“Many men go fishing all of their lives without knowing it’s not the fish they are after.”

-Henry David Thoreau

In case any of you emailed me and got a “Gone Fishing” auto-reply, I checked out on Tuesday night of last week to go on what has become an annual Hedgeye Fishing Trip to my homeland on Lake Nipigon. It was epic.

Got volume? Often called the “Sixth Great Lake”, Lake Nipigon is massive. It has a surface area of 1,872 square miles and average and max depths of 180 and 541 feet, respectively (Wikipedia).

So now I’ll try to make the literary-transition from a place where there were no other humans to where there was no volume. On Friday, Total US Equity Market Volume was down -22% and -33% vs. its 1-month and 1-year averages. Wow.

Back to the Global Macro Grind…

Buying markets on slow-to-no-volume UP days is not what I do. I like to buy/cover on capitulation (low-end of my immediate-term risk range) DOWN days. For many things High Beta #Deflation, that day was Wednesday of last week.

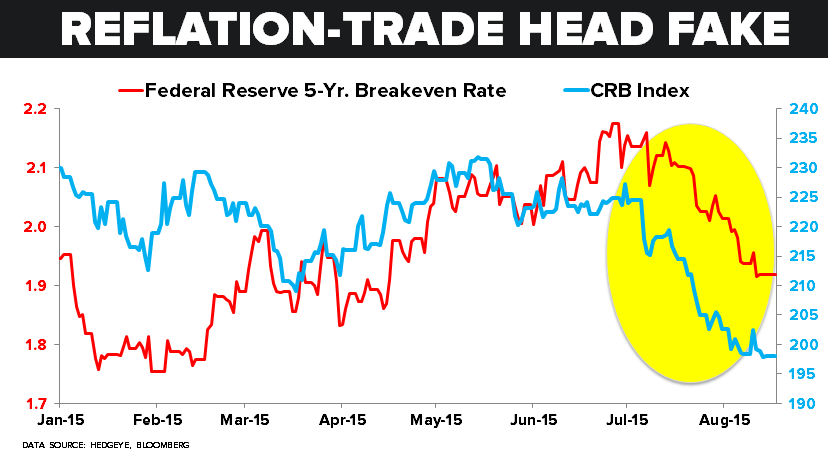

By week’s end, what the growth bulls call “reflation” finally had an up week. Not up huge, but up. And that’s mainly because the US Dollar ended up closing down -1% (US Dollar Index) on the week.

If you look at the week-over-week moves in Global FX vs. the month-over-month, here’s what that added up to:

- US Dollar Index -1.0% on the wk = -0.1% month-over-month

- Euro (vs. USD) +1.3% on the wk = +0.9% month-over-month

- Canadian Dollar +0.3% on the wk = -2.8% month-over-month

- Brazilian Real +0.7% on the wk = -9.9% month-over-month

- Russian Ruble -1.4% on the wk = -13.1% month-over-month

In other words, the closer a country’s leverage is to what’s been crashing for the last 1-3 months (commodity “reflation” expectations, Oil, etc.), the less of a “bounce” it got on Down Dollar last week.

Here’s how Commodities themselves did last week:

- CRB Commodities Index -0.2% on the wk = -9.8% month-over-month

- Oil (WTI) down another -4.1% on the wk = -21.3% month-over-month

- Gold finally had a real up wk of +1.9% = -3.6% month-over-month

- Silver was +2.5% on the wk = -0.8% month-over-month

- Copper was +0.6% on the wk = -7.5% month-over-month

Yes, it is rather damning for the USD to have one of its biggest down weeks of the summer and see both the commodities index and oil continue to crash/deflate (for those who remain long of them, that is).

That said, if you pivoted, hard (on Wednesday), and bought/covered anything US Equities that was in the midst of a -7% (Russell 2000) to -15% (Energy Stocks) draw-down, you crushed it last week.

Even though the world couldn’t find it in them to buy Brazilian Stocks (down another -2.1% on the wk, and down -10.7% in the last month), hedge funds that were short US Energy and Utility stocks evidently had to buy/cover, for a trade:

- Energy Stocks (XLE) were +3.4% on the wk, but are still down -7.0% in the last month

- Utilities (XLU) were +2.7% on the wk, and continue to have a big relative move +6.1% in the last month

You see, the one thing that the Utilities (XLU) long position has going for it that “reflation” bulls don’t is called … drumroll … #Deflation! Yep, as both US growth and global inflation expectations fall, so do sovereign bond yields.

With the US 10yr Treasury Yield down another -3 basis points this morning, it’s almost down as much in the last month as inflation expectations themselves:

- US 10yr Treasury Yield -24 basis points in the last month to 2.17%

- US 5yr Break-Evens -33 basis points in the last month to 1.28%

And sure, there’s something like “82% of economists polled” at some Old Wall media outlet still looking for a “rate hike” in September. And maybe this un-elected Fed is under enough political pressure to do just that…

And… if they do that, as both growth and inflation expectations continue to map their respective cyclical and secular slow-downs, they run the very obvious risk of being THE catalyst for the next Dollar Up, #Deflation of levered asset prices.

I’m betting many at the Federal Reserve have spent their entire central-planning lives not knowing that they are the catalyst some of us are still looking for.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.12-2.24%

SPX 2071-2106

VIX 12.03-14.32

EUR/USD 1.08-1.11

Oil (WTI) 41.35-44.11

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer