Conclusion: The reason we turned bullish on DKS earlier this year came through in these numbers. No major changes to our model, or our thesis. While the model has its challenges long term, it has more EPS power to recoup near-term than people think. When $4+ EPS becomes a reality, this stock should be in the $60s, at least.

What We Liked:

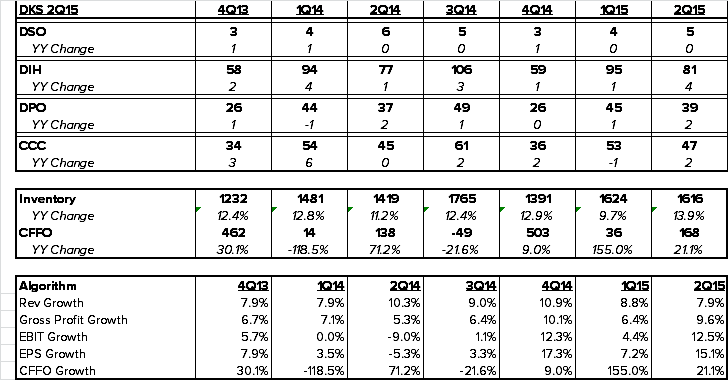

- Growth Algorithm: This is the first quarter in six where growth in revenue<gross profit<EBIT<EPS<Cash Flow.

- The company beat without showing meaningful strength in the top line – showing the leverage in the model as the business recovers.

- Gross margin +47 bps despite e-comm (dilutive) accounting for all the growth. DKS also likely starting to recoup margin lost last year due to golf/hunting categories. We estimate about 160bps hit to gross margin from these categories in 2014, almost all of which is recoverable.

What We Disliked:

- Store comp improved sequentially, but it was still negative which now makes 4 quarters in a row that the stores comped negative, and 9 out of the last 11.

- Implied New Store Productivity came in at 83%, a good number compared to most retailers but was the worst number at DKS since 2Q 2010. We would note that DKS opened 6 new locations in the south from Texas to Virginia during the quarter, including a dual format Dick's/Field & Stream in Hibbett's back yard Mobile, Alabama.

- Inventory up 14% with sales up 8%, the worst spread in 7 quarters. Management noting earlier receipts of BTS product and planned support of outdoor business as the reason for the increase – but that’s what they all say.

Change In Our View:

- More Bullish: We’ve been saying for four months that estimates are too low. This growth algorithm on trough-ish sales sets DKS up nicely when the business turns – which we think it will.

- No change to our model, which is already ~10% above consensus.

- Within 6 months, it’s more likely than not that the dialogue will evolve into the potential for DKS to hit ‘17E EPS a year early.