This call is likely going to be six months early, but now is the time to go LONG DFRG.

The LONG DFRG thesis is centered on management doing the right thing. Management needs to right size the company with significant changes to its growth/operating strategy that will significantly improve profitability. This will take time but it’s a critical step to building a stronger company.

The plan that the DFRG management team needs to execute has been done many times before by some of the industry’s largest and most successful companies. The following is our theory about the operational cycle that many companies in the restaurant industry tend to go through. Typically, when a concept gets in trouble, the management team’s decision-making process has followed a certain pattern. A company’s stock becomes a buy when the cycle is complete.

THE SYMPTOM - OVERCONFIDENCE AND IRRATIONAL EXPECTATIONS— A concept loses its operational integrity when unit growth exceeds the company’s capacity to manage that growth. Also, a concept can lose its value proposition when management raises prices too aggressively or lowers the quality of the food, leading to a decline in customer counts.

Most management teams are unwilling to acknowledge the issues and try to grow through the mistakes, which usually make the issues more difficult and costly to fix. The grieving process looks something like this:

STAGE 1 – SETTING THE GROUND WORK — In an effort to meet aggressive unit growth targets, management makes bad real estate decisions. Management knows from the beginning that any given sight is questionable, but opens it regardless. From the store opening, it takes about 6-12 months (depending on the size of the company) for the street to see it in the numbers. For more mature companies, that raise prices aggressively, it is a two years process before consumers catch on and begin to frequent the concept less often. Traffic begins to decline and management usually begins to blame the weather or another external event.

At this stage the best SHORT stories are created!

STAGE 2 – THE DENIAL — Depending on the situation, denial can take many forms. Unfortunately, bad real estate site selection is hard to explain away, but it usually comes in the form of lack of brand awareness. In an effort to avoid the inevitable and appease the street, management begins to accelerate growth through the form of new unit acceleration in core markets. More mature companies will look to the acquisition of new brands as a way of maintaining a growth story. Unfortunately, the core business continues to deteriorate alongside a decline in ROIIC (return on incremental invested capital).

STAGE 3 – THE PANIC — As the numbers become self-evident, the fast money crowd begins to circle, pushing management to disclose more details. In the beginning, the sell-side takes it easy on management, allowing for any initial strategy to play out. Depending on how bad things look, management talks about a number of changes to operations and may respond by slowing new unit growth, although often not by enough. The core business continues to decline, as senior management begins to replace the operating team. Simultaneously, management concludes that the advertising agency is not creative enough and the search for a new agency begins.

STAGE 4 – DEPRESSION — Now it really gets ugly. At this point one of two things can happen. First, management can reduce labor at underperforming units to improve profitability, or second, management sacrifices margins to increase customer counts by implementing a deep discounting strategy. It then becomes clear that major changes need to be made across the enterprise.

STAGE 5 – THE UPWARD TURN AND HOPE — Management decides to close stores, stop growth and or stops discounting to improve profitability. The next move is to attack the middle of the P&L to improve profitability.

At this stage the stock becomes washed out and the sell-side has abandoned the company. It also becomes very hard for the buy-side to pull the trigger and buy the stock. At this stage I like to go LONG!

Having acknowledged the need to close stores and slow the growth rate of The Grille, we view DFRG as emerging from depression. To that end, DFRG has announced the first steps to improving the broken company:

- Closing unprofitable stores

- Slowing unit growth

- Increase focus on existing assets

What we are missing from the DFRG story are the details behind what level of profitability (the improvement in EBITDA) will be coming from the store closings. Despite management acknowledging the issues, the stock has been beaten to a pulp, down ~30% over the last three months. We are starting to feel that at 6x EV / NTM EBITDA all the bad news has been priced into the name.

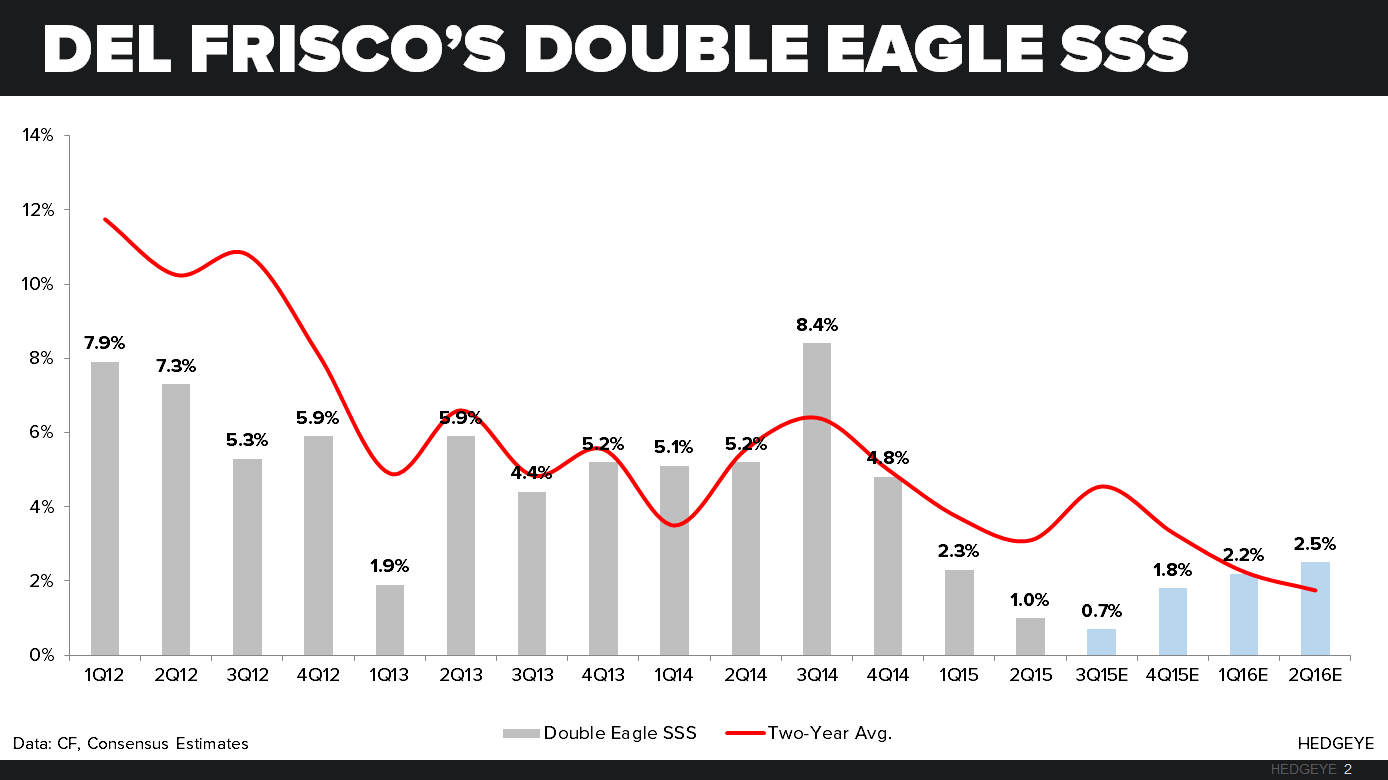

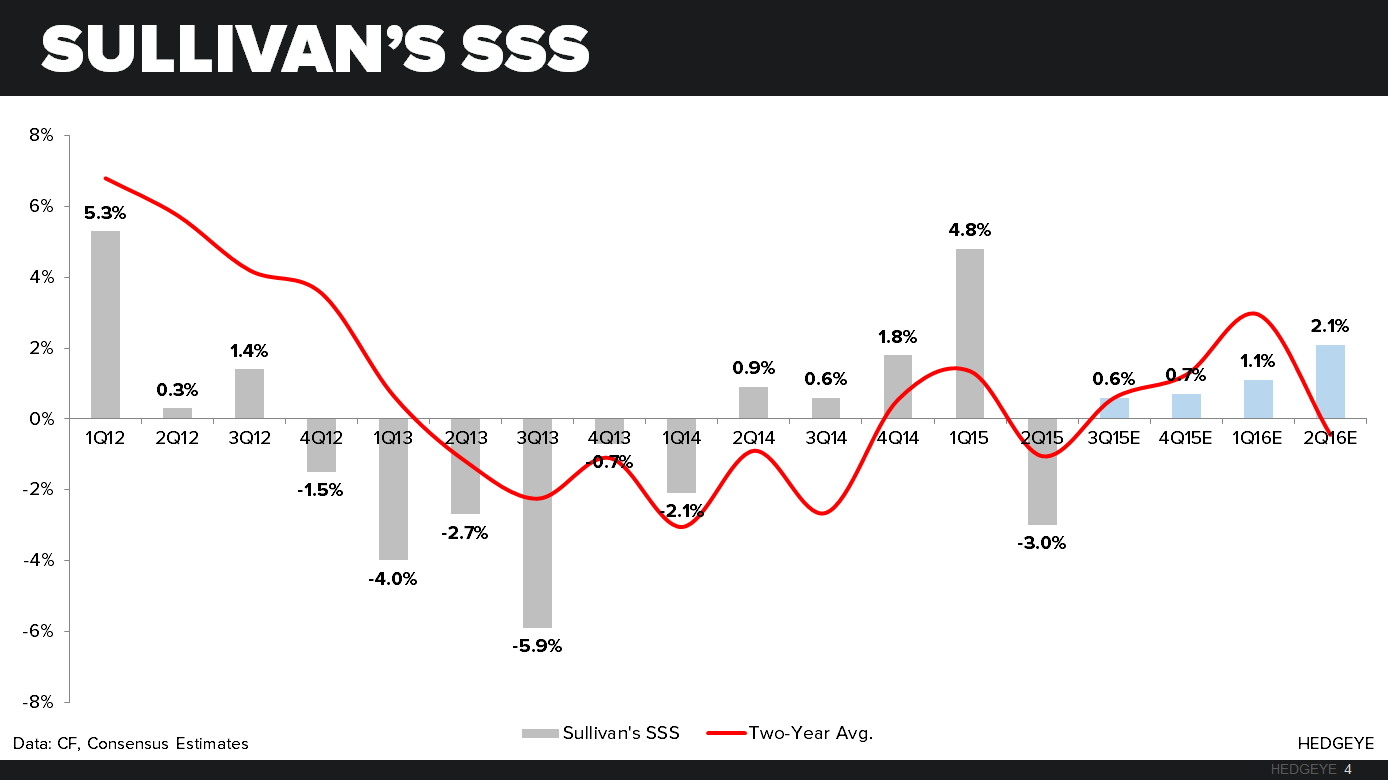

Unfortunately, the company’s strongest brand, The Double Eagle, is seeing slowing sales trends due to market volatility and the associated decline in banquet business. As for the changes within their control, this is exactly what we want them to be doing, and we believe that they will get the Grille concept running smoothly.

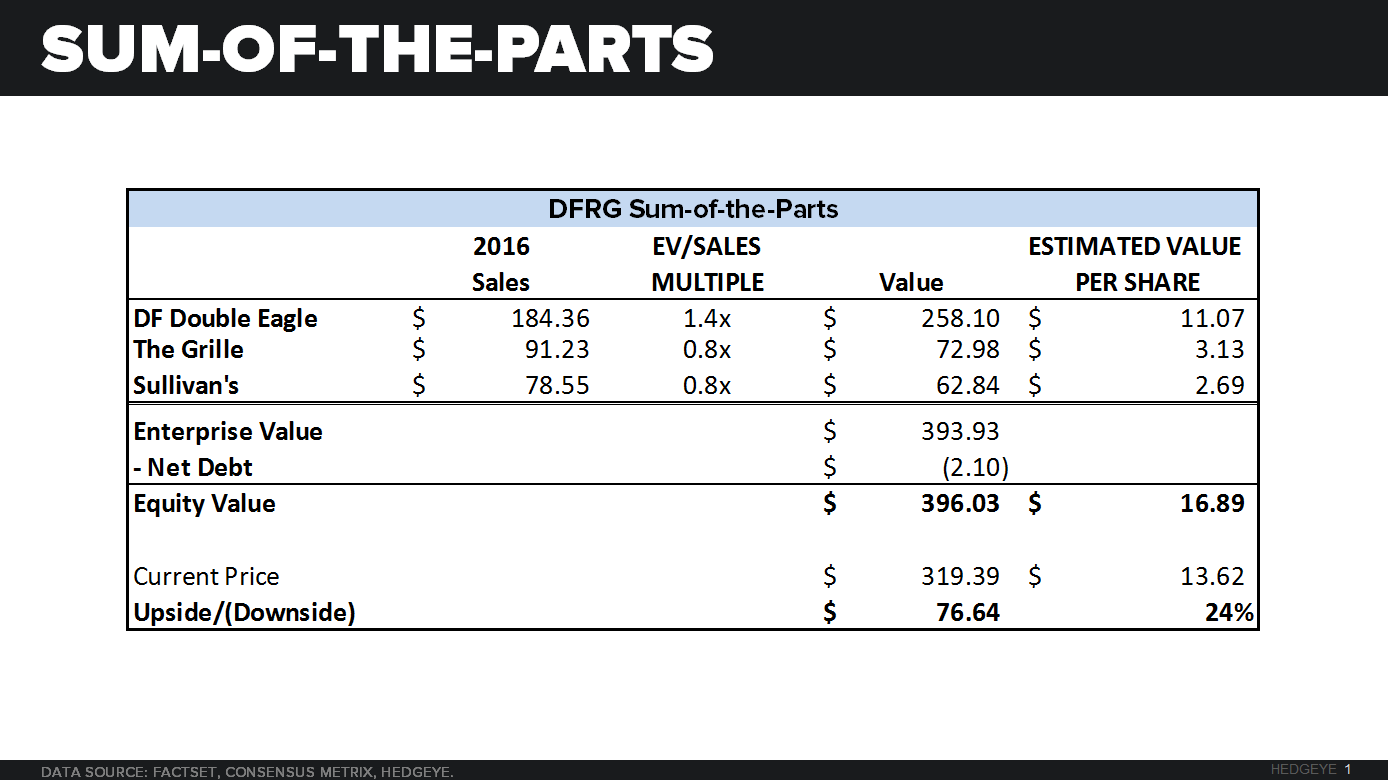

From a sum-of-the-parts analysis the stock is significantly undervalued (see table below) as it probably should be given the current fundamentals. That being said, six months from now, hope will turn into optimism and the stock will be a lot higher!

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst