Q3 2015 FINANCIALS THEMES OVERVIEW:

#Exchanges&Volatility - Volatility looks poised to break substantially higher on European angst and summer's seasonality and the exchange group will be a beneficiary of this dynamic. That said, there is collateral damage from the energy patch bust. We see a great opportunity in being long CME on the underappreciated upside to its earnings trajectory, and being short Intercontinental Exchange (ICE).

#Canada'sBankBubble - Canada's property market is poised for a generational correction while the Banking system has its head in the sand. De minimis reserves, thin capital/high leverage and Energy/CRE exposure paint a very asymmetric picture of vulnerability, especially when juxtaposed against the mythology of Canadian banking strength.

#FinancialEngines & #Och Ziff - Two of our favorite SMID cap ideas on the long side. FNGN is a battleground small cap name that we think is misunderstood and undervalued. OZM has a secular tailwind from the rotational forces of pension assets into alternatives and is trading at its cheapest valuation in a decade.

- Relevant Companies/Tickers:

- Royal Bank of Canada (RY) (Market Cap $113 billion)

- Toronto-Dominion Bank (TD) (Market Cap $100 billion)

- CIBC (CM) (Market Cap $37 billion

- Home Capital Group (HCG) (Market Cap $3 billion)

- Genworth MI Canada (MIC) (Market Cap $3 billion)

- CME Group (CME) (Market Cap $32 billion)

- Intercontinental Exchange (Market Cap $26 billion)

- T. Rowe Price (Market Cap $22 billion)

- Och Ziff Capital Management (Market Cap $7 billion)

- Virtu Financial (Market Cap $3 billion)

- Financial Engines (Market Cap $2 billion)

CALL DETAILS:

US Toll Free:

Toll Free:

Confirmation Number: 13613076

Materials: HERE

Outlook Calendar Reminder: HERE

*********************************

Key Takeaway:

Last week's Greek woes remained contained to Greece as the broader EU complex appears de-coupled from what's happening within Greece. Not that it matters much in the short/intermediate term as the Eurozone has just agreed to a new €86 billion bailout package for Greece this morning.

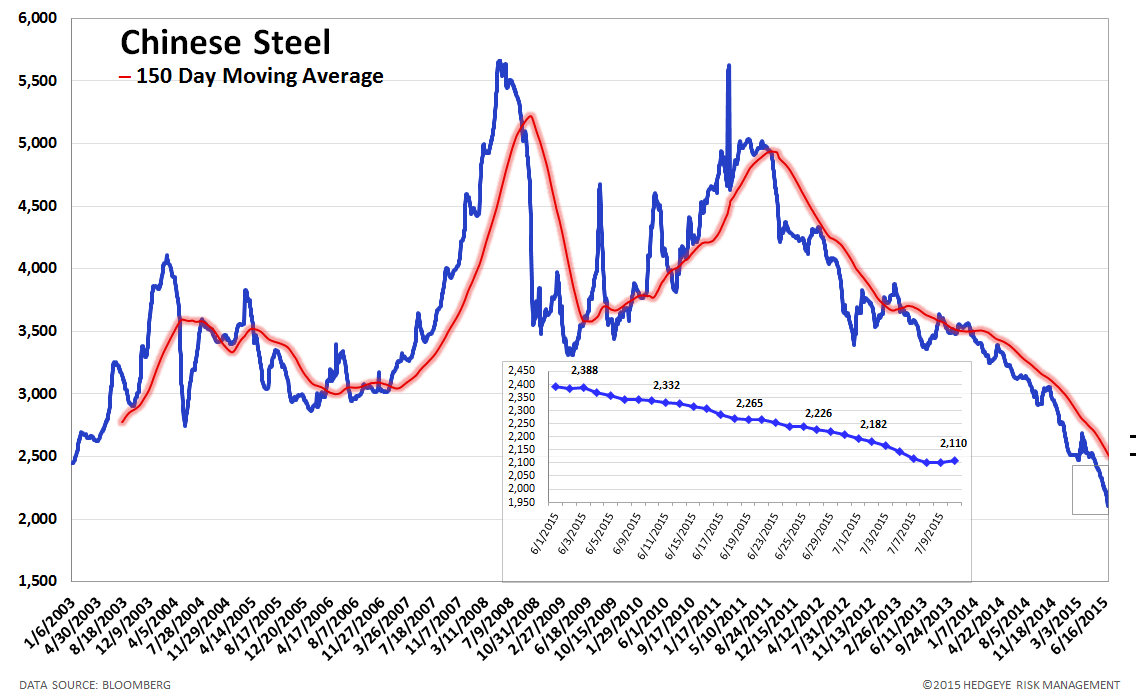

Meanwhile, China's steel prices continue to plumb new lows, shedding another 2.5% on the week. We use Chinese steel prices as our proxy for the real economy.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 5 of 12 improved / 2 out of 12 worsened / 5 of 12 unchanged

• Intermediate-term(WoW): Negative / 3 of 12 improved / 6 out of 12 worsened / 3 of 12 unchanged

• Long-term(WoW): Negative / 2 of 12 improved / 2 out of 12 worsened / 8 of 12 unchanged

1. U.S. Financial CDS - Swaps tightened for 17 out of 27 domestic financial institutions. Concluding a volatile week, the median week-over-week change in spreads ended at -1 bps.

Tightened the most WoW: HIG, AGO, AIG

Widened the most WoW: UNM, AON, MMC

Widened the least/ tightened the most WoW: CB, HIG, SLM

Widened the most MoM: MMC, MBI, ACE

2. European Financial CDS - Greek banks took it on the chin again last week as prospects for survival waned further. Outside of Greece, however, the broader European banking complex saw swaps tighten for the most part, indicating that contagion fears are nominal to non-existent at this point.

3. Asian Financial CDS - Two of three Chinese Bank saw CDS improve last week. Additionally, all Indian Bank CDS improved. However, Japanese Bank swaps widened.

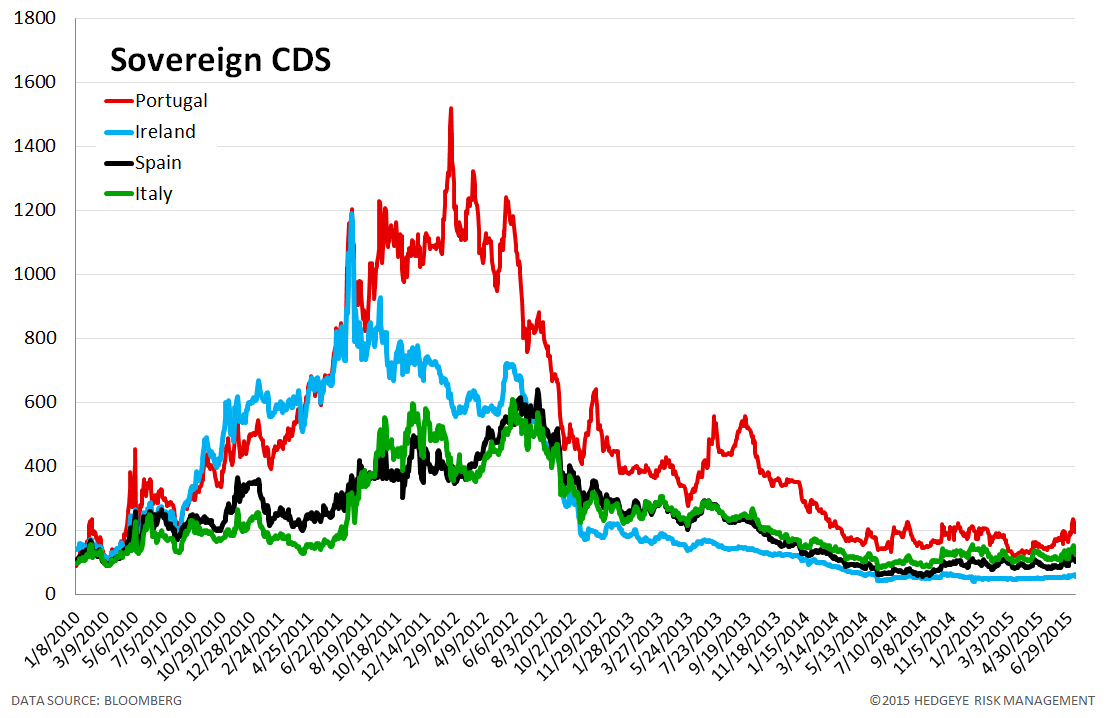

4. Sovereign CDS – Sovereign Swaps mostly tightened over last week. Italian sovereign swaps tightened the most, by -11 bps to 123.

5. Emerging Market Sovereign CDS – Emerging market swaps mostly tightened last week. Turkish and Indian swaps tightened the most, by -5 bps to 214 and -5 bps to 165 respectively.

6. High Yield (YTM) Monitor – High Yield rates rose 6 bps last week, ending the week at 6.68% versus 6.62% the prior week.

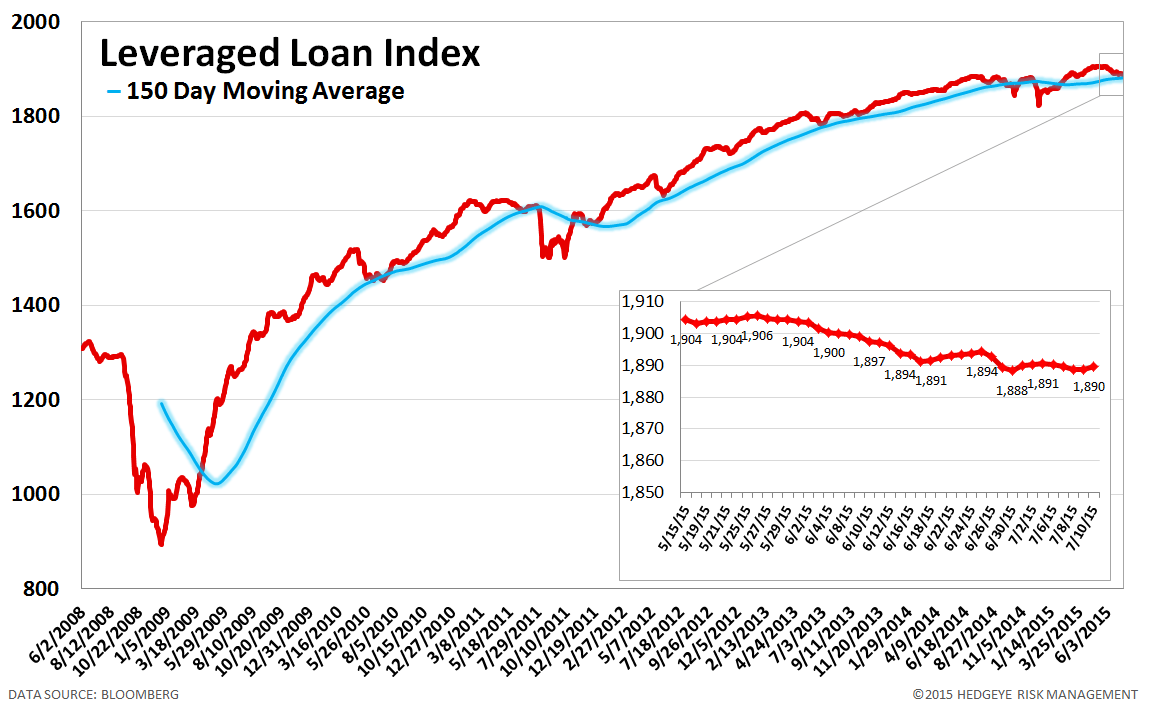

7. Leveraged Loan Index Monitor – The Leveraged Loan Index fell 1.0 points last week, ending at 1890.

8. TED Spread Monitor – The TED spread was unchanged last week at 28 bps.

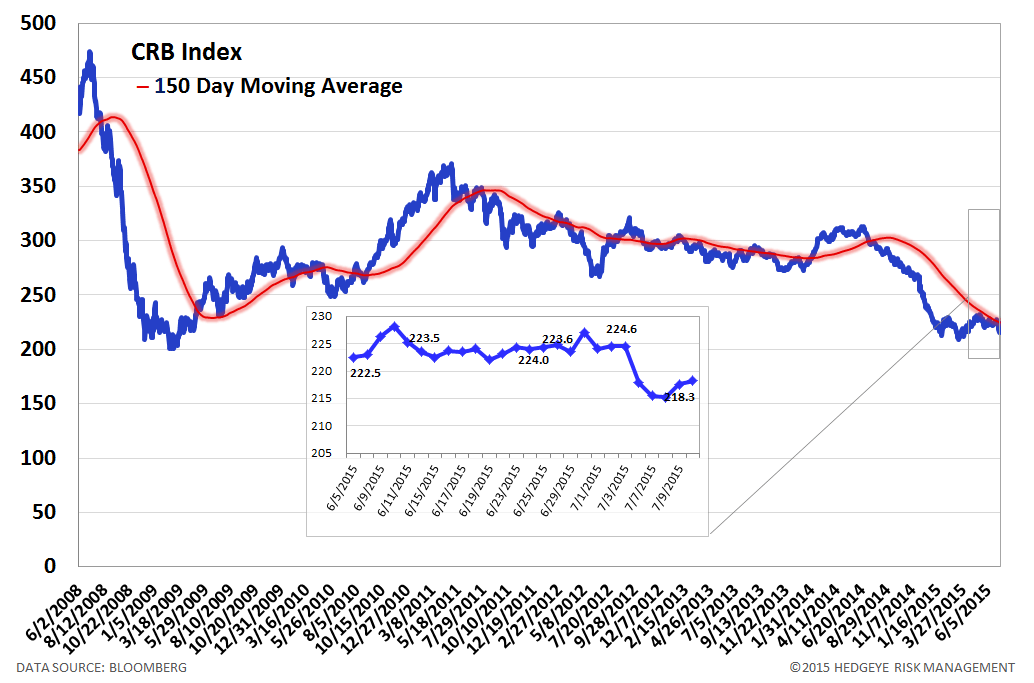

9. CRB Commodity Price Index – The CRB index fell -2.6%, ending the week at 218 versus 224 the prior week. As compared with the prior month, commodity prices have decreased -2.4%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 11 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 5 basis points last week, ending the week at 1.21% versus last week’s print of 1.16%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China fell 2.5% last week, or 55 yuan/ton, to 2110 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

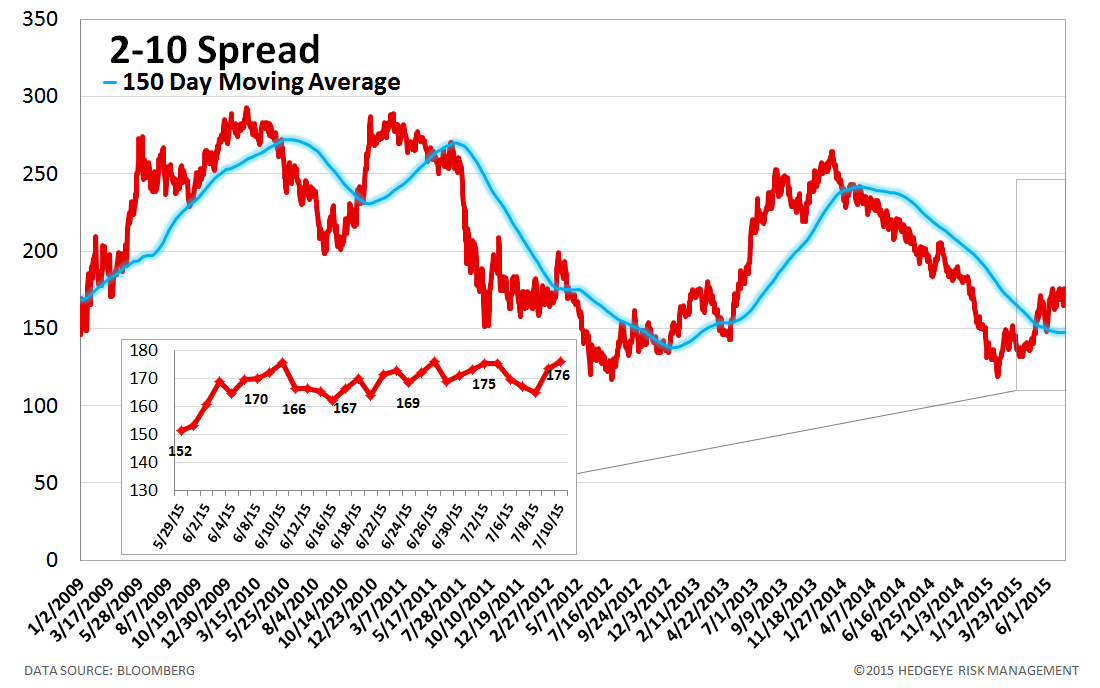

13. 2-10 Spread – Last week the 2-10 spread widened to 176 bps, 1 bps wider than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 0.9% upside to TRADE resistance and 2.6% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT