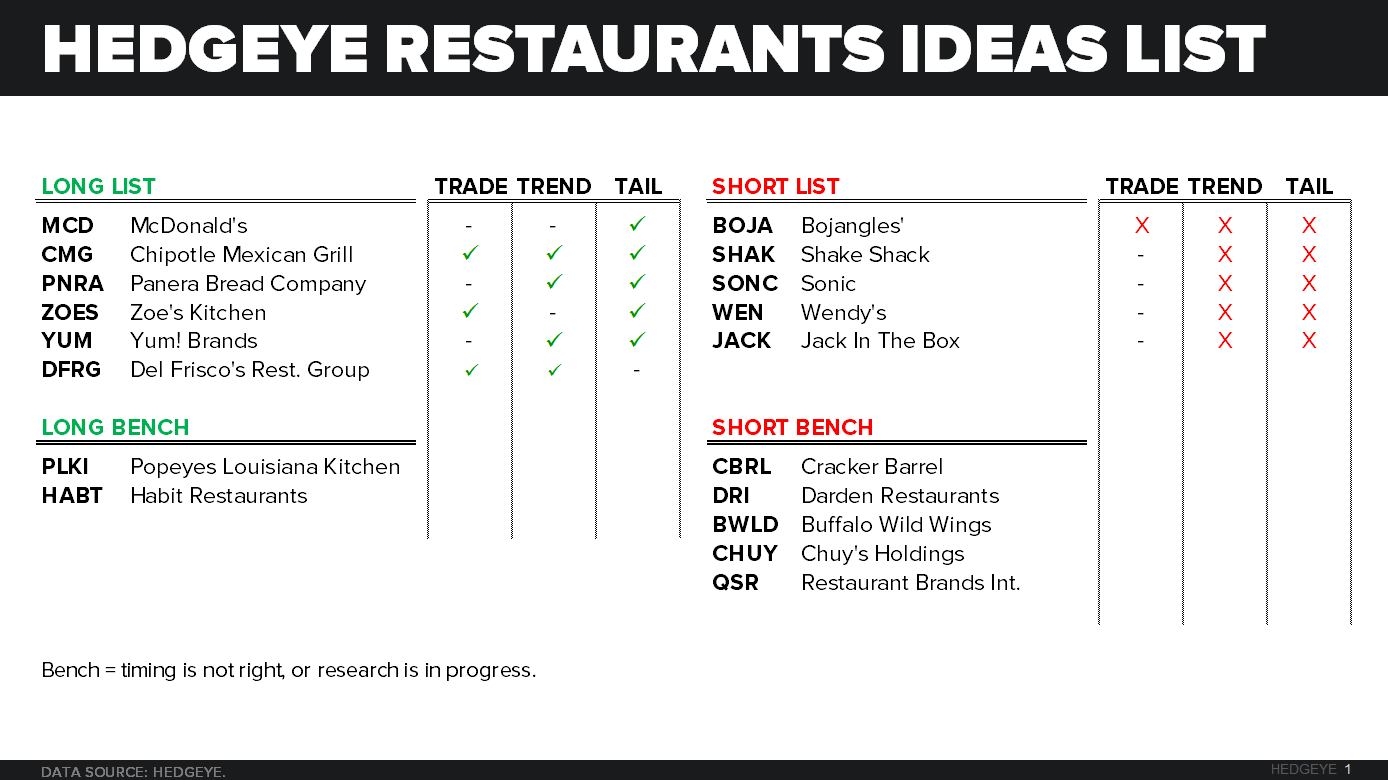

RECENT NOTES

9/21/15 DFRG | WORKING THRU THE STAGES OF GRIEF | GOING LONG

9/16/15 SHORT SMALL-CAP BURGER CHAINS | QUICK SERVICE CAN’T AFFORD $15 MINIMUM WAGE

9/15/15 August Restaurant Sales and Employment Trends

9/15/15 SONC | FIRST MISS – EXPECT MORE TO COME

RECENT NEWS FLOW

Friday, September 25

MCD | McDonald’s launches organic burger in Germany (ARTICLE HERE)

Thursday, September 24

MCD | McDonald’s named two new executives, David Fairhurst named chief people officer and Chris Kempczinski named EVP of strategy. Fairhurst an internal promote, has moved up the ranks, while Kempczinski is an external hire who previously worked at Kraft Foods (ARTICLE HERE)

Tuesday, September 22

DRI | Darden reported 1Q16 numbers that impressed, leading it to outperform the XLY by 2.9% last week. All brands had comps that beat expectations. Olive Garden, the company's most important concept, had traffic up for the quarter, but was very lump, -1.4% in June, +3.9% in July and -1.2% in August, not exactly giving us confidence in the recovery of the brand (ARTICLE HERE)

Monday, September 21

JACK | Announced a new $200mm share repurchase program (ARTICLE HERE)

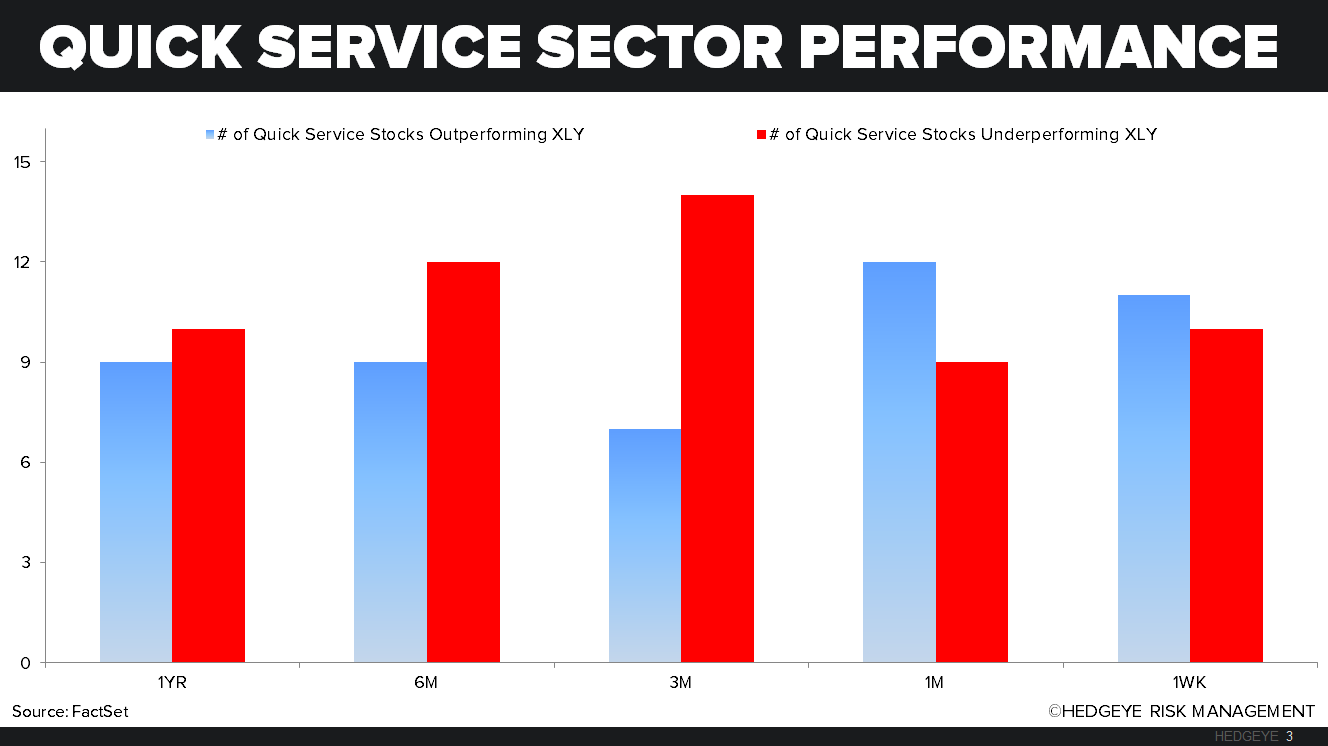

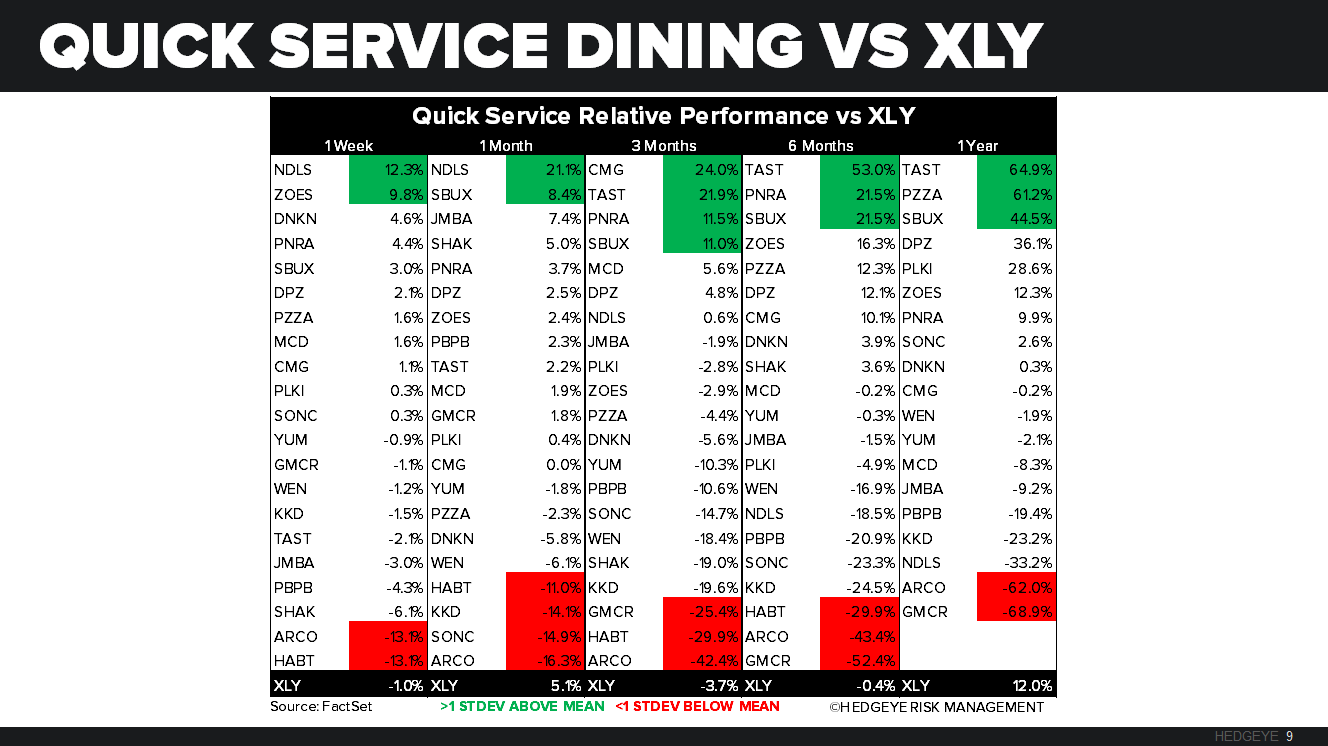

SECTOR PERFORMANCE

Casual Dining and Quick Service stocks that we follow, balanced out to match the XLY last week, with Quick Service coming in slightly above and Casual Dining slightly below. The XLY was down -1.0%, top performers on a relative basis from casual dining were DRI and TXRH posting an increase of +2.9% and +2.7%, respectively, while NDLS and ZOES led the quick service group this week up +12.3% and +9.8%, respectively.

XLY VERSUS THE MARKET

The XLY has fared better than most other sectors in the YTD time period and as of late especially. In the last five trading days, while the SPX was down -1.4% the XLY was down only -1.0%, outperformed by XLK (Technology), XLP (Consumer Staples), XLF (Financials), and lastly XLU (Utilities).

QUANTITATIVE SETUP

From a quantitative perspective, the XLY looks bearish from a TRADE and TREND perspective, TRADE support is 74.02.

CASUAL DINING RESTAURANTS

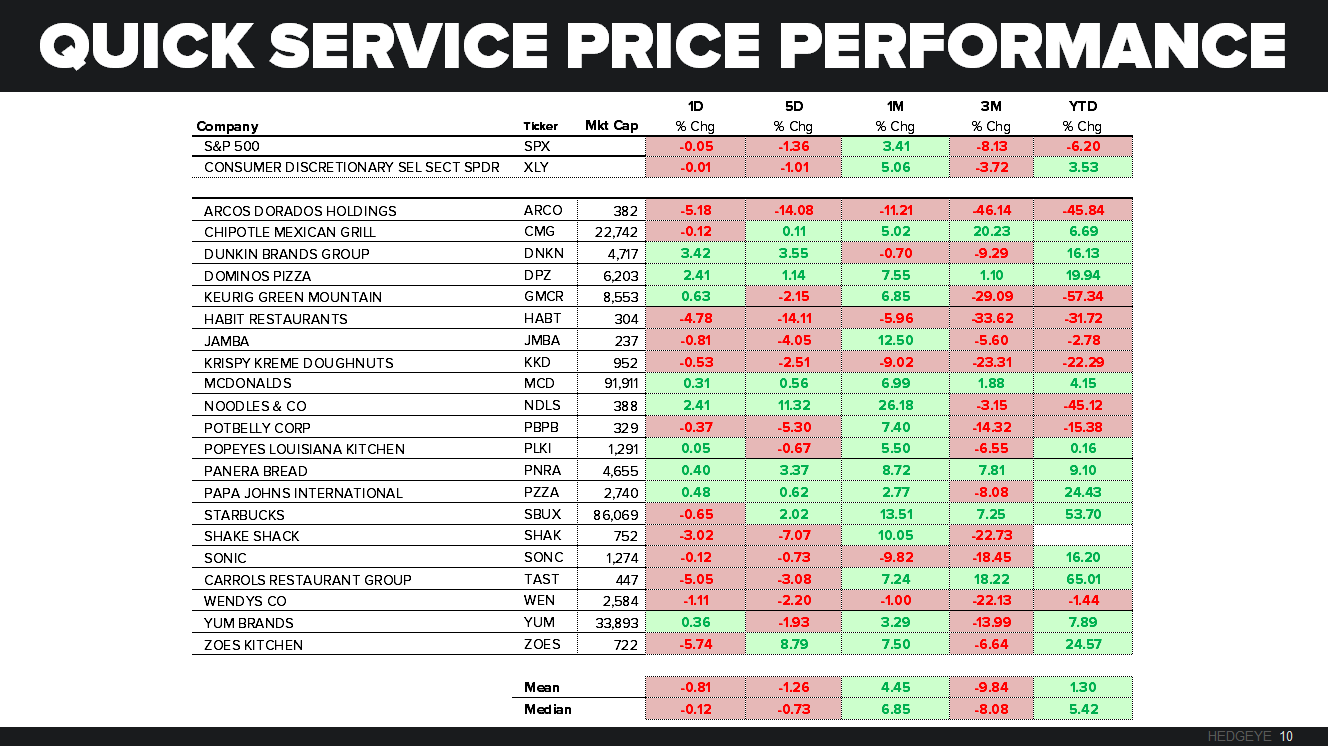

QUICK SERVICE RESTAURANTS

Keith’s Three Morning Bullets

IMF cutting global growth forecasts (again) as macro markets continue to crash:

- USD – a one-day move higher (off the lows) in USD and rates does not a credible rate hike make – no follow through so far on that w/ Yen actually +0.2% vs USD this morning (Nikkei doesn’t like that, down another -1.3%)

- RATES – bond market doesn’t believe Yellen – neither does the growth data; 0.69% 2yr and 2.16% 10yr both remain bearish TREND signals for yields as Utilities (XLU) continue to breakout (+1.2% in a down tape last wk, +2.9% in the last 3 months)

- CRASHES – Biotech stocks (IBB) moved into crash mode on Friday (-22% from the July peak) joining China, Germany, Spain, Oil, Emerging markets, etc. in what is the most visible slow-moving-train-wreck I have seen in High Beta in my career; Latin American Stocks (MSCI) -27.3% in last 3 months

SPX immediate-term risk range = 1; UST 10yr 2.07-2.21%

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst