We welcome anyone to challenge our statement that this is the best and most impressive quarter in Nike’s 35 years as a public company. Our rationale is below. But whenever any company’s performance is so mind numbing – both on an absolute basis and relative to expectations – one has to wonder if there’s room to go. Is this the time to peel some off, or sell outright? The stock closed Thursday at a $99.2bn market cap. It flirted with $100bn only twice before. But Friday it will hit the triple digits, and the question is whether it will fall below $100bn ever again. We’re going to answer that question in depth when we release our Nike Black Book on October 12th (two days before the analyst meeting). But our initial sense is that the best is yet to come.

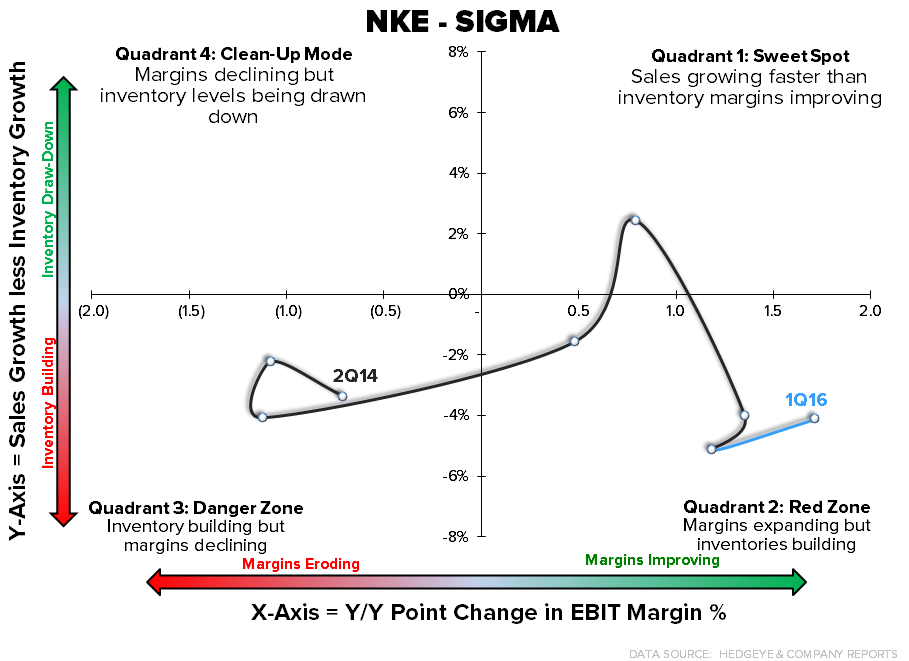

Interestingly enough, the only negative in the quarter was a high level of inventories in the US. This will be nothing more than a hiccup for Nike, but it should absolutely slow growth, or impact margins for Retailers like Foot Locker and Hibbett, two of our top shorts.

Here’s why we think this quarter is Nike’s #GOAT… (note: not all of these factors are at historical peaks, but collectively, they paint a GOAT picture).

1) Growth Algorithm. 5% top line, 7% gross profit, 17% EBIT, and 24% EPS growth. It’s tough to ask for more from a $33bn revenue company. Moreover, check out the chart below which shows that directionally, the company had a nearly identical Algorithm five quarters in a row. The number 5 is very important, because it ‘comped the comp’. There’s nothing stopping it from getting to 6, 7 or 8.

2) EBIT Growth. Despite only 5% revenue growth, this was the second largest EBIT growth quarter in Nike history as measured in incremental dollars – something that should technically not be happening in the heart of a down-cycle in FX.

3) Pure Unadulturated Growth. Seriously…this company just put up a 17% (currency neutral) futures number. We’ve only seen that once before over the past 10 years, and that includes a time period (’05) that had $20bn less in revenue. Growth should be slowing, but someone forgot to send Nike that memo.

4) Let’s put this growth into context. First off, nearly every geography and most categories are growing double digits – all at the same time. The only real negative callout is Emerging Markets. This has been a gripe for us over the past year. Last we checked, Emerging Markets are supposed to ‘emerge’ as opposed to grow at half the rate of mature markets like the UK and US. Every sport is up for Nike except for Football due to a hangover from World Cup last year (we’ll give a pass on that one). If we look at the implied dollar value growth over the upcoming futures window, that’s about $2.6bn. If you annualize it, it is the size of UnderArmour and AdiBok’s US business combined.

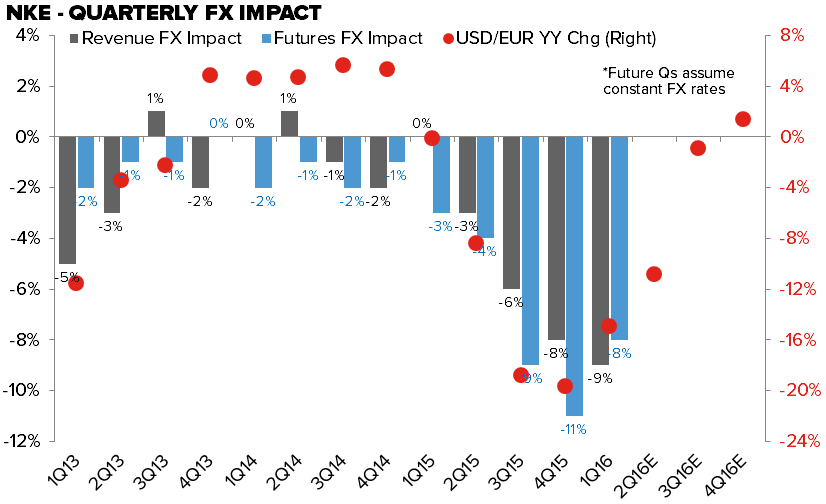

5) Currency Immune? Nope. The chart below shows that revenue is doing exactly what it should be doing given FX pressure. But EBIT is not. We still think it’s amazing that nobody questions why gross margins are positive despite the negative hit in FX. In every single past FX downcycle back to the time it started to sell outside the US in earnest (circa 1990), Nike’s margins got hit dramatically due to FX transaction impact. Did the company acquire a black box to hedge better? No. Is it making more product locally? No (though that should soon happen). The stark reality is that the massive growth ramp in e-commerce is materially padding margins – much more so than the company casually admits on the conference calls. Consider the following math. If we assume that e-comm and DTC growth (which grew at 46% and 21%, respectively in the quarter) was in line with the company average at 5%. With implied margins at e-comm of 70% and DTC of 50% that means that the base business was down 38bps in the quarter with outsized DTC growth driving 125bps of the margin change.

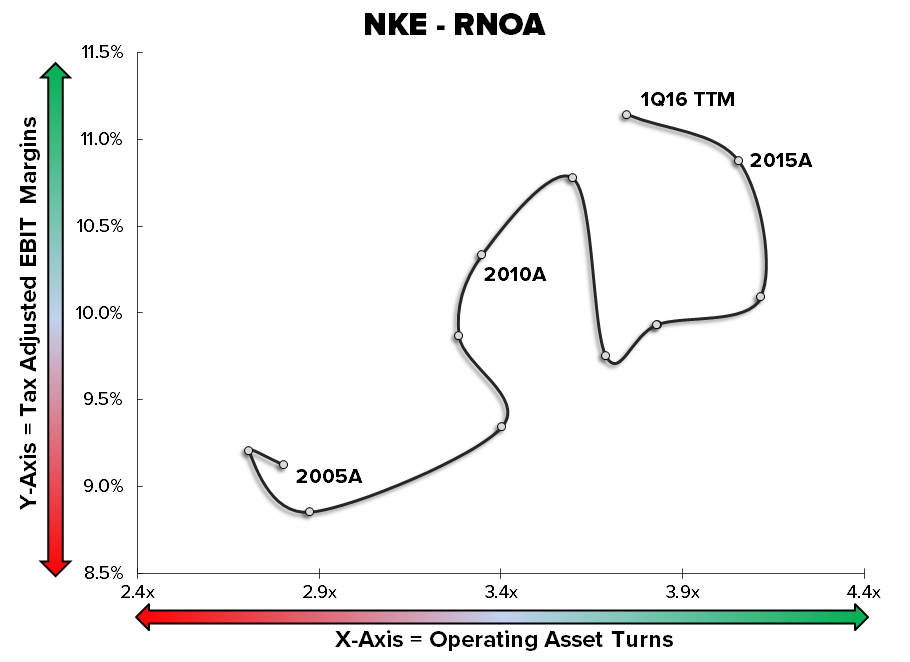

6) RNOA Looks Solid. While not perfect, due to higher inventory levels, the overall trajectory of RNOA is outstanding – sitting at 42%. As a reminder, this analysis looks at the only two things that consistently drive value creation for consumer brands and retailers – 1) tax adjusted operating margins x 2) operating asset turns. A company can usually improve any one of those in any period, but can rarely improve both at the same time. Nike is better than any company we’ve ever seen in driving value in this regard.

NKE | New NIKE Black Book

Takeaway: We’re issuing a detailed Black Book on Nike just ahead of its Oct 14 Investor Day, and will dive deep into all the key issues as we see ‘em.

There’s going to be several key areas of focus for Nike in the three weeks between NKE’s print this evening, and it’s Analyst meeting on October 14th. As such, we’ll tackle them prior to the analyst event in a deep dive Black Book and presentation on Monday, October 12th at 1:00pm ET. Key issues include…

1) Global growth algorithm – how will today’s building blocks be different in 1, 3 and 5 years.

2) US Distribution -- how much runway exists for Nike to profitably grow in the US.

3) ASP Cycle -- Where are we, what keeps it going higher, and where’s the downside risk.

4) e-commerce – why Nike sandbagged on its targets, and will sandbag again.

5) GM%: Why a 50%+ Gross Margin is achievable for Nike

6) China: How weakness in the Chinese economy could affect Nike’s growth

7) Athlete Endorsements – we’ll look at returns on athletes, which are largely diminishing

8) Competitive Landscape – especially in the US. Also how customers are becoming competitors

9) Investor Meeting: How this analyst meeting should be different from others.

Call details will be provided one week prior to the call.