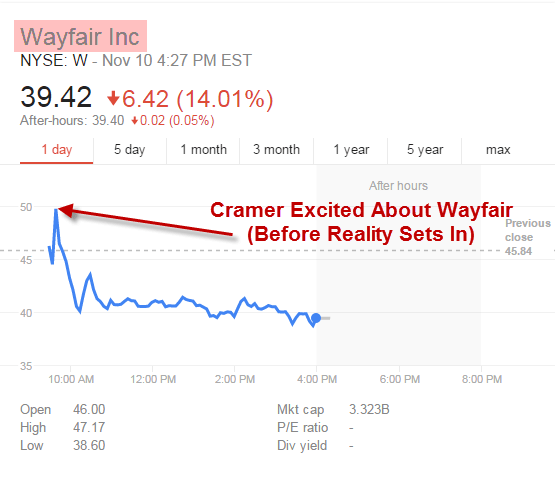

Earlier this morning, CNBC's Jim Cramer was on TV at the open trumpeting Wayfair (W) which had just released its earnings. He said the numbers were great and that the online furnishings company was "the most important stock in the market today."

Huh?

Wayfair closed down 14% today. While shares popped at the open to just shy of $50, reality soon set in. Take a look at the chart below.

For the record, our Retail analyst Brian McGough has Wayfair on his Best Ideas Short list. Here's an excerpt from a research note he sent to institutional subscribers after Wayfair reported earnings:

"Consider the following…a) Wayfair added $266mm in revenue – an astonishing number. But the company still lost money. True, the operating loss narrowed, but only by $13mm. That pegs the company’s incremental margin at only 5.1%.

To be clear, companies like Restoration Hardware and Williams-Sonoma – who are consolidating a different end of the home furnishings market (the good end) have incremental flow-through rates of about 20-25%. Heck, even AMZN, which is not afraid to lose money for a very long period of time, has an incremental margin of 15%. Then why are we looking at 5% for W?

The bottom line is that this company is spending – and it’s spending big – around penetrating what management believes to be the company’s TAM. Unfortunately, we think they are overestimating it by a country mile, and are building an infrastructure for growth that will not materialize – at least profitably."

Key to McGough's short thesis is the estimation of Wayfair's addressable market. The company's management puts that number at $90 billion.

"That’s just flat-out wrong," McGough writes. Here's another excerpt:

"We’ve done extensive research on this one, and when all is said and done, we think that the end market is no more than $30bn. To put that into context, it suggests that Wayfair has about 10% share of its market. That’s 2-3x the share of players like RH and IKEA. There’s absolutely no reason why this should be the case."

Why? Because most consumers buy furniture and home goods through a combination of online research and in-store visits. Wayfair is an online-only shopping experience. As McGough writes, "you can't touch and feel the seven million items sold by the company." By his estimation, Wayfair consumers don't ‘blind buy’ above $750. That's "well below the prices listed for furniture sold on its websites."

Bottom line: We'll gladly take the other side of Cramer on Wayfair any day.