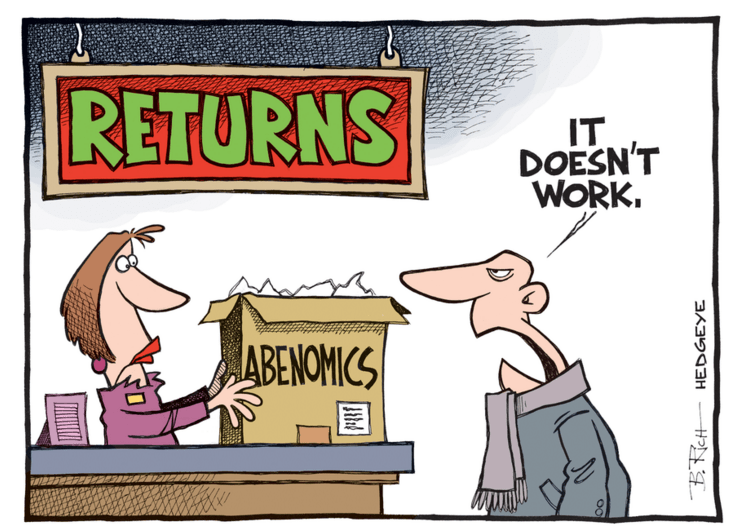

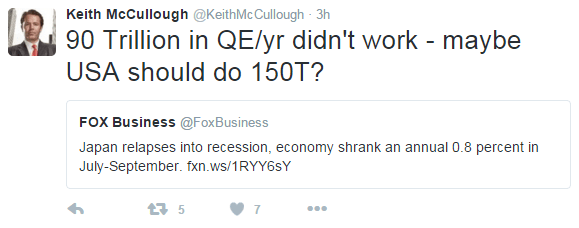

The Bank of Japan has been purchasing 90 trillion yen worth of government bonds annually, which began in early 2013, in an effort stimulate economic growth. It's part of Abenomics, the concerted effort put forth by Prime Minister Shinzo Abe to pull Japan out of it's decades long slump.

It is failing.

This is something we've been concerned about for a while now. Take a look below at a brief excerpt from our 73-page Q3 Macro Themes presentation released in early October:

"... We do not think investors are appropriately positioned for a likely trend of negative revisions to the respective growth outlooks in the U.S., Eurozone and Japan throughout the balance of the year."

We could pull up any number of recent headlines that suggest as much about global growth, but the latest news out of Japan is more than just an intimation. It's a direct confirmation of our #GameOfSlowing macro theme.

Here's Reuters:

"Japan slipped into its fourth technical recession in five years between July and September - spotlighting how the government's "Abenomics" policies have struggled to drag the economy out of chronic stagnation.

Official data on Monday showed the world's third-largest economy shrank an annual 0.8 percent in July-September after a 0.7 percent contraction in the prior quarter, putting it firmly into recession - two consecutive quarters of declines."

Interestingly, Japan's Economics Minister Akira Amari blamed the recent contraction on an overhang in inventories and (wouldn't you know it) sounded a positive tone on the country's recent jobs and income data.

This should sound familiar.

New York Fed president Bill Dudley talked up the same playbook last Thursday:

- "... the fundamentals supporting domestic demand look quite sturdy. For example, consumer spending has been well-supported by real income gains and rising household net worth."

- "It is also important that the forward momentum in the jobs market persists."

- "A large decline in the pace of inventory accumulation was the main reason why real GDP growth faltered in the third quarter."

The parallels would be comical were it not so troubling. As Hedgeye CEO Keith McCullough continues to write, "The Fed’s ‘forecast’ is wrong 70% of the time. They are the new market risk.”

So too is Abenomics.

But we digress...

The Nikkei index was down over 1% on the news that the economy had slid into recession. We'll have to wait and see how this changes the monetary calculus of the Bank of Japan at their rate review next week.

The recent news is a confirmation of our initial take on Abenomics. So we'll reiterate: