“To be of championship caliber, a crew must have total confidence in each other.”

-George Pocock

That’s how Daniel James Brown brings home the final chapters of his epic championship story about 9 Americans winning Gold at the 1936 Olympics in Berlin (Boys In The Boat). And that’s how I’m going to start my week. I love excellence. Congrats to the Kansas City Royals for winning The World Series last night.

Back to the Global Macro Grind…

Instead of a big European and/or Chinese central plan (that was the catalyst for “stocks” 2 weeks ago), last week was dominated by the one thing a mediocre consensus has had wrong in 2015 – that #LateCycle US Growth continues to slow.

In addition to New Home Sales, Durable Goods, and Consumer Confidence #Slowing, the week was capped off by a big sequential slow-down in Q3 US GDP to 1.5%. The new bull case is that it ended up being “in line” with a consensus estimate that was cut in ½ in the 3 months prior.

But, no worries, everything is going to re-accelerate in Q4 (per consensus). And while we continue to have confidence that that’s dead wrong, it may take another bad jobs report at the end of this week to hammer home reality.

Pardon? I thought “everyone is bearish” so the jobs report could be bullish?

Yep. Keep on hoping for that, I guess. But there is absolutely nothing in our long-term cycle work that suggests the labor market stopped slowing in October. US layoff announcements actually hit new YTD highs.

Taking a step back, here’s what macro markets did last week:

- US Dollar Index traded sideways and finished the week -0.2% (after being +2.6% in the week prior) and is +7.4% YTD

- EUR/USD was flat week-over-week at $1.10, post the week prior’s Draghi Devaluation of -2.9% taking it to -9.0% YTD

- US 10yr Yield bounced 6 basis points on the week to 2.14% after re-testing the low-end of its 1.99-2.19% risk range

- CRB Commodities Index had a +1.0% bounce on the week (after deflating -2.9% in the week prior) and is -14.9% YTD

- Oil (WTI) bounced +4.5% on the week (after deflating -6.3% in the week prior) and is still in crash mode -21.6% YTD

- Gold deflated another -1.8% week-over-week and remains -3.8% for 2015 YTD

- Copper deflated another -1.4% week-over-week and continues along its recessionary path at -18.1% YTD

- SP500 closed the week +0.2% after having a big slow-volume bounce of +8.3% for OCT to +1.0% YTD

- Russell 2000 deflated another -0.4% week-over-week and remains -3.6% for 2015 YTD

- US Equity Volatility (VIX) rose as many asset classes fell, closing +4.2% week-over-week after correcting -38.5% in OCT

In other Global Equities “are back” news:

- European Stocks (EuroStoxx600) lost -0.5% on the week

- Emerging Market Stocks (MSCI Index) deflated another -2.4% week-over-week

- Latin American Stocks (MSCI) remained in #crash mode, dropping another -2.2% on the week

Yeah, Europe and Latin America (and maybe China?) is where all the new labor market “demand” is going to come from in Q4, eh? Cool. US Dollar denominated debt #Deflation Risk remains one of the most misunderstood for US equity market navel gazers.

Here’s another way to slice and dice last week’s performance - US Equity Style Factors (SP500 Companies) to continue to avoid:

- LEVERAGE – High Debt (EV/EBITDA) companies lost -1.0% last week and are -7.0% in the last 6 months

- BETA – High Beta Stocks lost another -0.6% last week and are -11.5% in the last 6 months

- SIZE – Small Cap Stocks were -0.2% vs. Large Cap +0.4% last week, taking Small Cap -10.8% in the last 6 months

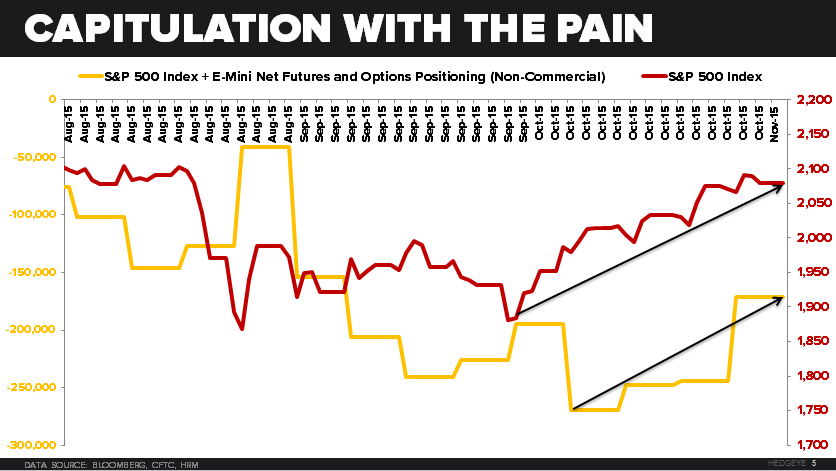

Finally, from a sentiment perspective, CFTC non-commercial Futures & Options net positioning saw the YTD highs in NET SHORT SP500 Index + Eminis from September melt-down by 72,584 contracts (covered) week-over-week.

That’s nice, because it’s a lot easier to have confidence in maintaining a bearish small cap, beta, leverage, etc. view when a consensus that wasn’t Bearish Enough to begin with (in JUL) doesn’t trust the short positions they put on at the AUG-SEP lows!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.99-2.19%

SPX 2015-2096

RUT 1135--1175

VIX 13.76-19.40

EUR/USD 1.08-1.11

Oil (WTI) 43.31-47.09

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer