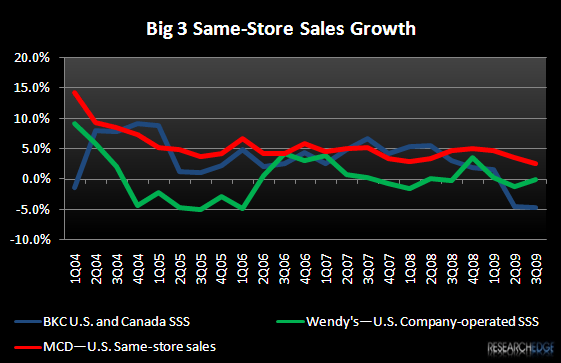

The Big 3 Same-Store Sales chart below does not tell the whole story. It does show that Burger King has lost a considerable amount of market share over the last five quarters to McDonald’s and more recently, Wendy’s. We all know now that Wendy’s 3Q08 value launch of its Double-Stack Cheeseburger, the Crispy Chicken Sandwich and the Junior Bacon Cheeseburger for $0.99 each helped the company to gain market share, largely from BKC. But, that was a year ago and what matters now is where we go from here.

Wendy’s same-store sales turned positive in September 2008 when it introduced these three $0.99 sandwiches to its menu so the company lapped these improved results in the last month of 3Q09 and YOY comparisons are even more difficult come 4Q09 (facing a +3.6% comparison). The chart below includes our flat 3Q09 same-store sales estimate for Wendy’s. Although the company stated that comparables sales growth was up 2% in July, I am expecting the quarterly number to come in below that as a result of the more difficult YOY comparison in September.

BKC rolled out its $1 double cheeseburger nationally on October 19. Although the company did not comment too much on how the product has performed in the last two weeks, management did say yesterday on its fiscal first quarter 2010 earnings call that the markets that supported the new product with media plans during the first quarter (about 25% of U.S. restaurants) generated traffic growth. With the $1 double cheeseburger now in 100% of the U.S. restaurants, BKC could gain some traffic momentum if the test market results correctly reflect what this product can do on a national basis. As for McDonald’s, we already know that October same-store sales are trending flat to negative. As I always say, it is zero sum game so if Burger King begins to get traction with its $1 double cheeseburger, someone else will lose. We could see a market share shift among the big 3 in the coming months. I am not saying Burger King will move ahead of both McDonald’s and Wendy’s, but it could steal some marginal share.

Burger King’s potential traffic gains will not come without expense, however. Management stated yesterday that in the markets that had already rolled out the $1 double cheeseburger, the company experienced both traffic growth and profit dollar growth, but lower YOY gross margin. Specifically, management stated, “margins in the tests were impacted somewhere around 100 to 150 basis points, but GP dollars obviously were up. As we said, what we've seen so far continues to mirror what we saw in the test.”

BKC’s consolidated restaurant margins improved nearly 50 bps during the first quarter while EBIT margins declined. In the first quarter, company restaurant margins in the U.S. and Canada benefited from a 210 basis point improvement in food, paper and product costs and the non-recurrence of startup charges related to the acquisition of 72 restaurants in the prior year. I would expect margins to be under increased pressure in the second quarter with restaurant margins turning negative as well. The company is not only lapping a more difficult restaurant-level margin comparison but the higher mix of sales coming from the $1 double cheeseburger and other value items in the quarter will likely offset the expected YOY commodity cost favorability in the U.S. and Canada.

There are a lot of moving parts on a YOY basis relative to margins and a lot will depend on just how much the increased traffic from the value menu items hurts average check and margins. Commodity costs in the U.S. and Canada should continue to be favorable in 2Q but become less favorable on a YOY basis in 2H10.

Restaurant margins outside the U.S. and Canada were a drag on consolidated results in the first quarter from higher commodity costs and the negative impact of currency translation on cross-border purchases in the UK and Mexico. Currency translation should turn positive in the second quarter and is expected to have a positive impact on earnings on a full-year basis.

From an operating margin standpoint, higher than expected SG&A expenses in the first quarter (+8.6% YOY) hurt results, but the company is forecasting that it will still only be up about 3% for the full year so this pressure should moderate in the coming quarters. D&A, on the other hand, was down 2% in the first quarter and is expected to be up 10%-15% for the full year.

So there are a lot of positive and negative offsets coming in 2Q relative to 1Q, but as I said earlier, I am expecting margins to decline in the current quarter. We could see Burger King gain some top-line momentum and in this environment, getting people in the restaurant seems to matter most to investor sentiment and stock price performance.