Hedgeye Retail Ideas List

UA - Not A Winning 'Streak', Just #winning. Again, and Again. Now Needs to Translate it to Dollars.

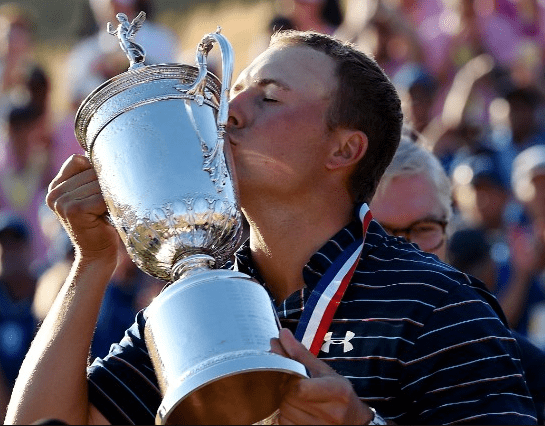

Just when you thought Under Armour's 2015 couldn’t get any better, in the same week that Stephen Curry wins an NBA title, Jordan Spieth wins the US Open. Spieth's victory marks the first time a player has won the first two majors of the year since Tiger in 2002 and the youngest to win the US Open since Bobby Jones 1923.

Under Armour presciently signed Spieth to a 10 year contract in January, and so far the return -- at least as measured by share of voice -- has been immense. Jordan put the UA logo on prime time TV throughout the weekend and even managed to mention Under Armour in an interview immediately following the victory when asked if he had a 5th outfit for a playoff.

The challenge for UnderArmour at this point is whether the company can monetize these moments when its athletes are in the limelight. Historically, that's where every single brand has fallen down when playing the athlete endorsement game. It's not enough for the athlete to play, win, and advertise the logo all along the way. The company needs to use events like this to establish emotional connections between the Brand and the Consumer.

With Nike, we'd argue that its competitive edge in endorsements is not just a function of its huge wallet, but rather its ability to drive this emotional connection -- which clearly drives loyalty and increased sales. In fact, Nike has been known to do this even when it's athletes don't win -- or flat-out lose. This is the one area where we're waiting to see UA shine. If it succeeds in this regard, then 2H and 2016 expectations will prove far too conservative for UA.

OTHER NEWS

LB - L Brands Authorizes $250 Million Repurchase Program

(http://phx.corporate-ir.net/phoenix.zhtml?c=94854&p=irol-newsArticle&ID=2060879)

AMZN - Amazon to open FC in Target's backyard

(http://www.retailingtoday.com/article/amazon-open-fc-targets-backyard)

Retailers Cut Jobs as Pressures Mount

(http://wwd.com/retail-news/financial/layoffs-job-cuts-retail-10159174/)

Anna's Linens begins liquidation sales

(http://www.retailingtoday.com/article/annas-linens-begins-liquidation-sales)

Barneys enables Instagram shopping

(http://www.chainstoreage.com/article/barneys-enables-instagram-shopping)