YUM is on the Hedgeye Restaurants Best Ideas list as a LONG.

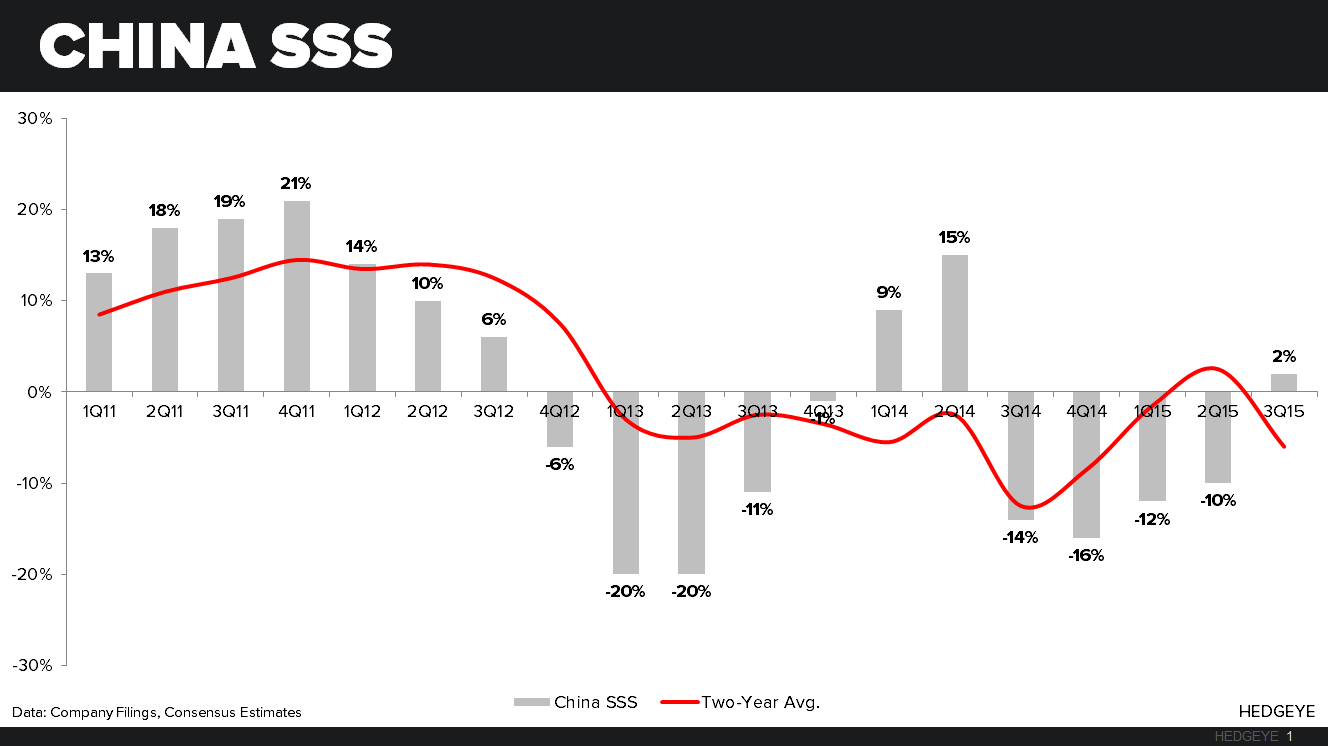

The overall performance of Yum! Brands continues to be overshadowed by the poor results from the China segment. Yesterday, YUM released 3Q15 earnings that missed estimates on the top and bottom-line, mainly due to China. Company revenues were $3.43bn, short of consensus estimates of $3.67bn. Same-Store Sales (SSS) were strong in all segments except for China and India. China posted SSS of +2%, well short of consensus estimates of +9.6%, while India posted -18% SSS versus consensus at -6%. KFC on the other hand continued to perform well, posting +3% SSS versus estimates of +2.6%, Pizza Hut continued their flat trajectory with +1% comps versus estimates of +0.5%, and lastly, Taco Bell, put up a +4% comp against estimates of +3.9%. Even with the positive performance ex-China, YUM missed on the bottom-line, reporting Q3 FY15 EPS of $1.00 versus consensus estimates of $1.06.

THE NEW FULL YEAR GUIDANCE

With the continued pressure in the China business, management has decided to lower guidance, they now expect full year 2015 EPS growth to be in the low single-digit positive range. Versus guidance delivered during the 2Q15 call, of at least 10% EPS growth.

I asked Greg Creed at the analyst meeting last November what he wanted his legacy to be as CEO of YUM. His answer: “to return YUM to the 10% EPS growth model of the past.” While that may sound good given the track record of his predecessor, the world has changed and so should YUM. Holding onto the past is a waste of energy, and serves no purpose in creating a new future for YUM. It’s time for CEO, Greg Creed, to solidify his legacy as CEO of YUM and forge a new path for YUM that will better serve shareholders.

More to the point, YUM’s CHINA growth model has changed and will never look like it did in the past. As opposed to 5 or 10 years ago, China represents a nasty mix for YUM – a business unit that is under significant pressure and it makes up a significant part of YUM’s financial performance.

The Board must do something to evolve the business model and reduce its exposure to China in a meaningful way. The board can de-risk the business by selling off company-owned stores in China and returning the company to a GLOBAL QSR asset light model.

YUM is a great company with three great global brands. The margin structure, balance sheet and cash flow of the company are envy to many global companies. This is highlighted by the dividend raised by 12%, slightly better than what I thought they would have done. The strength of the company can also be seen in the performance of KFC and Taco Bell, both concepts posted strong results, despite potential headwinds (KFC in emerging markets and MCD slowing Taco Bells performance).

Despite these having significant number of positive attributes, the assets in China are now a liability, and the stock will trade that way until a new path forward is determined. The clear evidence of this is how the stock traded today, down roughly 17%. The message to the company is clear - shareholders want a new way forward.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst