Holding the unallocated corporate expense % of revenue line flat in the quarter EBIT would have been down 6% instead of up 6%.

International – We’re not convinced that this is a winning strategy for WSM. It’s not a new thought to call out the fact that WSM is desperately looking for growth in any corner of the globe it can get its hands on, but the gross margin drag we saw this quarter isn’t a one off, and the EBIT accretion associated with that trade off didn’t show up. Consider this for a second, RH hired Doug Diemoz, previously of WSM, back in March of 2014 (he has since left to be the CEO of Crate & Barrel). At WSM he was charged with structuring the International licensing agreements for Pottery Barn in the Middle East. So, RH acquired first hand knowledge on the ins and out of that business and has subsequently talked down its International growth opportunity.