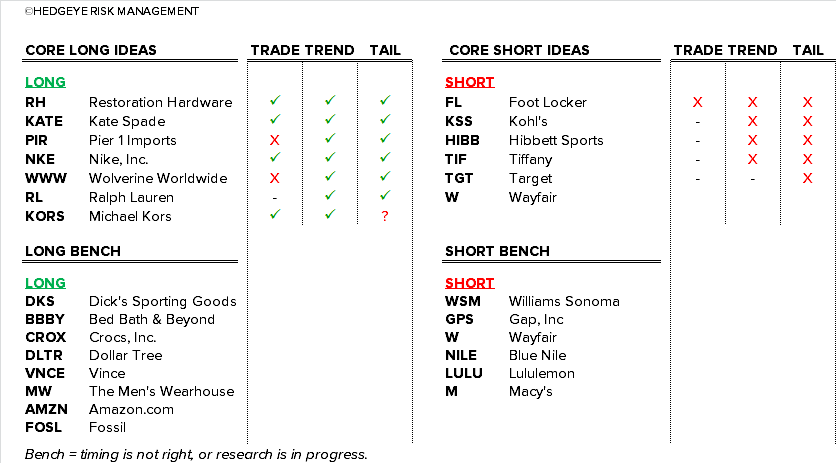

LONGS

RH: TAIL = $11 EPS and $300 stock. TRADE looks strong with Chicago opening this week, then Modern, Teen, and 175k add sq ft by Jan. This model is primed.

KATE: We think the downward spiral in sentiment is over. People are looking to own KATE again. Business is outstanding. $1.10 in EPS next yr makes this name cheap now.

PIR: One of best value stocks we can find. Capex cut, working cap improving, now 500bp of margin to recapture, which then drives top line. $2-3 down/$10-13 up.

NKE: This qtr was its best in history. But there’s likely more to come. We’ll outline puts and takes in our Nike Black Book Monday, October 12th.

RL: RL moved up to our Long list. We don’t think it will ever go below $100 again. If/when management gets the org plan right, the stock is over $200. With the stock at $108, that’s a big deal.

KORS: Does not have the momentum that KATE does, and never will (again). But evolving into more of a RL model. That’s a long transition. But at 9x EPS, we’ll assume that risk.

WWW: Under review.

SHORTS

FL: The fact that people took NKE’s results as a positive for FL is mind boggling. It’s the exact opposite. NKE DTC grew by $358mm. FINL inventories up 11% on 3% sales growth. NKE up 20% at KSS. FL has no room for error. We’re been waiting for the time on FL. We think it’s now.

HIBB: After all its problems, numbers are STILL too high. Oversaturated in core market, marginalized (by DKS/Academy) in new markets. No dot.com arm. Peak margins. Nothing but downside.

KSS: Richards and I debated pulling the plug given that this short has worked. But if our ‘credit cannibalization’ thesis is right, then estimates and the stock are going much lower.

TIF: If you don’t like the US macro setup, which we don’t, then TIF is your poster child short. It blew up twice this year – there’ll be a third. ’16 estimates are still high by $0.25-$0.50.

W: While there’s the potential for this rapid grower to print a profit by way of lower SG&A – and send the bears running for cover…the fact is our research suggests a single channel model in this space is destined to fail.

TGT: WMT is down 30% TYD and is at 13x EPS. TGT outperformed by 40% and is at 16x earnings. We’re concerned about how WMT will ultimately drive profits this holiday to offset labor costs – which won’t make TGT’s life easy. TGT also anniversarying a solid 4Q ly. Not a juicy short here, but we’ll hang onto it.