In the new world of market expectations gripped on every central bank utterance, indeed markets are getting “wild”.

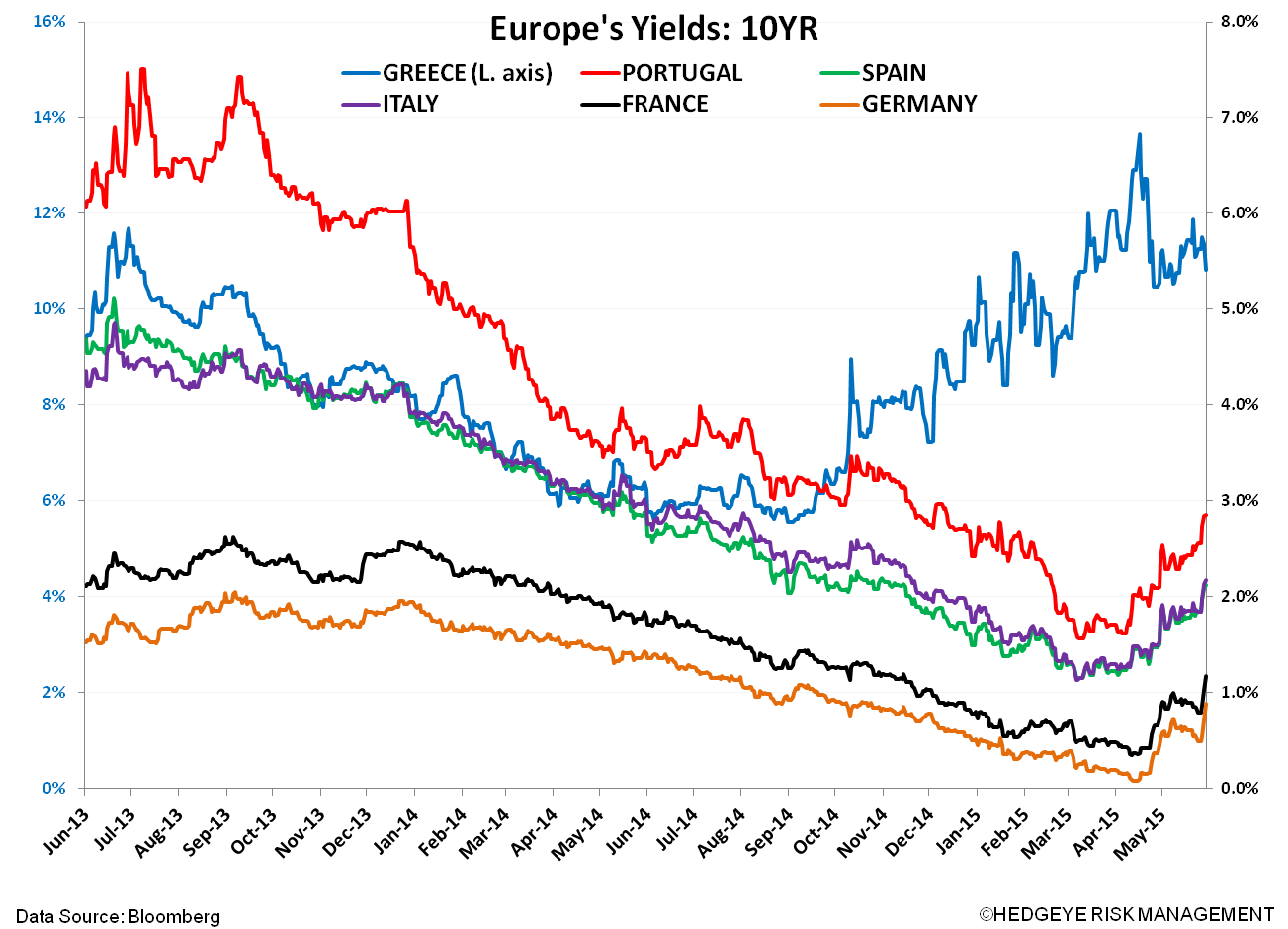

The (in)ability of Greece to pay its debt obligations once again remains pronounced, with just about everyone in the dark about how a “deal” will come together. We view this uncertainty as the biggest drag to the Eurozone equity market in recent weeks, and to boot mixed to weaker data points over the period.

So what’s our thinking on Greece? A deal gets done! Whether it has nails or not, we expect the Eurocrat mentality of #Extend&Pretend Greece’s fiscal burden on the Union to prevail. After all, the Eurocrats are incentivized to play ball to keep Greece in the Union. And in addition, poll after poll shows the Greeks themselves don’t want to leave!

Data Gone Gangbusters? There was great market excitement yesterday when the Eurozone reported CPI at 0.3% in a preliminary MAY reading (Y/Y) vs 0.0% prior. German CPI also saw a positive divergence, rising to 0.7% vs a prior 0.3%.

Sure, the Eurozone print is the first inflationary one in 6 months, and “deflation” could be in the rear view mirror. However, the figure is a long way from the ECB’s CPI target of 2.0%. This is a signal to us that ECB head Mario Draghi’s foot will have to remain planted on the QE gas pedal.

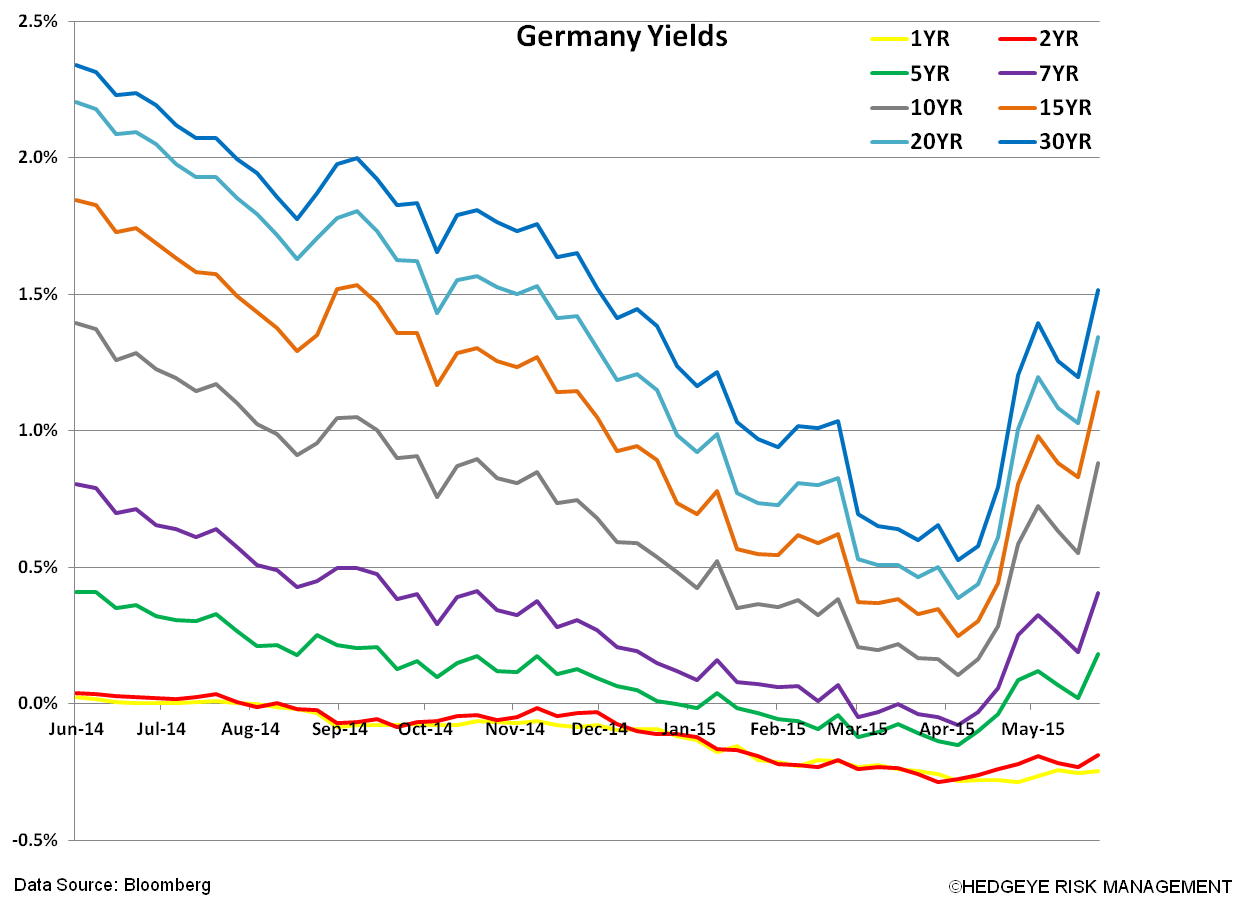

The CPI data led to monster moves across most of the Eurozone sovereign bond market (German 10yr yield ramped from 0.49% to 0.71%, in a day!). But is the move misplaced? Where’s the growth?

Dull Data! Our call remains that we expect economic performance and data to be Slower-For-Longer on both US and Global growth.

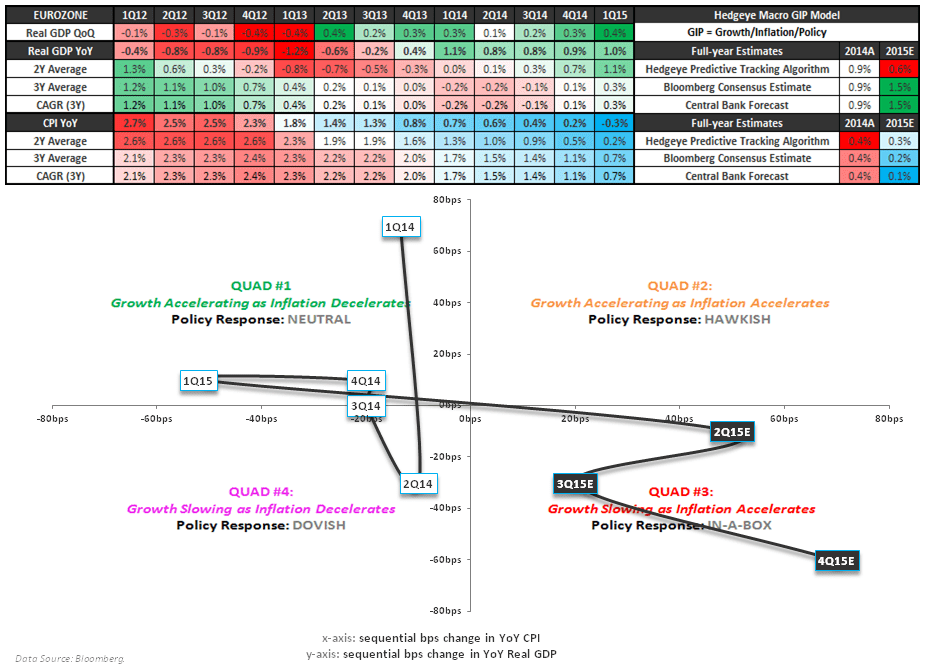

Specific to the Eurozone, our proprietary GIP (growth, inflation, policy) model shows the Eurozone squarely in QUAD3 (= growth slowing as inflation accelerates) for the remainder of 2015.

In addition, today on the ECB call Draghi noted that his team’s economic staff projections remain largely unchanged from the March assessment. As we show below, the pace of economic activity is modest:

- ECB MAY Eurozone GDP staff projections largely UNCH: +1.5% in 2015 (UNCH), +1.9% in 2016 (UNCH), and +2.0% in 2017 (vs 2.1% estimate in MAR)

- ECB MAY Eurozone CPI staff projections revised slightly higher: 0.3% in 2015 (vs 0.0% estimate in MAR), +1.5% in 2016 (UNCH), and +1.8% in 2017 (UNCH)

Further, a couple recent high frequency data points confirm that growth is modest to muted:

- Manufacturing PMIs fell for the Eurozone (52.2 MAY vs 52.3 prior) and Germany (51.1 MAY vs 51.4 prior)

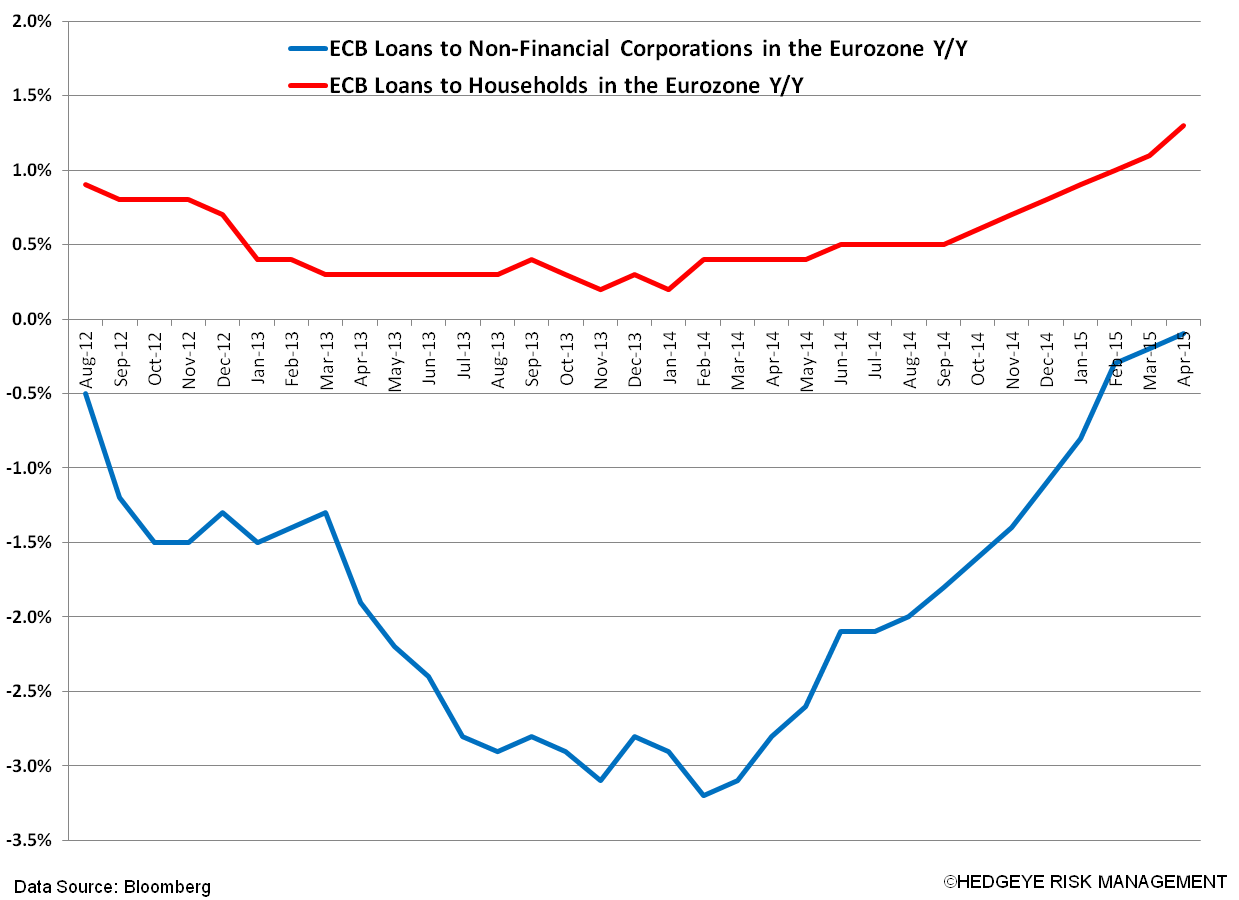

- ECB Loans to Non-Financial Corporations and Households have improved, yet at a very slow rate and low level. Clearly the QE “channel” to the real economy has not materialized for Draghi.

Don’t Rule Out QE! The games central bankers play should not be ignored. While we believe fundamentals matter to investors, we think Draghi’s ability to do “whatever it takes” to move inflation, and in concert equities, higher, he’ll do.

Therefore, we expect a rotation into Eurozone equities to hold up, especially as the Greek headlines fade following a “deal”.

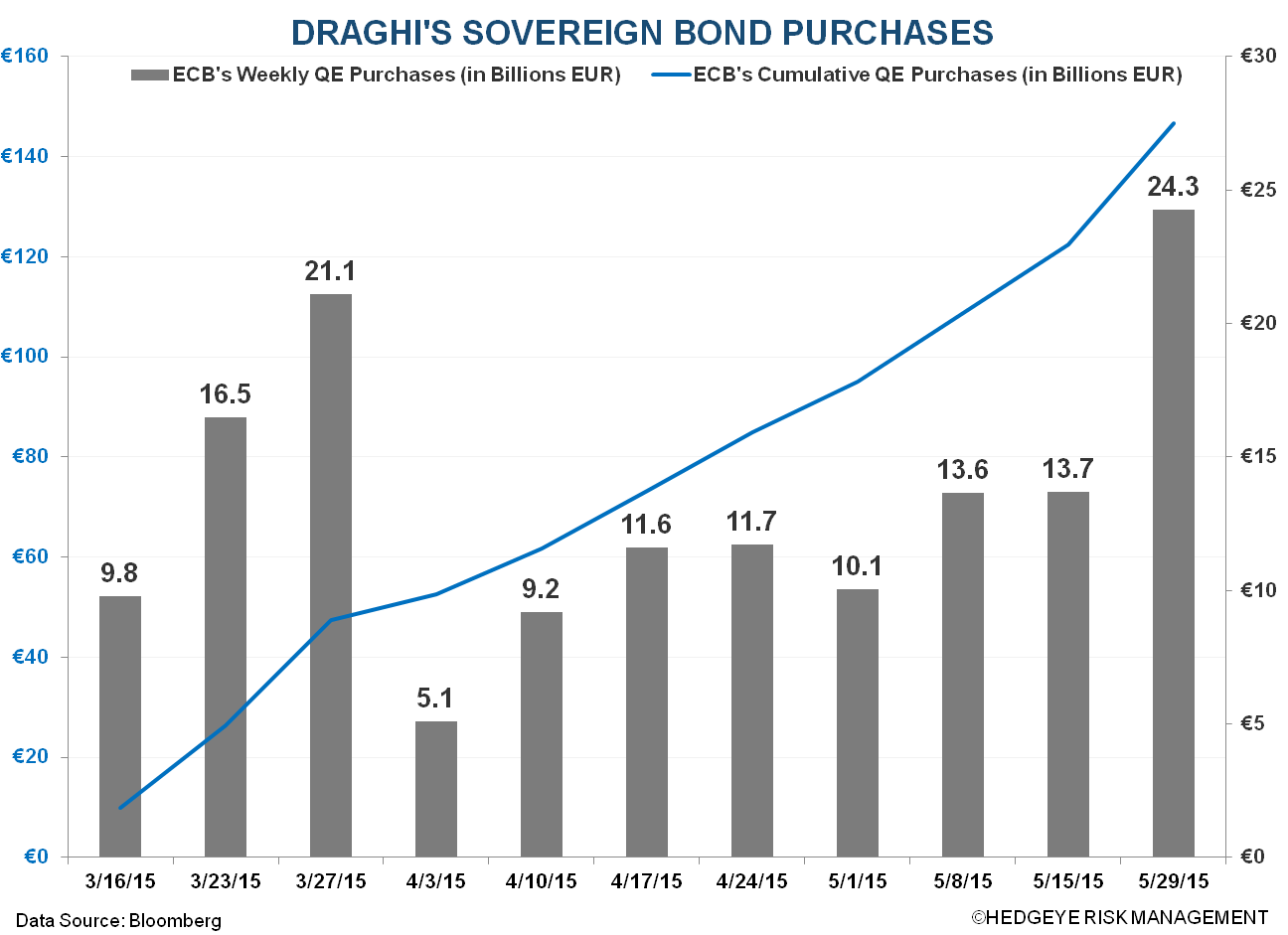

Below we show the pace of QE buying from the ECB. We expect the QE machine to ramp higher over the coming months (see recent buying in the chart below). We got a preview of this a couple of weeks ago when ECB board member Benoit Coeure remarked that the Bank will frontload QE purchases in May and June and will backload in September if needed.

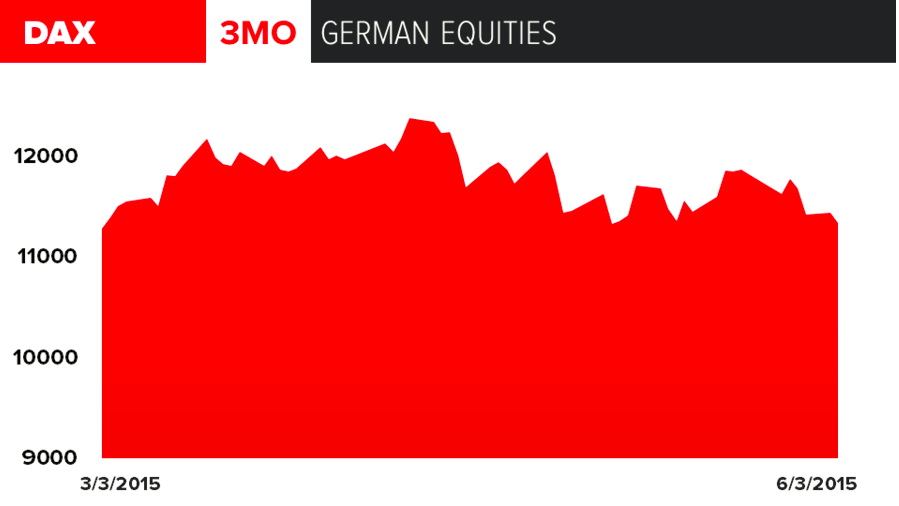

If you’re a believer in the QE game, we continue to like German equities over the intermediate term with the economy levered 47% to exports (a weaker EUR encourages exports). While the DAX remains bearish over the TRADE (immediate term), it remains bullish TREND (intermediate term).