This note was originally published at 8am on June 08, 2015 for Hedgeye subscribers.

“Education is what happens after one has forgotten what one has learned in school.”

-Albert Einstein

After rates rise, we learn that consensus hasn’t learned a whole heck of a lot about cyclical investing. It’s too bad they don’t teach that in school.

I don’t know about you, but I got schooled last week. Both stocks and bonds were down. With German Bund Yields doubling in 3-days, then US yields rallying on another “good” jobs report, bond yields ripped.

No, I’m not capitulating on the Slower-For-Longer (lower rates) cycle call this morning. If US growth was accelerating, I would. On jobs, #history students know that Non-Farm Payrolls rising is what happens AFTER the US economic cycle has already peaked.

*Click here to watch The Macro Show at 8:30am ET with special guest, U.S. macro analyst Christian Drake.

Back to the Global Macro Grind…

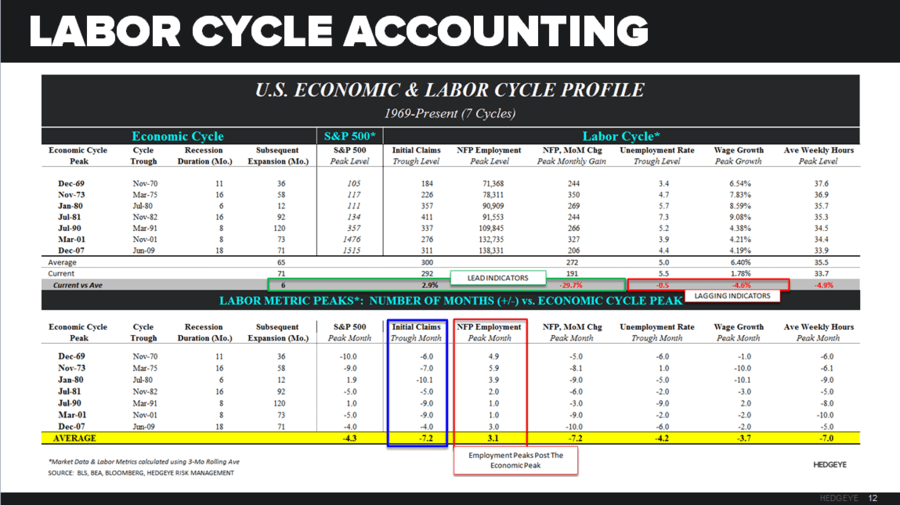

As you can see in today’s Chart of The Day (it’s actually a rock solid table of historical labor cycle data), these are the facts about US labor metrics. I’d like you to zero in on the number of NFP months (+/-) vs. economic cycle peaks:

- DEC 1969 (economic cycle peak) = +4.9 months (# of months after DEC 69’ when NFP peaked)

- NOV 1973 = +5.9 months

- JAN 1980 = +3.9 months

- JUL 1981 = +2.0 months

- JUL 1990 = +1.0 months

- MAR 2001 = +1.0 months

- DEC 2007 = +3.0 months

Yeah, I know – the Fed and its Old Wall research departments are all over it, reminding you about that this morning. But, unless it’s “different this time”, US non-farm payrolls are in the #process of peaking. And I’m not a big fan of capitulating at peaks.

Zooming into this #LateCycle (2015), here’s what the rate-of-change in Total Non-Farm Payrolls (NFP) has looked for the last year:

- JUL 2014 = +2.01% year-over-year growth (y/y)

- OCT 2014 = 2.04% y/y

- NOV 2014 = 2.11% y/y

- ***FEB 2015 = 2.34% y/y

- APR 2015 = 2.18% y/y

- MAY 2015 = 2.21% y/y

And if you want to data mine, Total Private Payrolls (PP) peaked in rate-of-change terms in FEB 2015 as well = 2.71% (vs. 2.53% in Friday’s jobs report).

In other words:

A) The US economic cycle (see recent GDP report for details and/or April/May economic data) already peaked

B) The latest of #LateCycle indicators (employment) is in the process of peaking, as it always does

“So”, Janet, what do you say you raise rates into that?

You know, with the almighty Dow down for 3 straight weeks (-1.6% in the last month) – why not give it a try, just to see what happens? Not that you care about the stock market, or any other asset bubble that your boy Bernanke perpetuated… give it a whirl!

While this note contextualizes the latest GROWTH cycle component of the Fed’s decision on June 17th, here’s a friendly reminder on the other big economic factor that some say bond yields are rallying on – INFLATION:

- CRB Commodities Index was down another -0.3% last wk and is still in crash mode at -26.9% year-over-year

- Oil (WTI) remained in TAIL risk mode (TAIL resistance = $67.92/barrel) -2.3% last wk and -36.7% year-over-year

Not to be confused with the counter-TREND bounce off the January 2015 #deflation scare lows (when the Long Bond tested all-time highs), year-over-year inflation’s TREND remains as bearish as the rate of change in US growth is.

I’m thinking that if the Fed raises rates in this environment, equity volatility (VIX) is going to start looking like FX and Fixed Income volatility (venti!). Don’t forget that horse has already left the barn (VIX +21.7% year-over-year) too.

If I’m wrong on US Treasury Yields from here, the re-education of perma stock market bulls is officially back-to-school.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.02-2.44% (bearish)

SPX 2079-2109 (neutral)

RUT 1239-1267 (neutral)

Nikkei 20371-20679 (bullish)

VIX 13.04-14.99 (bullish)

USD 95.01-98.05 (neutral)

EUR/USD 1.08-1.14 (bearish)

YEN 123.76-125.81 (bearish)

Oil (WTI) 56.77-61.30 (bullish)

Natural Gas 2.52-2.75 (bearish)

Gold 1170-1200 (bullish)

Copper 2.62-2.78 (bearish)

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer

Click to enlarge