Long LNCE – 8/19/15 Call Replay and Slides

Link to Audio Replay

Link to Video Replay

Link to Slide Deck

(If you have any issues accessing the replay, please email )

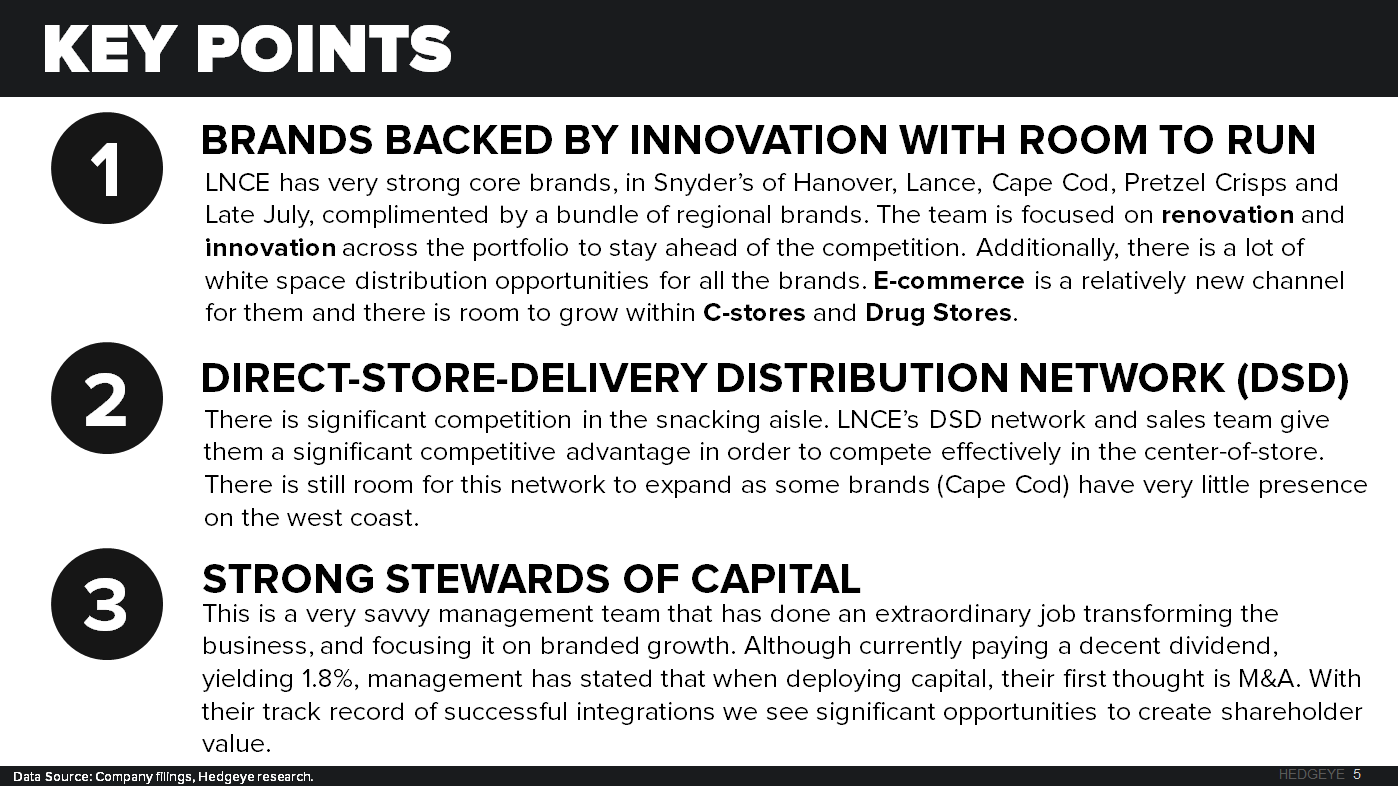

Our LONG thesis on LNCE is focused on three key points:

LNCE has repositioned their portfolio since the merger in 2010. They are now fully focused on branded products.

One of their biggest advantages is their Direct-Store-Delivery Distribution System (DSD). DSD is a big revenue driver, representing roughly 71% of sales.

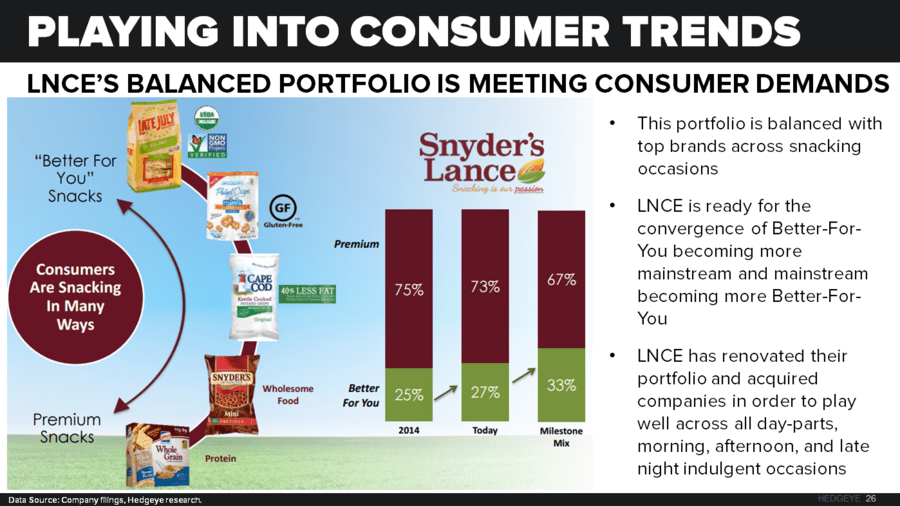

LNCE has products for every occasion, from better-for-you to indulgent and everything in between.

Snyder’s-Lance has gone through a period of broad based investments in infrastructure; they are now past this and shifting spending towards growing the top line.

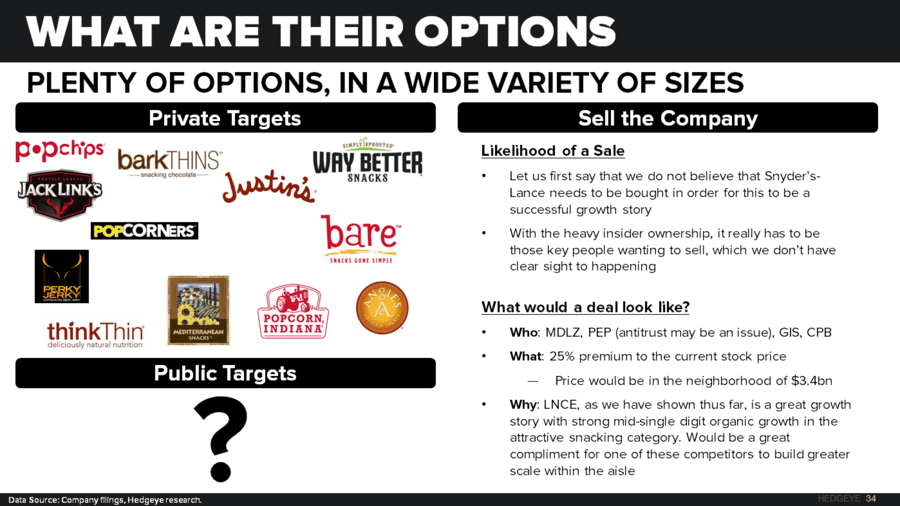

LNCE has plenty of dry powder to do a deal, and they are looking.

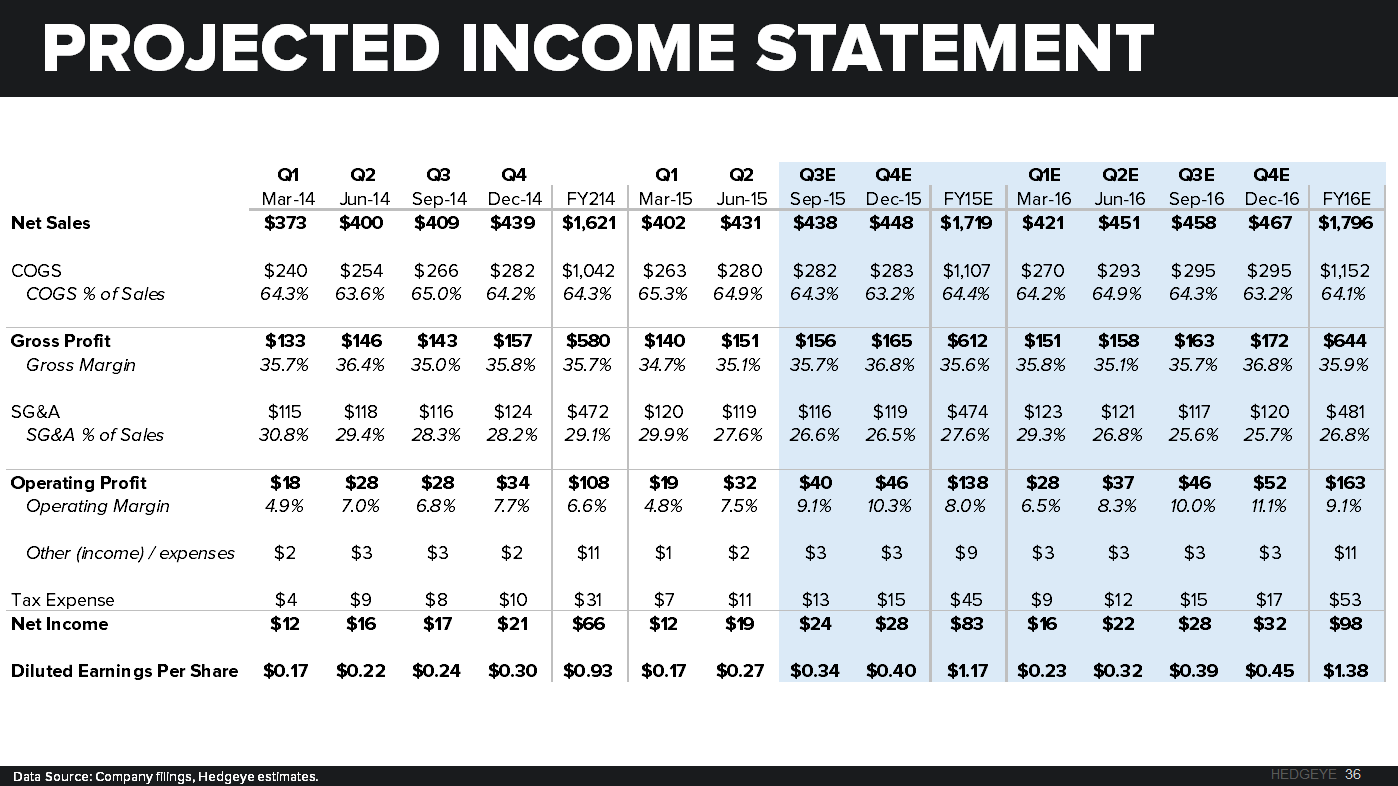

Our projected top line growth yields strong results.

Margins are going to expand as LNCE leverages their newly remodeled system.

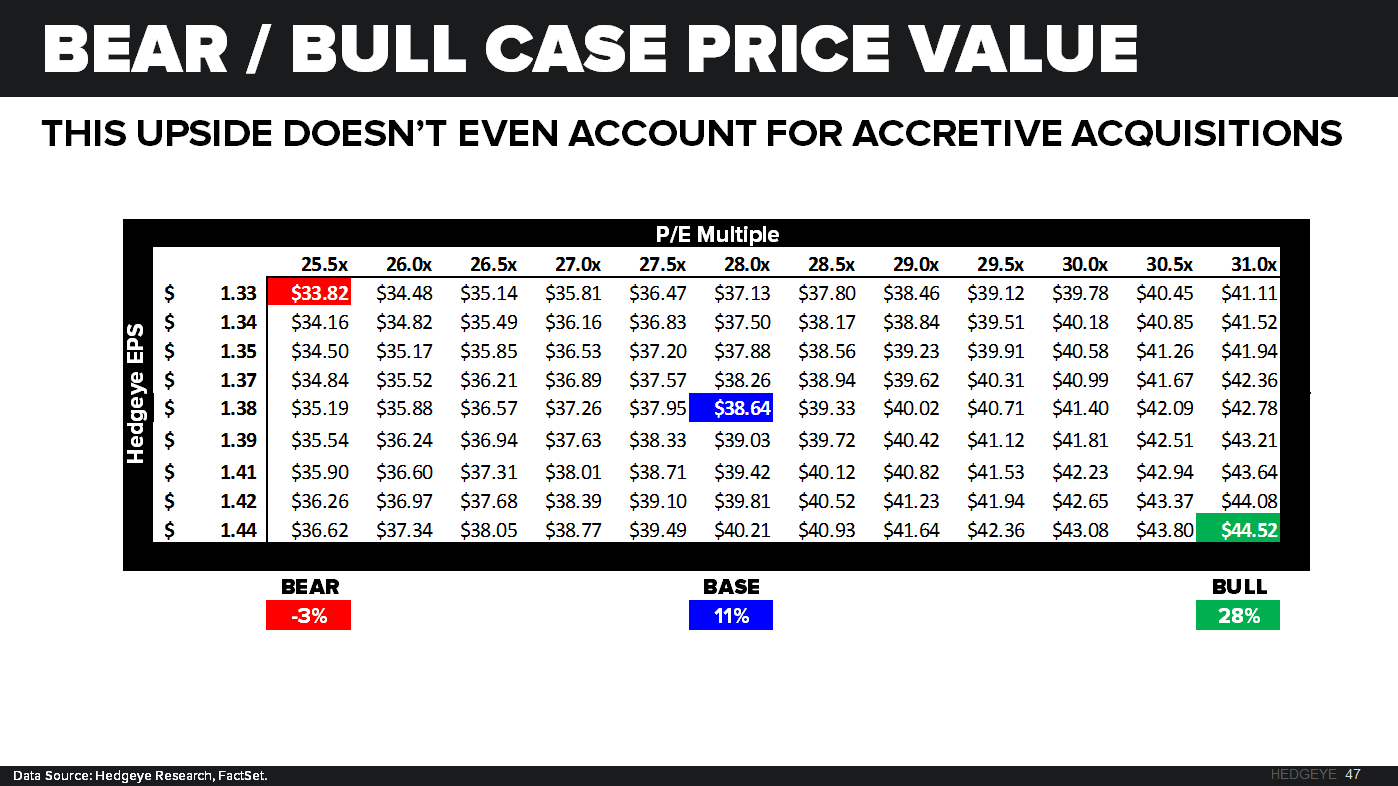

We see a solid 25%+ upside to the name without accounting for accretive acquisitions.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst