"[I’m] not loving it …I have problems with earnings growth [and] problems with multiples, …So I can't really call myself a bull "

- David Tepper, 9/10/15

A little bit of a #TepperTantrum yesterday from the Appaloosa Management founder and stalwart bull.

Advocating higher cash allocations, highlighting higher volatility and increasingly challenged corporate fundamentals, voicing concerns over current multiples and pervasive over-optimism around forward growth prospects.

Sound familiar?

Tepper’s fundamental and valuation concerns are really just manifestations of our current late-cycle reality and a recapitulation of our 2Q15 #LateCycle Macro Theme.

We don’t always agree with Tepper but, when we do, we like to do it 3-months and 150 SPX handles ago.

(The prescient cartoon above was published one year ago this month.)

Back to the Global Macro Grind…

Since 2 & 20 sourced soundbites still grab more headlines than Hedgeye’s #BlueCollarMacro mouthpiece, Tepper’s comments yesterday offer a worthwhile opportunity to review some of the fundamental market data and contextualize the current expansion within the historical late-cycle experience.

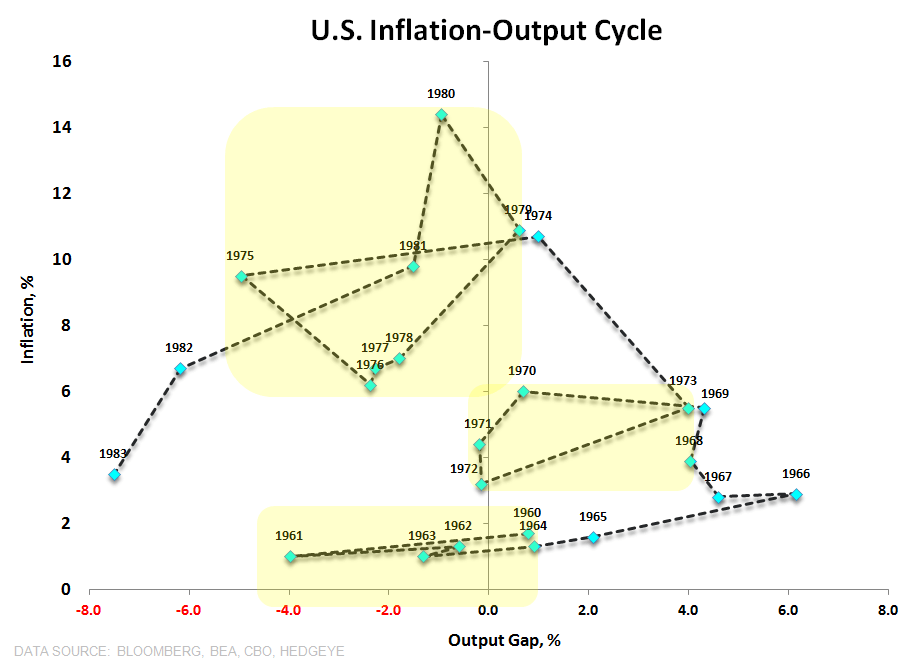

First, The Cycle: Let’s take a quick step back to re-remember the archetypical economic cycle – from the perspective of the current cadre of policy makers.

Macro cycles, left to themselves, follow a pattern that largely resembles the circular, counter-clockwise flow captured in the inflation-output loop depicted in the 1st Chart of the Day below.

The conventional view is that the level of output drives inflation which, in turn, drives the policy response. These output-inflation cycles were the prevailing macro reality when the present global policy making oligopoly was coming of age and conventional monetary policy is designed to function within the context of this naturally evolving cycle.

The broader goal of current policy efforts is to both jump-start and subsequently smooth such a cycle in the face of persistent cyclical challenges and glacial secular shiftings.

Policy = Lost in Transmission

The Phillips Curve and the aforementioned output-inflation cycle on which conventional monetary policy is based has been so loose over the last 2 cycles (& the present one) as to be non-existent.

Meanwhile, the empirics on Janet’s hoped for policy flow through to Main Street remain dismal. Labor’s Share of National Income – which, historically, only rises at the tail end of an expansion and after growth and profits have been strong for a protracted period – remains at a multi-decade trough. Even if we follow the pattern of gains in the late innings of expansion it won’t close the gap – and, if it does, it will likely come alongside a step function move lower in corporate profitability and EPS growth.

The other side of rising inequality and top-heavy income distributions is lower highs and lower lows for labor income.

Valuation = An Anchor, Not a catalyst

Valuation is not a catalyst and from a short-to-medium term risk management perspective, it sits somewhere near the middle-bottom of our consideration hierarchy.

That said, over the longer-term, valuation certainly matters in anchoring return expectations and we don’t discount it as a factor completely, particularly as it moves towards extremes in either direction. Underneath the technicals, acute policy catalysts, and reflexivity that drives immediate and intermediate term price trends sits the steady drumbeat of fundamentals and an accordion-like tether to ‘fair value’.

Because investor’s maintain varying proclivities for particular multiples and conceptual valuation frameworks, one measure we track is a valuation composite which represents an equal weighted composite of three of the most widely used conventional valuation metrics: Shiller PE, SPX Market Cap-to-GDP and Tobin’s Q.

We review each in turn below but the broader conclusion is straightforward: current valuations are richer than at any point except the nose-bleed tech bubble highs. As we’ve highlighted, lower neutral policy rates and perma central bank interventionism may indeed be supportive of higher mean valuations but that only modestly dilutes the conclusion. When valuations are in the top decile of LT historical averages, subsequent returns over medium and longer-term periods are just not that compelling.

- Shiller PE: Inclusive of the hundred’s of billions of market cap lost in the recent correction, the Shiller PE remains above 24x and sits just south of the top decile of its historical range. Mapping the Shiller PE by decile vs subsequent market performance suggests return expectations should move systematically lower alongside incremental increases in valuation. Historically, 1Y and 3Y returns progressively decline for each decile change in the Shiller PE.

- Tobin’s Q: Longer-term valuation arguments center on the premise that returns on capital should equalize to cost of capital and market values should normalize to economic value. Tobin’s Q ratio is not a measure we use to tactically manage risk, but we can appreciate the intuition underneath its application – why buy an asset when you can re-create it for less and compete away existing, excess profit. Historically, at extremes, it has served as a solid lead signal for subsequent market performance. Currently, the q-ratio sits at ~1.06 and greater than 1.3 standard deviations above the long-term mean value – a level that has generally not been a harbinger of positive forward returns historically.

- S&P 500 Market Cap-to-GDP: Assuming the collective output of SPX constituents credibly reflects aggregate national production (or serves as a credible proxy for it), the Market Capitalization-to-GDP ratio effectively represents a price-to-sales multiple for the economy. At current levels we are well above both the LT average and the 2007 highs.

The Chart of the Day below shows the valuation composite using the most recent data for the respective metrics.

PEAK PROFITABILITY

Earnings, Corporate Margins and collective SPX profitability all peak mid-to-late-cycle and the last few quarters of data suggest we’re probably past peak in the current cycle (ping sales@hedgeye if you’d like to review our 2Q/3Q Macro Themes decks).

In a low-to-no growth environment where the pie size stays the same, peak margins are good until they aren’t and are probably a symptom of policy ineffectiveness (in terms of flow thought to Main St.) more than not. Unless you think peak returns to capital provide a sustainable path to aggregate demand growth in the face of negative trend growth in real earnings, trough returns to labor, middling productivity growth and secularly depressed investment spending, then the mean reversion risk for operating margins remains asymmetrically to the downside.

- 2Q15: As Keith highlighted yesterday, with 2Q earning largely rearview for SPX constituents, the final score shows revenues and earnings down -3.5% and -2.2% year-over-year, respectively. Yes, the commodity rout was an outsized impact to energy/industrial’s profitability and this year’s collapse becomes next year’s comp but still, negative top & bottom line growth is not the stuff escape velocity, private-sector handoffs are made of or multi-year tightening cycles anchored on.

Our immediate-term risk Global Macro Risk Ranges (with our intermediate-term TREND call in brackets)

UST 10yr Yield 2.12-2.24% (bearish)

SPX 1 (bearish)

VIX 21.70-30.93 (bullish)

Oil (WTI) 42.43-48.17 (bearish)

Gold 1101-1147 (bullish)

Turning away from the market myopia for a moment before closing.

Today is Patriot Day. To those who serve(d) in the military and those, more broadly, who go underpaid and underappreciated in service of our greater good, your selflessness does not go unnoticed and your sacrifice will not be forgotten. We are sincerely grateful for your effort.

To hope & humanism, doing the right thing when no one is looking and blue collar alpha,

Christian B. Drake

U.S. Macro Analyst