There will be a time Del Frisco’s Restaurant Group (DFRG) is a LONG, but for now we want to keep it on our bench as we wait for further evidence that management will make better capital allocation decisions.

At DFRG’s current market value, the Del Frisco Double Eagle segment accounts for ~74% of the market value. The implications are that The Grille and Sullivan’s are destroying shareholder value. Therefore, to create shareholder value from these levels significant changes must be made in the future capital deployment plans in those concepts. Management hinted on today’s earnings call that changes might be coming, but the stock reflects zero confidence that management will make the right decisions.

There things management can do to regain investor confidence:

- Stop new unit growth of “The Grille” in 2016

- Close all underperforming stores

- Demonstrate confidence in the trajectory of “The Grille’s” average unit volumes

Hoping that management will see the need to make these changes is not reason enough to go LONG DFRG.

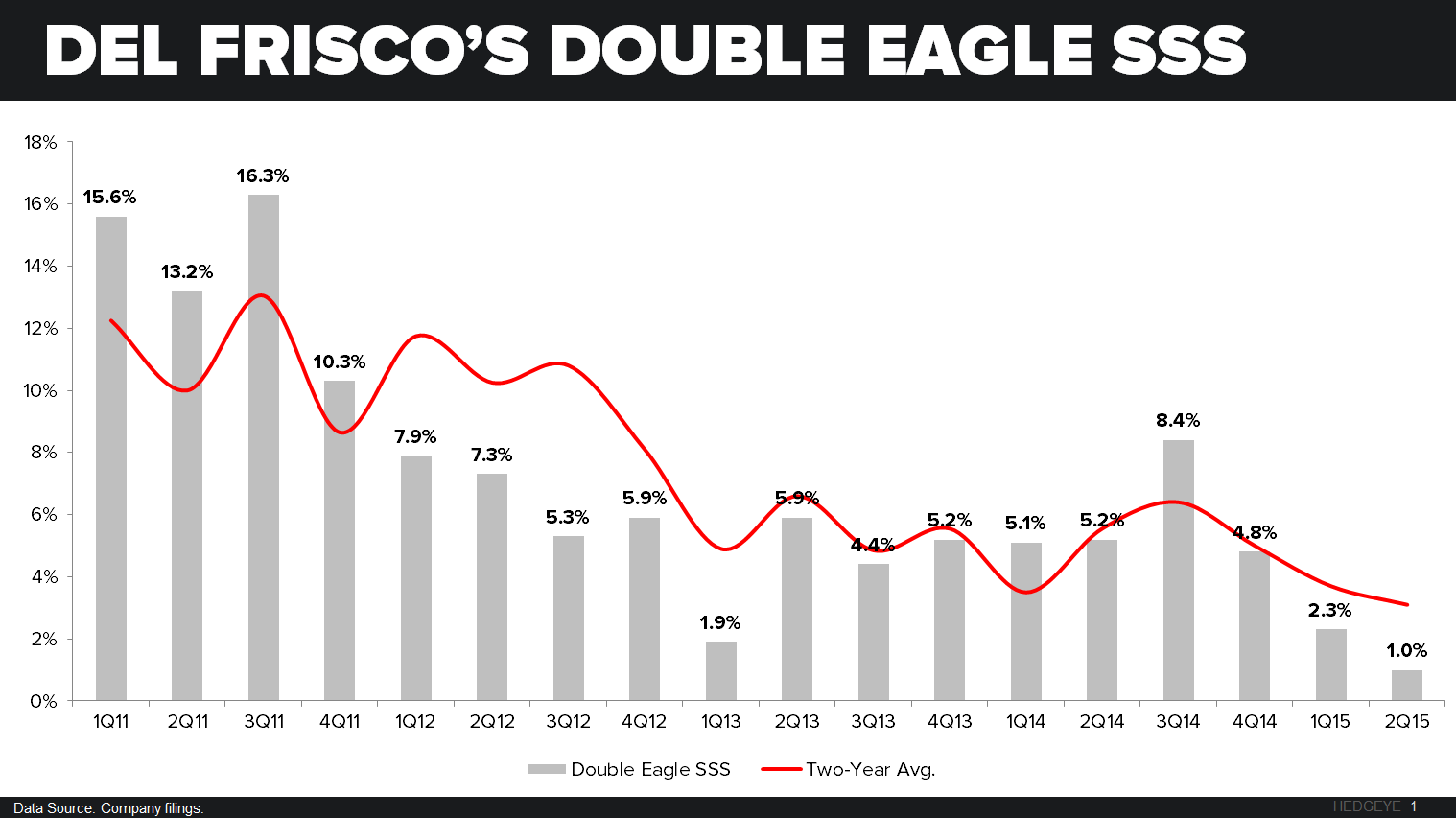

DFRG reported 2Q15 earnings this morning and it was overall a disappointing performance. Consolidated revenues increased 9.5% to $73.8 million but fell short of consensus estimates of $75.4 million. Comparable same-store sales (SSS) also missed across the board, Del Frisco’s Double Eagle reported +1.0% SSS versus consensus of +2.3%, showing a sequential slowdown over the last four quarters. Sullivan’s Steakhouse SSS decreased -3.0% versus a consensus estimate of +1.4%. And finally, Del Frisco’s Grille decreased -6.3% versus consensus estimates of -2.3%. Reported EPS was $0.16 versus consensus estimates of $0.19, further showing the current weakness across the business.

Del Frisco's Double Eagle 2-year trends are concerning, as they have decreased sequentially three quarters in a row.

Management’s reasons for poor performance were mostly blamed on external factors; weather affecting patio sales, Father’s Day shift, construction at NYC Double Eagle and conventions switching locations, among a few others. The Grille concept continues to struggle and we were hoping with the exit of Jeff Carcara, they would lessen their focus on the concept. For now their voiceover is the opposite, as they continue to sink capital into the Grille and Sullivan’s.

Recent restaurant development remains focused on the Del Frisco’s Grille concept, which just posted a -6.3% comps. At the end of the second quarter DFRG opened a Del Frisco's Grille in The Woodlands, Texas. In the third quarter, they have already opened a Del Frisco's Grille in Plano, Texas and will be opening a Del Frisco's Grille in Stamford, Connecticut and a Del Frisco's Double Eagle Steak House in Orlando, Florida. The remaining three Del Frisco's Grille locations in Little Rock, Arkansas; Hoboken, New Jersey; and Cherry Creek, Colorado will open in the fourth quarter. Management also closed the Sullivan's Steakhouse in Denver, Colorado during the second quarter upon its lease expiration.

Management adjusted the outlook for the remainder of 2015 down, annual comparable same-store sales are now expected to be 0.5% to 1.5% down from previous estimates of 2% to 3%. Annual adjusted EPS growth between 5% and 9% versus previously projected 15% to 18%.

We remain hopefully in the underlying business and the strength of the Double Eagle concept. Management needs to get smarter about capital spending, deploying it where the best return for shareholders is created. Until we hear something along these lines we are not comfortable jumping in on the long side.

The stock market reaction to the earnings is overwhelmingly negative as it is currently trading down ~16%. We will continue to monitor the name from the sidelines as we wait for the right entry point.