In a note to subscribers earlier this morning, Hedgeye CEO Keith McCullough laid out an under-appreciated effect that a poor U.S. jobs report would have on bonds.

"We’ve only seen 8 alleged “breakout rallies” in rates the last 10 months (and every one of them has been quashed by that damn “data” that the Fed continues to say they are dependent on) – the U.S. labor cycle peaked in FEB and should slow well into the middle of next year."

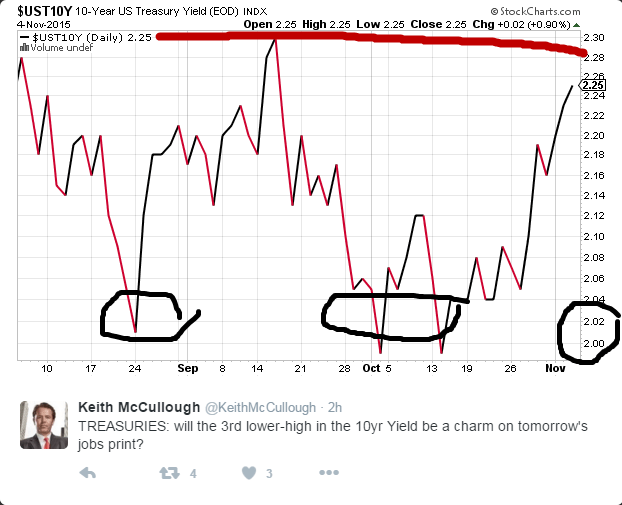

Check out the chart below. In two of the year's more recent "breakout rallies," underwhelming U.S. economic data sent 10-year Treasury yields back below 2%.

Here we go again?