KATE - Thoughts on 2Q Earnings Timing

There's a lot going on this morning, but from our perspective there is one thing that matters and that is the timing of the KATE 2Q release. The fact that KATE is stepping up ahead of KORS in the queue (it’s the first time KATE has reported ahead of KORS in a 2nd quarter since 2012 -- KORS 3rd quarter as a public company) tells us that the company wants to be out in front of KORS to delineate the good from the bad. That means that a) the company feels good about the trends in its business and b) management is playing a little bit of offense which is a step in the right direction for the IR department. Separating itself from the noise is a good move by the company and should give those pressing the short headed into the quarter due to concerns on the 'space' something to worry about.

SHOO - 2Q15 SIGMA

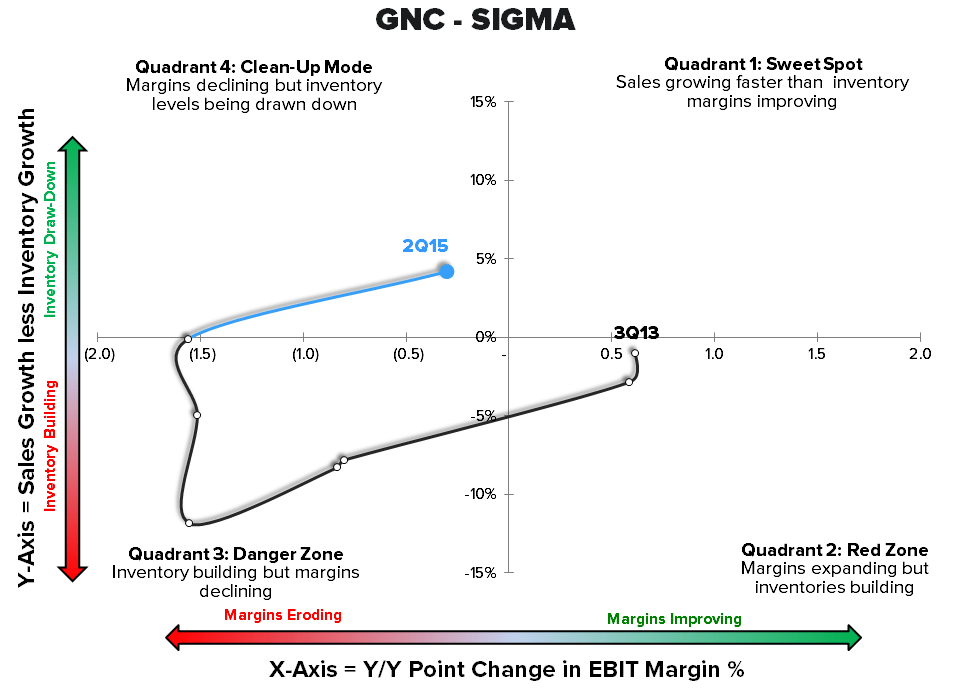

GNC - 2Q15 SIGMA

SKX - 2Q15 SIGMA

OTHER NEWS

Petco Said to Be Interviewing Banks for IPO Later This Year

Xcel Brands Raising More Money, Moving to Nasdaq

(http://wwd.com/business-news/financial/xcel-brands-nasdaq-offering-qvc-10193495/)

Joe’s in Breach of Forbearance Agreements

(http://wwd.com/business-news/financial/joes-jeans-breach-forebearance-10194581/)

TGT - Target doubles down on denim

(http://www.retailingtoday.com/article/target-doubles-down-denim)

Menswear retailer acquires all Jones New York stores in Canada; to expand