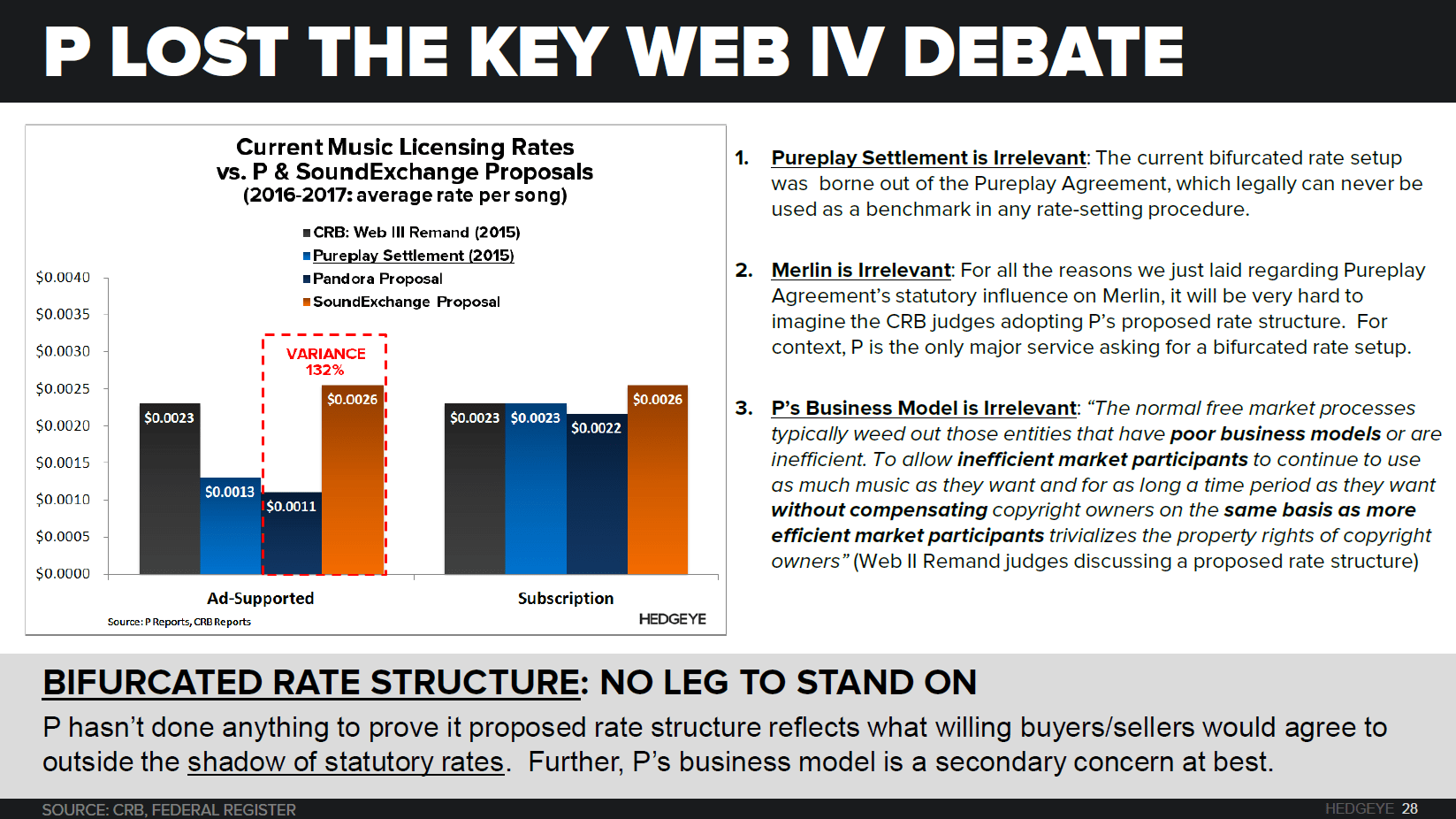

INTRODUCTION

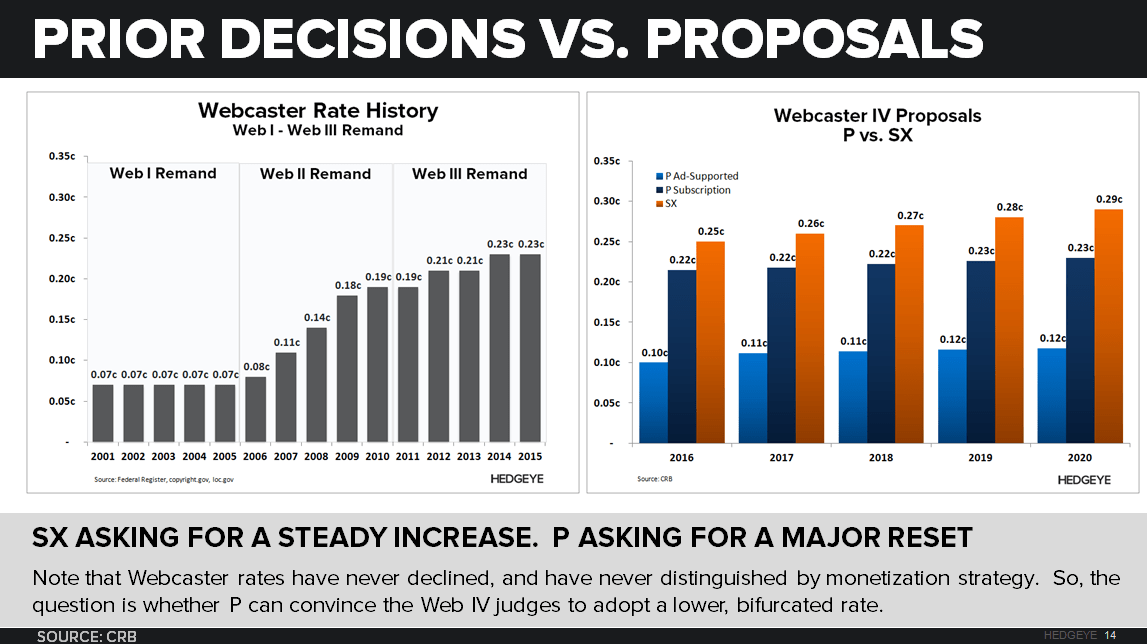

P and SX are worlds apart in their proposals, but the big difference is that SX is looking for a steady increase off the Web III rates, while P is asking for a massive reset. We can all exchange jabs on who has the better benchmark, but unless P is the clear winner, it will likely be the loser since its proposal is the one that deviates most from prior rates set by the CRB (see the below quote for context). In short, P was playing from behind before the game even started.

“the rates in these negotiated agreements serve as a caution to us not to depart radically from past rates where we cannot be confident, based on the quality of the benchmark evidence in the record, that the magnitude of such a departure is fully supported in the target market.”

- Web III Copyright Royalty Judges

As we mentioned during our call last week (P: Webcaster IV = Powder Keg), the benchmarks matter most, and this is where P has the weakest argument of all the players involved. Below we discuss each of the major benchmarks, with supporting slides from our deck.

BENCHMARKS

- IHRT (Warner Deal): The deal includes a series of benefits not covered by the statutory license, particularly a revenue share opportunity for terrestrial radio, which IHRT doesn’t have any legal obligation to pay WMG for since terrestrial is considered promotional. For context, terrestrial represents the overwhelming majority of radio consumption in the US (vs. internet). Further, IHRT's effective rate for the WMG deal was supposedly recalculated at $0.0017/spin at final arguments vs. the $0.005 it previously submitted (we're still trying to verify). What we do know is that SX calculated the effective rate for the IHRT-WMG deal at $0.00309/spin (for the 10/2013-5/2014 period) after attempting to adjust for perceived calculation errors and extra-statutory factors. IHRT doesn't appear to make any attempts to adjust its own benchmark for these extra-statutory features in its Proposed Findings, so it would seem that if $0.0017/spin is indeed the effective rate, that would be the lower bound of the zone of reasonableness, not the upper bound, especially considering the terrestrial radio revenue share in the deal.

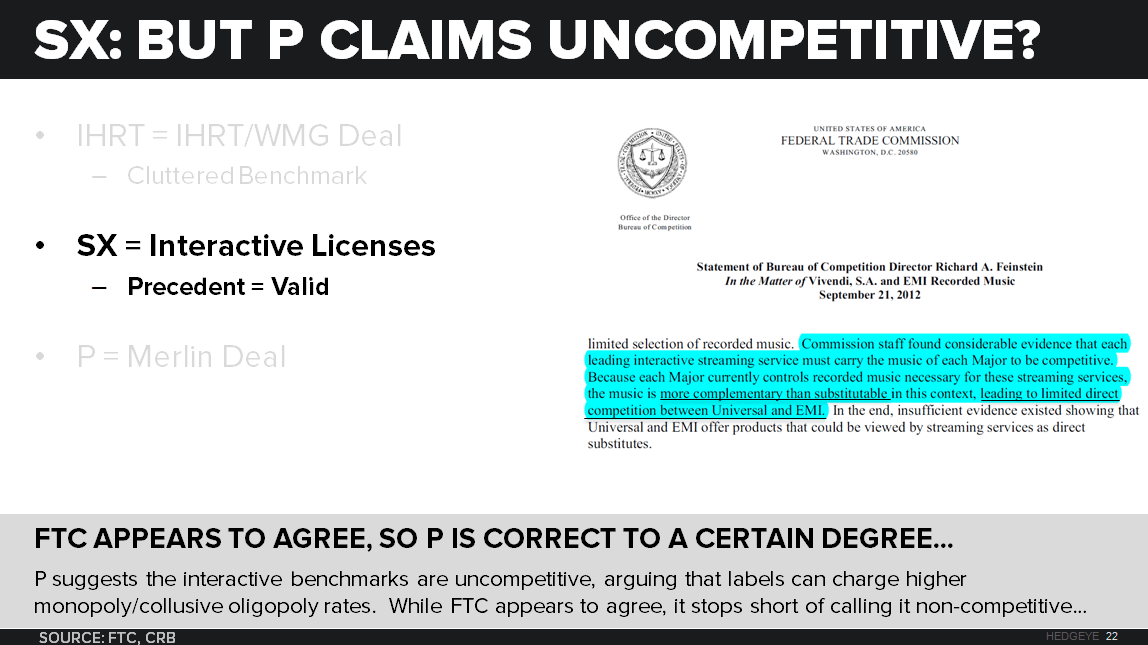

- SX (Interactive Deals): SX's benchmark is derived from 80+ interactive agreements. Note that outside the ability to choose specific songs, interactive and non-interactive are largely the same service, buyers, and sellers. Further, the Copyright Royalty Judges (CRJs) in both the Web II and III proceedings used the interactive benchmarks as a baseline for setting rates. The question is what is the appropriate interactivity adjustment, with SX calling for 2x based on the ratio of retail subscription prices in the interactive vs. non-interactive market, and P calling for 4X based on the ratio of total webcaster revenues in the interactive vs. non-interactive market. The former was the same analysis used by SX in Web III, which the CRJs adopted with downward adjustments. The latter essentially calls for a greater interactivity discount given the lower relative monetization levels of a non-interactive webcaster (primarily ad-supported) vs. an interactive webcaster (primarily subscriptions). Since P is the largest non-interactive player in the market, P is essentially asking the judges tailor the rate to suit its model. Note that all of the CRJs in every Webcasting proceeding before Web IV suggests that they copyright licensee’s business model (e.g. P's ad-supported model) is secondary concern at best for determining rates under the willing buyer/seller standard (see slides below and email us for direct quotes).

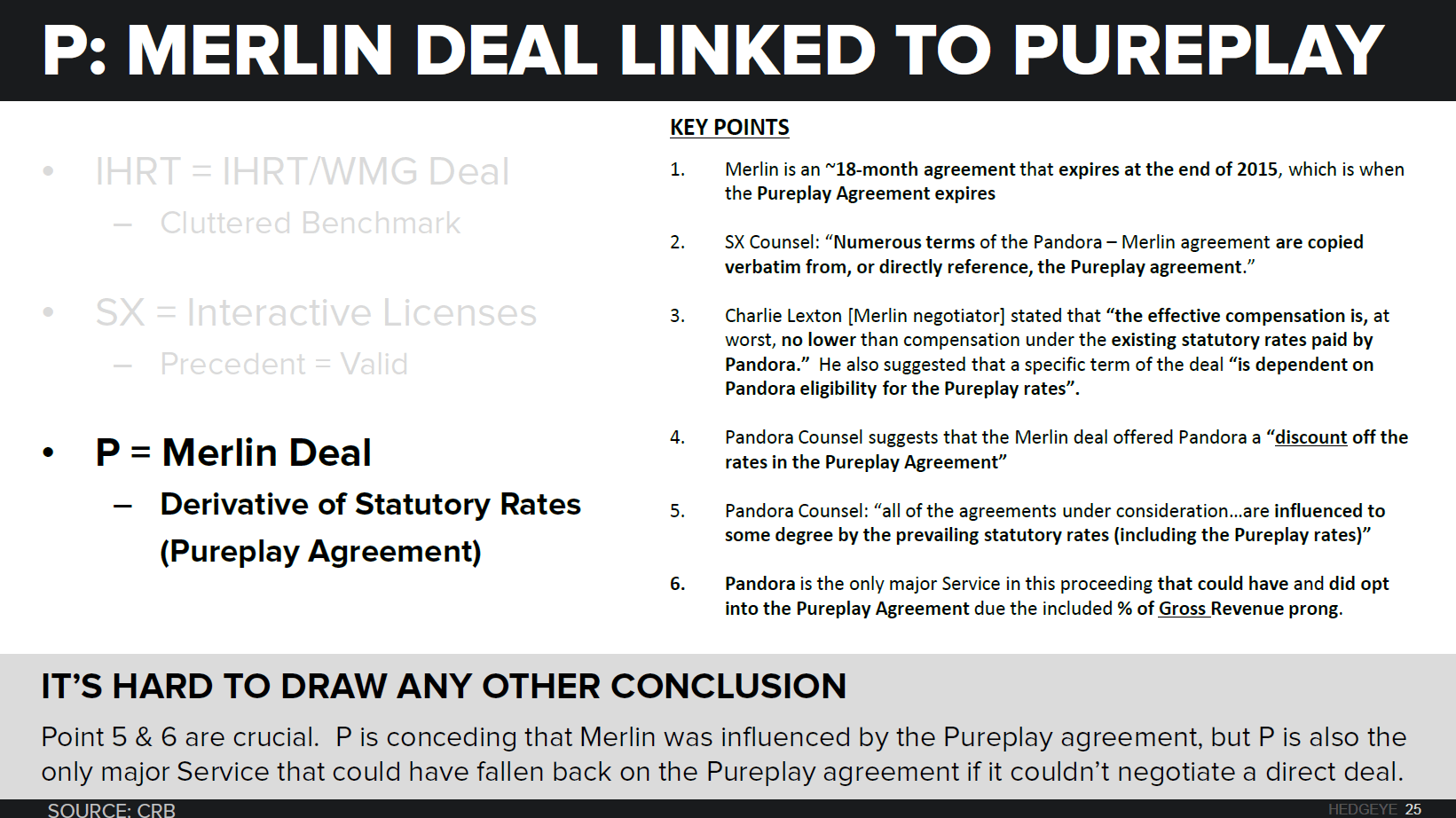

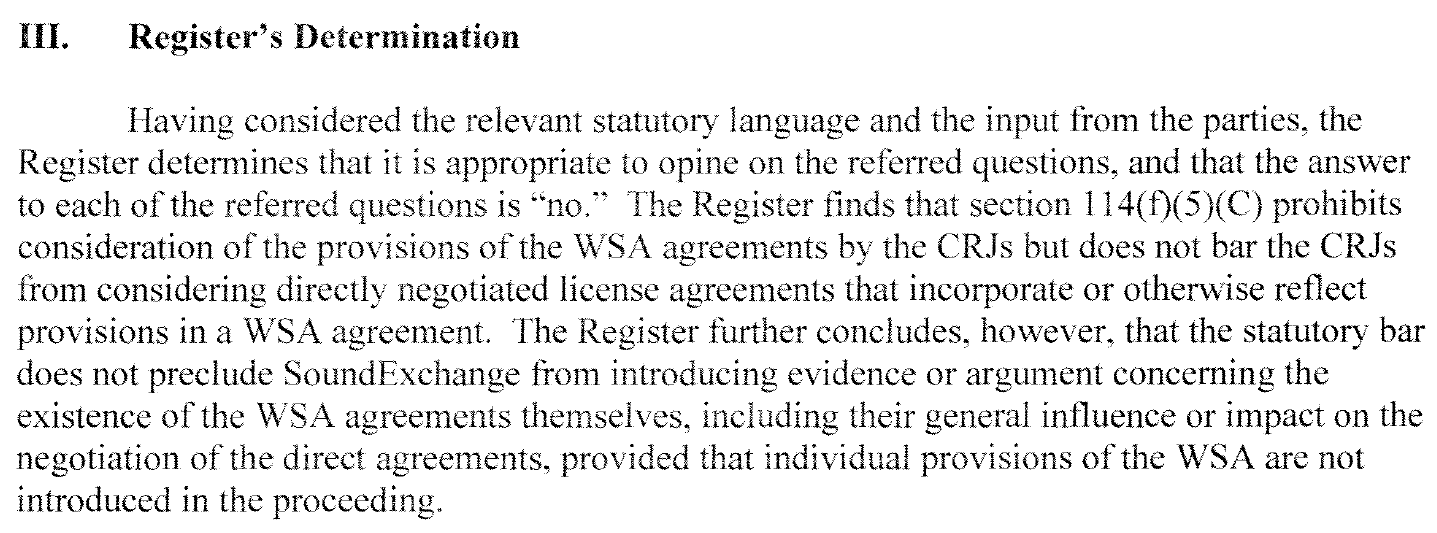

- P (Merlin): We’re not sure why one 18-month deal between P and an entity that represents 5%-10% of P’s total spins could receive the greatest weighting as a benchmark for what a willing buyer/seller would agree to over the next 5 years; regardless of statutory influence. But that’s the major issue. All the CRJs agree that their role is to establish rates that would have been negotiated in the market assuming no statutory license existed. P really hasn’t done anything to prove that Merlin wasn’t directly tethered to the Pureplay Agreement, which is both the prevailing statutory rate, and inadmissible as a benchmark for setting rates (see below). Further, the Register has never "blessed" the Merlin agreement; it has never even seen the agreement. The Register's role in this process was a matter of law, not fact. The Register allowed it because it was a direct license agreement, which legally can't be thrown out. However, the Register is also allowing SX to submit the Pureplay Agreement as evidence to assess its statutory influence over the deal (see actual excerpt from decision below). All indications are that Merlin was very careful in structuring the deal so that it couldn't be separated from the Pureplay agreement, which means P has likely already lost; especially since the onus was on P to prove why the CRJs should depart radically from past rates.

Below are the slides from our call last week specifically discussing the Web IV benchmarks. Let us know if you would us to send over the the full deck and replay.

Hesham Shaaban, CFA

@HedgeyeInternet