First Holiday Sales Projection Bearish, Retail Facing Tough Compares in 4Q

(http://www.reuters.com/article/2015/09/22/us-usa-retail-holidays-idUSKCN0RM2WN20150922)

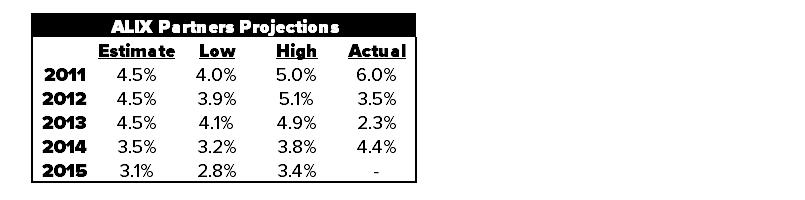

This is the first official holiday sales projection of the year, and the outlook is markedly bearish from Alix Partners. We don't think there's much of a process behind forecasts from just about any source (NRF, Alix, you name it). The track record is a bit spotty as can be seen in the table below. In fact, not once over the past 4-years has the Actual sales growth number fallen within the 'Low/High' range.

But what we do know is that, the retail sector is facing tough revenue AND margin AND working capital compares in 4Q. In what will likely be an extremely promotional holiday – we’ll see ‘free shipping’ as the most commonly used offensive weapon. We think that retailers will opt to hold the line on market share and will view weaker margins as a customer acquisition cost while most components of the retail landscape are dropping the gloves online.

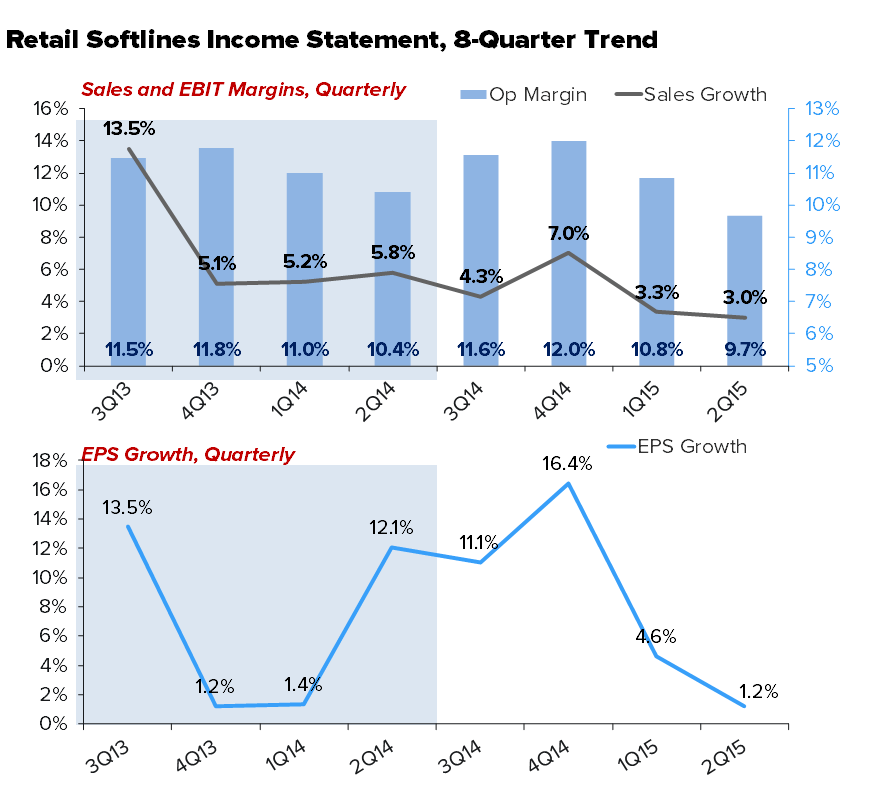

Note in the chart below that the 16.4% EPS growth for retail in 4Q14 is the highest we've seen in any quarter for the group in over two years. We think there's a far better chance of that rate going negative this 4Q than being double-digit positive. We've seen retail multiples contract by about 2 points (XRT) over the past quarter, which is twice the contraction of the overall market. So clearly, some deceleration is expected. But we still need to be very selective about what we own with the group at 19x earnings.

Long: RH, KATE, PIR, NKE, RL

Short: FL, HIBB, KSS, TIF

UA - One week after it's investor day, UA is launching a new campaign behind two of its athletes. The campaign is call "Slay Your Next Giant" and includes young soccer star Memphis Depay, and Cameron Carter-Vickers.

WMT - Wal-Mart has acquired PunchTab, a 4 year old tech startup to help with customer engagement and targeted offers at Sam's Club. Terms are undisclosed. This is the 15th acquisition for WMT in 4 years, as they continue to add young tech talent.

(http://wwd.com/retail-news/mass/walmart-labs-acquires-punchtab-10236874/)

AMZN, ETSY - Amazon has quietly started a "Handmade" concept connecting makers of handcrafted goods with Amazon shoppers, which would be a direct competitor to ETSY. Though not officially launched, select sellers have started using it.

(http://www.ecommercebytes.com/cab/abn/y15/m09/i21/s02)

LULU - Chip Wilson's family's new Brand Kit and Ace is a year old. The company has 600 employees and plans to have 50 North American stores by mid 2016.

(http://www.bcbusiness.ca/retail/is-kit-and-ace-chip-wilsons-big-new-bet-really-a-tech-startup-0)

HBC, M - Saks announced a new Off 5th location in Woodland Hills, CA opening Aug 2016. While Bloomingdale's announced two new outlet stores in Philly and San Diego by November.

JCP - JC Penney promotes John Tighe to EVP and Chief Merchant, from SVP and senior general merchandise manager for men's, children's, footwear, handbags and intimate apparel.

(http://ir.jcpenney.com/phoenix.zhtml?c=70528&p=irol-newsCompanyArticle&ID=2089751)

TPX, CONN - New Tempur Sealy CEO Scott Thompson resigns as director of Conn’s. Corporate governance guidelines require directors to offer to resign when their employment status changes.

CRI - Carter's amends revolving credit facility to $500mm from $375mm.

(https://www.sec.gov/Archives/edgar/data/1060822/000119312515325541/d35273d8k.htm)