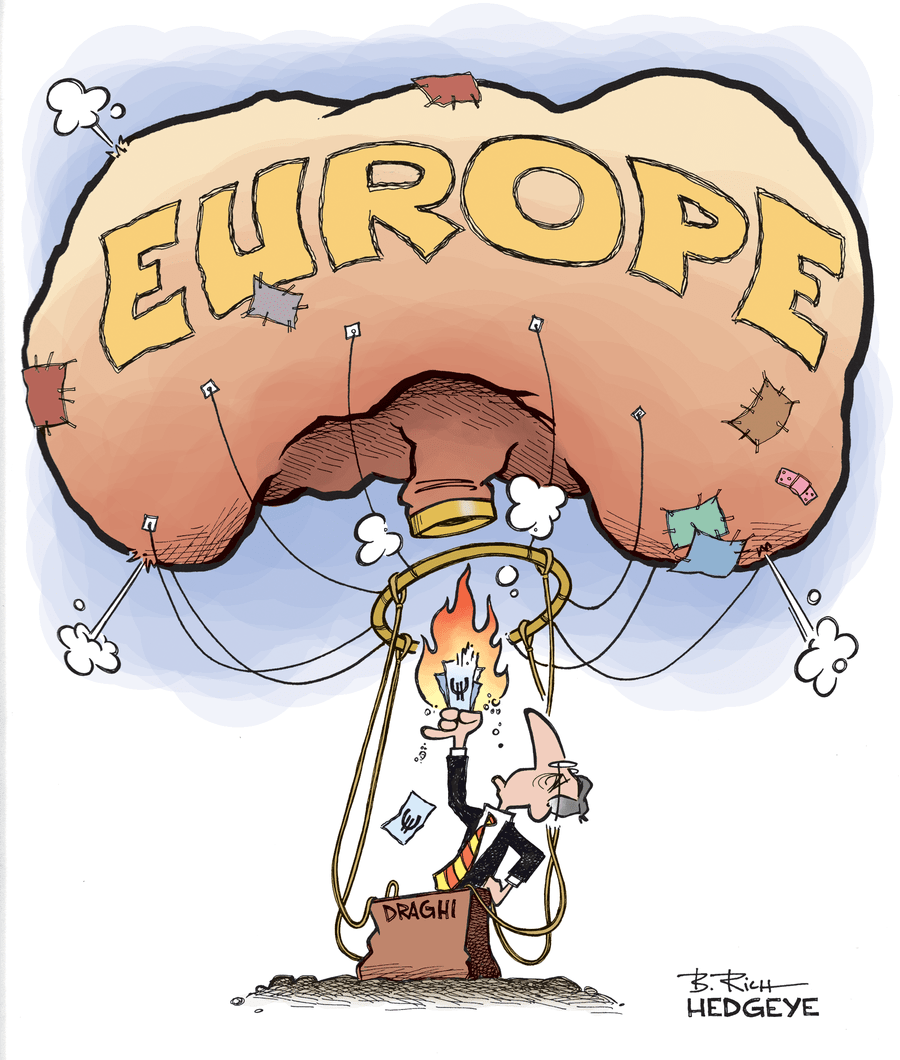

Mario "Whatever It Takes" Draghi Full of Hot Air!

* * *

So... ECB head honcho Mario Draghi (more than) hinted that additional monetary stimulus is on its way. Like his central-planning cousin Janet just across the pond, Mario loves that monetary cowbell. The ECB governing council apparently had a “rich discussion” about what accommodative monetary instruments might be used in the not-too-distant-future.

On The Macro Show this morning, Hedgeye CEO Keith McCullough explained the ramifications of what more monetary easing means. Here are some highlights:

U.S. Dollar

“The euro crept up a little bit yesterday to 1.15 versus the dollar, with everyone questioning that Draghi may not bring the thunder. That changed today. If it breaks 1.11, there’s going to be a mad rush to 1.05. If it gets to 1.05 on the euro you’re going to get 100-something potentially on the U.S. Dollar index. That is going to wreak havoc. Then you get the deflation dominoes.”

Spain

“Will Draghi be able to keep Spain from crashing? We doubt it. Cowbell does not create economic growth if it’s via currency depreciation. What it actually does is devalue the purchasing values of the people. That means you need more to buy that loaf of bread."

Oil

“This is very deflationary. It is perverse, but it is what it is. Draghi devalues the euro, that takes the euro down, the dollar up, and oil and energy stocks down.”

Fed Interest Rate Decision

“The Fed is absolutely scared of its own shadow. The minute the market went down, they got scared. But now, the economic data is going down and the market is up. What does the Fed do on that? Well, they see the market react to a stronger dollar, via Draghi, and say to themselves we don’t have to tighten Draghi did that for us.”

What does it all mean?

“The Japanese taught us this, when you’ve got nothing else going on, the best security is government bonds. This is what happens when people don’t have economic growth, or hope, or anything to invest in. The core feature of a Long Bond is growth slowing.”

In other words, recent global developments are further confirmation of our firm's non-consensus macro theme #LowerForLonger and our contrarian bet on the Long Bond.